Longevity Insurance and Longevity Swaps

Information

Table of contents

Purpose

This policy advisory provides information and guidance to administrators of federally regulated defined benefit pension plans who are considering entering into a longevity insurance or longevity swap contract as a means of hedging longevity risk. In this policy advisory, the term “longevity risk hedging contract” includes contracts structured either as longevity insurance or longevity swaps. This policy advisory applies to ongoing pension plans and describes:

- the broad types of longevity risk hedging contracts that exist;

- the risks to pension plans associated with these types of longevity hedges;

- considerations for plan administrators who are contemplating entering into a longevity risk hedging contract as a way of reducing their pension plan’s exposure to longevity risk; and

- OSFI’s expectations for plan administrators who choose to enter into a longevity risk hedging contract.

Introduction

The liabilities of defined benefit pension plans are calculated using assumptions, including an assumption about the life expectancy of pension plan members. Assumptions related to life expectancy are generally based on industry mortality tables. The risk that pension plan members will live longer than predicted is referred to as longevity risk.

A number of options are available to pension plans to help them to deal with longevity risk. At the most basic level, a pension plan could carry out an investigation into its own longevity experience and adapt the mortality table appropriately. This would reduce the element of longevity risk resulting from any potential understatement of current liabilities. The risk remains, however, that even revised longevity assumptions could be incorrect over the longer term.

One risk mitigation strategy is for pension plan administrators to purchase buy-in or buy-out annuities for all or some plan beneficiaries. Though the ultimate responsibility for paying pension benefits to plan beneficiaries remains with the pension plan, the purchase of annuities transfers interest rate, investment, and longevity risk from the pension plan to the annuity provider. Longevity risk hedging contracts, whether structured as longevity insurance or as a longevity swap, provide pension plans with a risk mitigation strategy that is focussed more narrowly on longevity risk. By entering into a longevity risk hedging contract, a pension plan administrator seeks to hedge longevity risk while retaining interest rate and investment risk. Longevity risk hedging contracts introduce new challenges for plan administrators, who must consider their complexity, costs and resulting risks. As is the case generally when a plan administrator of an ongoing plan purchases buy-in or buy-out annuities, a plan administrator that enters into a longevity risk hedging contract retains the ultimate responsibility for paying pension benefits.

Although longevity risk hedging contracts have been entered into by a number of pension plans in the U.K., they are new to North America. We understand that plan administrators in Canada are beginning to consider the use of longevity risk hedging contracts. OSFI intends to monitor developments and will consider whether further or revised guidance is necessary.

Longevity Risk Hedging Contracts

Longevity risk hedging contracts are designed to reduce the risk to pension plans of increased costs associated with unfavourable longevity experience (i.e. plan members living longer than reflected in mortality assumptions). There are two types of longevity risk hedging contracts: indemnity-based and index-based contracts.

With both indemnity-based and index-based longevity risk hedging contracts, the pension plan administrator agrees to provide a counterparty with regular pre-determined, or “fixed”, payments based on agreed upon mortality assumptions. In return, the counterparty provides the pension plan with regular floating payments based on either the pension plan’s actual mortality experience (indemnity-based longevity contract) or an agreed upon mortality index (index-based longevity contract). As a result, the pension plan has more predictable outflows over the period of the longevity risk hedging contract. The counterparty to the contract assumes the longevity risk over the period covered by the contract.

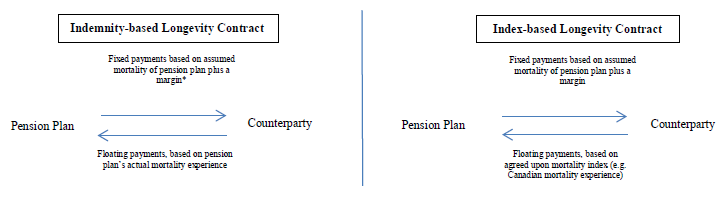

Comparison of an indemnity-based longevity contract versus an index-based longevity contract – Text version

There are two types of longevity risk hedging contracts: indemnity-based and index-based. For both types of contracts, the pension plan administrator agrees to provide a counterparty with fixed payments based on assumed mortality assumptions plus a margin. The pension plan administrator and the counterparty will generally agree on a mortality basis that represents the best estimate of future mortality for the covered group. The margin included in the fixed payments represents the risk premium required by the counterparty to assume the longevity risk and expenses. In return, the counterparty provides the pension plan with regular floating payments based on either the pension plan’s actual mortality experience (indemnity-based longevity contract), or an agreed upon mortality index, such as the Canadian mortality experience (index-based longevity contract). As a result, the pension plan has more predictable outflows over the period of the longevity risk hedging contract. The counterparty to the contract assumes the longevity risk over the period covered by the contract.

