OSFI Annual Report 2020-2021

Table of contents

Superintendent's Message

OSFI's job is to provide prudential regulation and supervision of C2019anada's banks, most of its insurance companies and a number of its private pension plans. We also house the Office of the Chief Actuary, an independent unit that provides a range of actuarial services to the Government of Canada including actuarial reports on the Canada Pension Plan, the Old Age Security Program and the Canada Student Loans Program among others.

These are weighty responsibilities. Many of the organizations we supervise are the lifeblood of our economy. They represent the hopes of many Canadians who have saved and invested for a better life, and their actions are key to a healthy and growing economy.

The period covered by this annual report was dominated by a singular global issue: the COVID-19 pandemic. While the first wave was well underway in Canada before the start of our fiscal year in April 1, 2020, COVID-19 would continue to influence the economy in profound ways during the ensuing 12 months.

Of course, we at OSFI have managed through uncertainty and upheaval before—in 2008, for example, during the global financial crisis, and in 1990 during another worldwide recession. In fact, we have a nearly 35-year track record of success founded on evidence-based, robust regulation and supervision.

Our experiences have taught us that complacency—thinking that what worked then will work again—is the antithesis of financial stability. We also know that the best countermeasure for uncertain times is preparation during periods of stability.

We are proud of the fact that our actions and guidance as a prudential regulator and supervisor helped prepare Canada's financial system to weather the worst that the pandemic had to offer.

In March 2020 we announced a series of regulatory adjustments to support the financial and operational resilience of federally regulated banks, insurers and private pension plans. As uncertainty caused by the pandemic receded, the need for these measures diminished and we reversed many of them over the course of the fiscal year.

Also in March 2020 we paused our consultative and policy development work to allow financial institutions and pension plans to focus on their responses to COVID-19. We restarted that work later in 2020 and, as a result, we have gained a new impetus for our work on emerging issues such as technology risk and climate-related risks.

Despite having to adjust in real time to this crisis as it emerged, we never lost sight of our longer-term goals. We continue to deliver on the Strategic Plan we published in April 2019. We are committed to furthering our work to build preparedness and resilience to financial and non-financial risk throughout the financial system, as well as improve our own agility, operational effectiveness, transparency and accountability.

I am grateful to everyone at OSFI for their efforts in what was, without doubt, an exceptional year, and for the continued support of all our partner agencies.

By the time you read this, OSFI will be led by Peter Routledge, who was appointed Superintendent of Financial Institutions in June 2021. I know that under Peter's leadership, OSFI will continue to deliver on its vision, mandate and strategic goals in the service of a sound and stable financial system.

Jeremy Rudin

Superintendent

OSFI's Vision, Mandate and Strategic Goals

In January 2021 we released a new video titled "Protecting Canada from a financial crisis". This video provides an overview of our role and the tools we use to prepare for certain risks such as cyberattacks and pandemics like COVID-19. As Canada's financial regulator, we plan and prepare for events that could affect Canada's financial system.

Vision

Building OSFI for today and tomorrow: preserving confidence, ever vigilant, always improving.

Mandate

Our mandate is to protect depositors, policyholders, financial institution creditors and pension plan beneficiaries, while allowing financial institutions to compete and take reasonable risks.

We achieve this through:

Fostering sound risk management and governance practices

We advance a regulatory framework designed to control and manage risk.

Supervision and early intervention

We supervise federally regulated financial institutions (FRFIs) and federally regulated pension plans (FRPPs) to ensure they are in sound financial condition and meet regulatory and supervisory requirements.

We notify financial institutions and pension plans if there are material deficiencies. If there are, we take or order corrective action to quickly address the situation.

Environmental scanning linked to safety and soundness of financial institutions

We monitor and evaluate system-wide or sectoral developments that may affect the financial condition of FRFIs.

Taking a balanced approach

We act to protect the rights and interests of depositors, policyholders, financial institution creditors and pension plan beneficiaries.

We consider financial institutions' need to compete effectively and take reasonable risks.

We recognize that an organization's management, boards of directors and pension plan administrators are ultimately responsible for risk decisions. We also recognize that financial institutions can fail and pension plans can experience financial difficulties resulting in the loss of benefits.