*The pension plan administrator and the counterparty will generally agree on a mortality basis that represents the best estimate of future mortality for the covered group. The margin included in the fixed payments represents the risk premium required by the counterparty to assume the longevity risk and expenses.

In the case of indemnity-based longevity contracts, if the pension plan’s beneficiaries live longer than was assumed for the purposes of setting the plan’s fixed payments, higher payments from the counterparty to the pension plan serve to offset the plan’s higher pension costs. In this scenario, the indemnity-based contract will generally be “in the money”, or have a positive value, for the pension plan. If, on the other hand, beneficiaries do not live as long as assumed, lower payments from the counterparty to the pension plan mean that the overall cost to the pension plan of paying beneficiaries’ pensions will effectively be held constant. In this way, indemnity-based contracts insulate pension plans both from increases and decreases in costs arising from unanticipated changes in the longevity of the plan’s beneficiaries.

In the case of index-based contracts, the actual mortality experience of the pension plan does not affect the amount of the payments from the counterparty to the pension plan. However, if there is an increase in longevity as measured by the index used to set the counterparty’s payments to the pension plan, this will result in higher payments from the counterparty to the plan (and vice versa). To the extent that changes in the mortality of the pension plan beneficiaries track changes in the index, the plan’s longevity risk will be mitigated by the contract. Pension plans that pursue an index-based contract are, however, faced with basis risk, which is discussed in the next section of this paper.

Risks for a Pension Plan

Counterparty Risk

Counterparty risk is the risk to the pension plan that the counterparty to the longevity risk hedging contract will not live up to its contractual obligations. Payment flows between the counterparties are generally netted, and collateral can be used to further mitigate counterparty risk. For a longevity swap, collateralization would follow typical practices for swaps and would require the counterparty to pledge assets (e.g. cash or securities pledged in respect of any net obligation to the other party) that can be seized in the event of default. Collateral is not typically required for indemnity based contracts; however, counterparty risk could be addressed through similar means, such as the taking of a security interest. Administrators of plans that pledge assets should examine the risks of these activities and ensure that these risks are addressed in the plan’s Statement of Investment Policies and Procedures.Footnote 1 Further, plan administrators should ensure that the pledging of assets is permitted by the terms of the pension plan and any supporting documents such as a trust agreement. A relevant factor in assessing counterparty risk is the regulatory regime to which the counterparty is subject, including whether assets are required to be held by the counterparty in respect of the contract and any applicable capital requirements.

In a longevity risk hedging contract, the initial amount of counterparty risk to the pension plan is generally small, but could increase over time if the contract moves into the money. Counterparty risk is likely to be small relative to the value of liabilities covered, both because payments are netted and because only unexpected changes in longevity affect the net amount owed. In other words, the underlying expected pension payments are not at risk in this case, it is only the ability of the counterparty to pay the additional payments resulting from beneficiaries living longer than expected or from changes in the underlying index. Plan administrators should consider the strength of the counterparty before entering into a longevity risk hedging contract.Footnote 2

Counterparty strength can be assessed, for example, through a review and understanding of:

- credit ratings for the counterparty;

- the regulatory regime in which the counterparty operates, including whether the counterparty is subject to rigorous regulatory oversight, including strong capital adequacy requirements; and

- the prudential and risk management requirements of the counterparty.

Rollover Risk

Longevity risk hedging contracts that are entered into for a shorter time period than the liabilities covered introduce the element of rollover risk to the pension plan. Specifically, although the contract protects the plan against changes in mortality over the period of the contract, it does not cover the risk of having to enter into a new contract once the contract expires. Rollover risk is the risk that entering into this new contract will be more expensive, as may result from changes in mortality expectations.

Indemnity-based risk hedging contracts introduce little or no rollover risk as they are typically structured for the remaining life of the covered populations, or alternatively for a fixed period that is long enough to cover the life expectancy of the majority of the covered population.

Basis Risk

A pension plan that elects to enter into an index-based longevity risk hedging contract is exposed to basis risk. Basis risk is the risk stemming from the possibility that the mortality experience of the pension plan can differ from that of the index on which the contract is based (i.e. the mortality table or index upon which the floating payments are based). The more similar the composition of the index to the plan members covered, the better the index hedge. It should be noted that basis risk could result in a significant reduction in the effectiveness of a longevity risk hedging contract (i.e. if the experience of a pension plan is such that there is a significant improvement in longevity compared to the index on which the swap is based).

Indemnity-based longevity risk hedging contracts introduce no basis risk as they indemnify the pension plan for actual experience (i.e. the floating payments are based on the actual mortality experience of the plan).