Strategic Plan

In March 2019, we released the 2019-2022 OSFI Strategic Plan. Its focus is a core strategic agenda that lays out the expected criteria for success. Central to the plan are four goals that guide all that we do:

- FRFI and FRPP preparedness and resilience to financial risk is improved, both in normal conditions and in the next financial stress event;

- FRFIs and FRPPs are better prepared to identify and develop resilience to non-financial risks before they negatively affect their financial condition;

- Our agility and operational effectiveness are improved; and

- Support from Canadians and cooperation from the financial industry are preserved.

Following the launch of our Strategic Plan, our sectors prepared a plan to meet the priorities identified through activities, projects and allocated resources.

Reporting Results

Measuring progress against the Strategic Plan is important, both in the actions we take and the results we achieve. As with the 2019-2020 fiscal year, we made significant progress in advancing our strategic goals in 2020-21. Although the Strategic Plan was finalized well before the COVID-19 pandemic took hold, we adapted to include our response to COVID-19 (see next section) and the measures taken to mitigate its effects on Canada's financial sector.

| GOAL 1: FRFI and FRPP preparedness and resilience to financial risk is improved, both in normal conditions and in the next financial stress event | |

|---|---|

| Sub Priorities |

|

| Progress in 2020‑21 |

|

| GOAL 2: FRFIs and FRPPs are better prepared to identify and develop resilience to non-financial risks before they negatively affect their financial condition | |

| Sub Priorities |

|

| Progress in 2020‑21 |

|

| GOAL 3: Our agility and operational effectiveness are improved | |

| Sub Priorities |

|

| Progress in 2020‑21 |

|

| GOAL 4: Support from Canadians and cooperation from the financial industry are preserved | |

| Sub Priorities |

|

| Progress in 2020‑21 |

|

Response to COVID-19

Even before the 2020-2021 fiscal year had begun on April 1, 2020, we acted to support Canada's FRFIs and FRPPs in weathering the risks posed by COVID-19.

During March 2020, we:

- lowered the Domestic Stability Buffer (DSB) requirement for domestic systemically important banks (D-SIBs) to 1% of total risk-weighted assets;

- postponed all consultation and policy development to give the entities we regulate an opportunity to focus on the challenges posed by the pandemic;

- announced a series of regulatory adjustments to support the financial and operational resilience of federally regulated banks, insurers and private pension plans;

- announced the expectation that federally regulated financial institutions not increase regular dividends, undertake common share buybacks or raise executive compensation until further notice; and

- issued direction on how federally regulated deposit-taking institutions should treat new capital made available to Canada's small and medium-sized businesses through the Government of Canada's various COVID-19 relief programs.

By the start of the 2020-2021 fiscal year, Canada was seeing more than 1,000 new cases of COVID-19 daily. Despite the spread of the virus, the early measures we put in place in March 2020 helped ensure Canadian financial institutions and private pension plans were positioned to withstand any pandemic-related economic stress that might affect their operations.

In April 2020 we announced key measures so that federally regulated banks could continue lending, and insurers could operate without increased capital requirements during the first wave of the pandemic.

In December 2020, we reaffirmed our decision to keep the DSB at its lower level of 1%. From the start of the pandemic, the 1% DSB level remained effective in supporting the resilience of the banking system. Our decision to keep the DSB at 1% was supported by the strength in banks' capital levels as well as evidence that banks continued to lend to Canadians.

In the latter half of 2020 we signaled that, under limited circumstances, federally regulated financial institutions may be permitted to offer a non-recurring payment of a special or irregular dividend. We also provided guidance to federally regulated financial institutions on the treatment of new loans to businesses under the Government's Highly Affected Sectors Credit Availability Program, which launched in January 2021.

By the spring of 2021, there were signs that the pandemic's potential impact on the financial sector had lessened. As a result, in March 2021 we announced that the Stressed Value at Risk ("SVaR") multiplier, a component of the market risk capital requirements that ensures that a minimum amount of capital is held against stress periods, would return to pre-pandemic levels.

Further details on specific measures taken by our divisions overseeing deposit-taking institutions, insurers, pension plans, and risk specialists will be outlined throughout this document.

Throughout the extraordinary circumstances posed by the COVID-19 pandemic, we ensured, as always, that our guidance remained credible, consistent, necessary and fit-for-purpose in the Canadian context. We continue to do so.

OSFI'S Operating Environment – Overview of Key Risks

Approach to Risk

We aim to ensure that federally regulated financial institutions (FRFIs) are always prepared to continue functioning through a range of severe yet plausible economic scenarios. The COVID-19 pandemic turned out to be such an event.

We evaluate whether these preparations are adequate to deal with the potential impact of risks. This requires us to identify both financial and non-financial risks as well as ways to mitigate and manage these risks. In 2020-21, we expanded and enhanced our tools for identifying new risks, and analyzing and reporting on existing and emerging risks.

Our approach to supervision is risk-based. It reflects the nature, size, complexity and risk profile of an institution and allows these entities to take reasonable risks and compete effectively. As such, our supervisory plans quickly shifted to focus on ensuring we understood and addressed the real and potential impacts of the pandemic. Although we play an essential oversight role, the executive management and boards of directors of institutions and pension plan administrators are responsible for their success or failure.

We constantly evaluate system-wide developments that may have an adverse impact on financial institutions and the financial system as a whole. The following section provides an overview of the key financial and non-financial risks on which we focused in the 2020-2021 fiscal year. More details on specific risks for deposit-taking institutions, insurers and private pension plans are available under the sections pertaining to our work with these entities.

Financial Risks

Financial risks continued to be present for most of the 2020-2021 fiscal year. The operating environment for FRFIs was volatile and challenging. It included a precipitous decline in economic growth and employment—and a deterioration in the credit, liquidity and funding environment—against a backdrop of high and growing household and corporate debt.

Household Debt

Throughout the 2020-2021 fiscal year, overall household indebtedness posed the largest risk for many FRFIs.

COVID‑19 created severe pressure on household employment incomes, with a large share of the labour force unemployed or substantially underutilized at the beginning of the pandemic. In fact, the unemployment rate in April 2020 was higher than during the 2007-09 global financial crisis, and those employed were working much fewer hours.

From the onset of the pandemic in March 2020 until January 2021, household debt rose by nearly 3.5%, largely due to an increase in mortgage debt. By the end of the 2020 calendar year, accumulated mortgage debt was 85% of Canada's GDP. This growth in mortgage debt was linked to both elevated levels of housing activity and the corresponding rise in house prices.

In a positive development, however, consumer indebtedness started to decrease in December 2020 as many Canadians made accelerated payments on products such as credit cards and lines of credit. According to the Bank of Canada's 2021 Financial System Review, the vast majority of households that benefitted from loan deferrals in 2020 have resumed making regular payments. As well, the number of personal bankruptcies dropped by 40% in 2020 compared with 2019. However, a long-term trend towards growing household indebtedness persists, and may indicate vulnerability in the Canadian economy and financial system.

Lenders subject to our supervision held nearly 80 percent of all residential mortgages issued in Canada, and residential mortgage loans account for almost 30 percent of the total assets held by these lenders. This meant that any significant fall in housing prices could have led to material credit losses for lenders. Similarly, in the event of a significant and sustained increase in mortgage borrowing rates or the unemployment rate, repayment capacity by borrowers could have elevated the vulnerability of mortgage insurers to higher claims.

Business Credit Risks

In a spring 2020 survey, about one-third of Canadian businesses reported a drop in revenue of at least 40 percent in the first quarter of 2020, compared with the same quarter in 2019. An additional one-fifth of businesses reported drops in revenue between 20 and 40 percent. These declines in revenue disproportionately affected small and medium-sized enterprises, which employ the large majority of private-sector workers.

While declines in business revenue were felt across virtually every sector in the first quarter of 2020, the greatest drops were in accommodation and food services, the arts, entertainment and recreation, and the retail trade.

The sharp drop in revenues caused by COVID‑19 meant that many businesses had difficulty meeting fixed payments, including debt repayment. The problem was particularly acute for businesses carrying a high overall level of indebtedness, as well as energy firms: the lower oil prices brought about by COVID-19 were exacerbated by the lingering effects from the collapse in world oil prices in 2014-16.

In the longer term, lingering concerns about the pandemic could lead to lower demand in some parts of the economy—for example, the travel and hospitality industry—with a significant negative effect on firms' revenue and earnings. This could create solvency issues for firms unable to access credit from financial markets and banks, especially if stress in the financial system returns with subsequent waves of the pandemic.

In 2020-21 we also watched credit extension closely, particularly in areas potentially most affected by the pandemic, including commercial real estate and hospitality. Continued economic disruption could have negatively affected asset values resulting in financial losses.