Legal risk

Longevity risk hedging contracts are legal agreements and are not traded on an exchange. The parties negotiating the contract must pay close attention to the terms of the contract. Plan administrators should fully understand the terms and risks of the transaction and seek legal advice before entering into a longevity risk hedging contract. Issues to consider:

- the legal ability of the counterparty to enter into a longevity risk hedging contract; and

- whether there may be difficulty in enforcing any legal rights against the counterparty if it is resident outside Canada and all or a substantial portion of its assets are located outside Canada.

Considerations for a Plan Administrator

A plan administrator who is considering entering into a longevity risk hedging contract must not only understand the risks and benefits that this transaction introduces to the pension plan, but also understand the terms of the contract. Specific considerations for a plan administrator include:

-

Cost: In determining whether a longevity risk hedging contract offers a pension plan value for the cost of entering into the contract, a plan administrator needs to understand how much risk is being hedged (i.e. potential for additional payments that may need to be made in the future due to increased life expectancy) versus the cost of hedging that risk (i.e. cost of the longevity risk hedging product).

Before entering into a longevity risk hedging contract, a plan administrator could conduct an investigation into the pension plan’s own longevity experience which would help the administrator understand the amount of risk that is to be hedged and would help ensure that the risk reduction justifies the cost of entering into the contract.

Whatever structure is used (index-based or indemnity-based), the plan administrator should ensure that it receives market-based prices from a number of potential counterparties to compare, thus helping to ensure that a fair market price is paid.

-

Acceptability: Under federal pension legislation, the plan administrator would have to satisfy itself that entering into a longevity risk hedging contract is in the best interests of beneficiaries and is in accordance with:

- the terms of the pension plan and the plan’s Statement of Investment Policies and Procedures;

- the standard of care required in administering the pension plan and a pension fund under subsection 8(4) and the prudent portfolio requirements under subsection 8(4.1) of the Pension Benefits Standards Act, 1985 (PBSA);

- the Pension Benefits Standards Regulations, 1985 (Regulations); and

- Schedule III to the Regulations.

The plan administrator is responsible for continuing to monitor the longevity risk hedging contract and ensuring continued compliance with the terms of the contract, the terms of the pension plan, the PBSA, and its Regulations.

- Administrative Complexity: Although a longevity risk hedging contract can transfer some of the longevity risk from the pension plan to a counterparty, they add an additional level of administrative complexity that needs to be managed. Potential examples include processes for ensuring that the payments between the pension plan and a counterparty are timely and correct, processes for the posting of collateral (if required), and the potential need for periodic monitoring of the financial strength of the counterparty.

-

Duration: In some cases, a longevity risk hedging contract will only enable a plan administrator to manage the longevity risk in the pension plan for a period of time that is shorter than the life of the plan’s liabilities. When a longevity risk hedging contract expires, the pension plan will again be exposed to unhedged longevity risk. The plan administrator should also consider the implications of entering into very long-term contracts, as the pension plan may be locking itself into payments to the counterparty for a long period of time, which could limit flexibility to respond to changing circumstances in the future (e.g. pricing, changes due to competition, changes to the creditworthiness of the counterparty, tax or regulatory changes, or the development of alternative investment products or strategies). Issues related to the duration of a longevity risk hedging contract could potentially be mitigated through appropriate terms in the contract.

As a longevity risk hedging contract could be structured so that it only covers retirees that are currently receiving a pension, a plan administrator should consider how to deal with the longevity risk of members who retire after the contract has been entered into.

-

Liquidity: The plan administrator should consider the fact that it will be difficult to sell or cancel a longevity risk hedging contract once it has been entered into. Unlike more commonly used swaps, such as interest rate swaps, there is currently no active, liquid market where longevity swaps are traded. A plan administrator may be able to “artificially” cancel a longevity swap by entering into an offsetting swap, by which the pension plan would receive a fixed payment and make a floating payment – however in practice, this may not be possible or practical.

A longevity insurance contract may include provisions for termination upon agreement of each party to the contract and provisions for conversion to an annuity policy. In evaluating the risks and obligations associated with a risk hedging contract, the plan administrator should consider the terms under which the contract may be modified or terminated. Also, the terms of the contract should address the possibility of plan termination or other significant transactions such as a plan merger or a plan conversion and what would happen in such instances.

-

Actuarial Valuation Implications: A going concern valuation assumes that a pension plan continues indefinitely. Although entering into an indemnity-based contract will have served to mitigate longevity risk, if the beneficiaries in the plan experience higher mortality (i.e. die earlier) than the agreed upon mortality assumptions used to determine the plan’s fixed payments, the funded position of the plan will be less than it would have been had the contract not been entered into. Conversely, if beneficiaries in the plan experience lower mortality than the agreed-upon mortality assumptions, the contract will help off-set the cost to the plan of the effect of this lower mortality.

For an index-based contract, if there is an increase in longevity as measured by the index used to set the counterparty’s payments to the pension plan, this will result in higher payments from the counterparty to the pension plan and the funded position of the pension plan will be higher than it would have been had the contract not been entered into. Conversely, if there is a decrease in longevity as measured by the index used to set the counterparty’s payments to the pension plan, this will result in lower payments from the counterparty to the pension plan and the funded position of the pension plan will be lower.

When valuing a longevity risk hedging contract as part of a going concern valuation, OSFI expects actuaries to include margins for adverse deviations. Actuaries should consider margins for counterparty risk and, where applicable, basis, rollover and other risks. In addition, each time a going concern valuation is completed, the gain and loss analysis would have to include an item related to either a gain or a loss on the longevity risk hedging contract. Expense provisions would need to reflect costs associated with the longevity risk hedging contract.

Example: Consider a pension plan that holds the following indemnity-based longevity contract.

Example of a pension plan that holds an indemnity-based longevity contract. Text version below

In the example, the pension plan administrator agrees to provide a counterparty with fixed payments based on the expected mortality of the pension plan determined using mortality assumptions agreed between the plan administrator and counterparty, plus a margin. In return, the counterparty provides the pension plan with regular floating payments based on the pension plan’s actual mortality experience.

Suppose that, in year 3 of the contract, there is a material improvement in the pension plan members’ life expectancies. The actuary would likely suggest a new, more conservative, mortality table. In this case:

-

Under the terms of the contract, floating payments would continue to be based on the actual mortality of pension plan members.

-

Although the pension plan would have to value its liabilities using the new, more conservative, mortality table, the present value of floating payments received from the counterparty would offset the additional liabilities (i.e. because of the longevity risk hedging contract, the pension plan would not experience an overall loss or have to fund the increase in liabilities caused by the change to the more conservative mortality table).

The above example is for illustrative purposes only. The actual realized effects of an indemnity-based longevity risk hedging contract would depend on the particulars of the transaction (e.g. costs, rollover and counterparty risks).

A solvency valuation provides a point in time snapshot of the financial position of a pension plan, assuming that the plan terminates on the valuation date. Solvency valuations should reflect the value that a longevity risk hedging contract would have on plan termination. That value will depend on the terms of the contract that set out the obligations of the parties in the event of plan termination.

OSFI Views and Expectations for Pension Plan Administrators Entering into Longevity Risk Hedging Contracts

It is OSFI’s view that a longevity risk hedging contract is a permissible investment provided that it is consistent with the terms of the pension plan and the plan’s Statement of Investment Policies and Procedures, that it complies with the PBSA and the Regulations, and that the administrator exercises proper due diligence. There is no requirement that plan administrators obtain approval from OSFI to enter into such a contract, nor is there any specific requirement to inform members of the existence of the contract. Plan administrators continue to be responsible for paying beneficiaries’ benefits, including in the event that a counterparty fails to make the agreed upon contractual payments to the pension plan. Before entering into a longevity risk hedging contract, OSFI would expect plan administrators to:

- understand the impact of longevity risk on their pension plan (e.g. via stress testing - by considering pension liabilities over a range of longevity scenarios);

- determine whether entering into the longevity risk hedging contract is in the best interests of beneficiaries;

- determine whether the longevity risk hedging contract offers value for the cost of entering into the contract;

- consider the risks to the pension plan associated with investing in a longevity risk hedging contract (e.g. counterparty risk, rollover risk, basis risk and legal risk);

- ensure that laws concerning data privacy are followed;

- develop adequate controls and oversight to manage these risks; and

- understand the longevity risk hedging contract (e.g. terms, associated costs, collateral, strength of counterparty, and benefits covered).

In order to demonstrate that they meet OSFI’s expectations, plan administrators should ensure that:

- individuals with the appropriate level of knowledge are involved in the decision-making process and/or advice is received from individuals with experience in this market;

- the longevity risk hedging contract is monitored and reviewed on a regular basis; and

- the above items are well documented.

In managing risks associated with longevity risk hedging contracts, plan administrators are also expected to consider the factors outlined in OSFI’s Guideline on Derivatives Best Practices for pension plans.

Footnotes

- Footnote 1

-

See OSFI’s Investment Policy Guideline: http://www.osfi-bsif.gc.ca/Eng/pp-rr/ppa-rra/inv-plc/Pages/penivst.aspx

- Footnote 2

-

Though there is a potential for the counterparty to transfer the longevity risk to another party (either through re-insurance or a subsequent longevity swap) the contractual obligation to the pension plan remains with the original counterparty.