Another area of increased risk monitoring was debt in the non-financial corporate sector. Business debt has seen significant growth in the past few years; last year was no exception, with a growing proportion of weaker structures such as less strict loan covenants (conditions on borrowers).

Climate Risk

As a subset of Environmental, Social and Governance (ESG) issues, climate risk has been garnering increased attention from prudential regulators, both in Canada and globally.

In November 2020 we launched a pilot project on climate-related risk with the Bank of Canada and six participating financial institutions. Through this initiative, we are gaining a better understanding of the risks to the financial system posed by the transition to a low-carbon economy.

This pilot project will also help build enhanced capability in analyzing and enhancing disclosure of climate-related risks, increase understanding of transition risks for the financial sector, and improve our understanding of governance and risk-management practices around climate-related risks and opportunities.

In January 2021 we launched a three-month consultation on the potential impact of climate-related risks on FRFIs and FRPPs with the publication of a discussion paper. In this paper, titled Navigating Uncertainty in Climate Change: Promoting Preparedness and Resilience to Climate-Related Risks, we outlined the possible risks stemming from climate change that could affect the safety and soundness of the organizations we regulate.

As is the case with other regulators, we see three main types of risk associated with climate change that could have a material impact on FRFIs and FRPPs:

- Physical risk, which comes from the increased frequency and severity of adverse weather events such as wildfires, floods, wind events such as hurricanes and tornados and rising sea levels, among others;

- Transition risk, which stems from changes in government policies and consumer preferences as well as technological advances as Canada moves to a low- or zero-greenhouse gas economy; and

- Liability risk, which relates to the potential for organizations to be targeted by climate-related litigation based on their investment and lending policies and practices.

As part of this discussion paper and consultation period, we sought comments on and insight into how FRFIs and FRPPs define, identify, measure and build resilience to climate‑related risks, and the role we might play in fostering preparedness for, and resilience to, these risks.

We are a member of the Basel Committee on Banking Supervision's high-level task force on climate-related financial risks, where we shared regulatory and supervisory initiatives with other banking regulators. This task force is expected to publish two reports on transmission channels and measurement methodologies for climate-related financial risks in mid-2021.

On the insurance side of climate-related risks, we track and contribute to work being done through the Sustainable Insurance Forum and the International Association of Insurance Supervisors. We have also joined a working group organized by the Network for Greening the Financial System that is examining data gaps in micro-prudential surveillance.

We continue to advance our understanding of climate-related risks of relevance to FRFIs and FRPPs. We will release a summary of comments received during our climate-related risk consultations and next steps in the 2021-22 fiscal year.

Non-Financial Risks

In all cases of non-financial risk, we are most concerned with how these risks might impact a FRFI's reputation risk and possibly materialize as financial losses. Mismanaging non-financial risk events such as data breaches, cyber attacks and most recently the COVID-19 pandemic can impact operational continuity of critical services and functions, divert resources to focus on the disruption and impact confidence in financial institutions.

In 2020-21 we enhanced our capabilities in assessing non-financial risks by building assessment frameworks and approaches to oversee technology and cyber risk as well as "people" risk. We also furthered our thinking on the topic of operational resilience and third- party risk management by providing input at international forums, gathering information on current practices through our technology risk discussion paper published in September 2020 and completing a third-party study.

Model Risk

While the use of modelling across different aspects of their businesses—such as risk measurement, pricing, marketing effectiveness and instances of fraud, among others—is invaluable for the financial institutions overseen by OSFI, the pandemic has demonstrated the fragility of such models as well as challenges related to model responsiveness. Financial institutions' swift actions such as applying model overlays and tightening conditions for model use have addressed model shortcomings in the short term, but a deterioration in model performance is expected once government relief programs have ended.

One of the key upcoming modeling challenges is reconciling new data and relationships that have emerged during the pandemic with existing data, which has historically followed a different regime. In some cases, this may result in the data prior to the pandemic losing its predictive ability, while in other instances data from the pandemic period may carry little importance for future modeling and assessment of risk. These challenges further illustrate the need to develop more agile and robust model risk management (MRM) frameworks, including new analytical approaches that can quickly adapt to new and radically different environments.

Advanced analytics tools such as Artificial Intelligence and Machine Learning (AI/ML) are expected to increase in importance both in terms of advancing MRM frameworks and in enhancing or creating new products and services. In addition to their benefits and opportunities, these advanced techniques introduce new risk and amplify existing ones. To that end, we are focusing on assessing how institutions use and manage AI/ML as well as developing additional principles to address emerging risks resulting from their use. This work is ongoing and will be used to inform an industry letter on advanced analytics and model risk as well as a revised model risk guideline, to be published in Q1 2022 and 2022-23 respectively.

Technology and Cyber Security Risk

Technology risk is the risk arising from the inadequacy, disruption, failure, loss or malicious use of the information technology systems, infrastructure, people or processes that enable and support business needs. The lack or ineffectiveness of controls to mitigate these risks can impact the confidentiality, integrity and availability of data and systems that support business services.

Throughout the year, technology risks were front and center at the FRFIs we regulate. The pandemic shone a spotlight on issues related to technology currency and technology debt, authentication, vulnerability and patch management, technology change management, accelerated movement to the cloud, and an advancement in digital innovation. All of these technology-related issues have an impact on existing business models. In addition to our increased and focused monitoring throughout the pandemic, OSFI shared technology risk bulletins focusing on Multi-Factor Authentication, and more recently on API security and risks, with FRFIs.

One component of technology risk is cyber security risk. This year, we observed increases in ransomware and supply chain attacks. While FRFIs themselves faired relatively well against ransomware, this threat affected their third and fourth parties—in other words, not just FRFIs' providers and suppliers, but their providers' and suppliers' providers and suppliers—causing notable disruptions to and impacts on FRFIs.

Supply chain attacks have also been capturing headlines in the second half of 2020 with increased attacks on trusted suppliers such as Solarwinds, Microsoft, FireEye and Accellion, among others.

Early in the COVID-19 pandemic we also saw increased trends in phishing and malware, a development that has amplified overall cyber threat level.

In September 2020, we issued a discussion paper titled Developing Financial Sector Resilience in a Digital World: selected themes in technology and related risks. Accompanied by a three-month public consultation, this paper shared our thinking and recent work on technology risk—spanning operational risk and resilience, cyber security, advanced analytics, data, and the third-party ecosystem—and invited feedback to help develop regulatory guidance and supervisory approaches in these areas. The feedback we received from our stakeholders will help us draft a technology and cyber risk guideline, which we plan to issue for consultation later in 2021.

Culture

An organization's culture can influence the effectiveness of its risk management, potentially leading to excessive risk-taking and negative financial and reputational outcomes. As a prudential regulator, understanding the impact of culture—for example, on decision-making behaviour—can provide an early warning and help prevent or minimize events that can ultimately weaken an institution's operational resilience, leading to an erosion of public confidence.

In 2020, we began culture-focused supervisory reviews targeting strategic decisions. These reviews provide insights into behavioural indicators such as transparency and communication, diversity of thought, ability to provide challenge and reflective learning.

Compensation, incentives and rewards remain a focus for OSFI as key drivers of organizational behaviour and culture. We are a member of the Financial Stability Board's (FSB) Compensation Monitoring Contact Group (CMCG), which monitors and reports on implementation of the FSB's Principles and Standards for sound compensation practices. We issued a CMCG survey questionnaire to select FRFIs to gather information on compensation practices, including non-financial measures and impacts related to COVID-19. The FSB is expected to publish its biennial progress report in late 2021 using the results of this survey.

Elevated people risks as a result of the pandemic have been a key focus of our risk monitoring. Prolonged working from home compounded by isolation due to social distancing requirements has led to heightened stress and anxiety—and an increased risk of misconduct due to financial pressure. Some FRFIs implemented more frequent and targeted employee surveys for insights into employee sentiment to better monitor their people risk. We continue to monitor FRFIs' responses to maintaining organizational norms, values and behaviors during the pandemic period.

Compliance

The pandemic has highlighted the importance of organizational change in evolving, adapting and remaining competitive in an ever-changing and uncertain environment.

Execution risk in relation to regulatory compliance continues to be an area of ongoing monitoring in the current remote working environment. COVID-19 has exacerbated execution risk in relation to FRFI regulatory transformation initiatives and readiness projects, the progress of remediation activities and in light of their cost-containment measures.

Since 2020, we have also introduced "culture of compliance" as an area of focus in the scope of our regulatory compliance management reviews.

Operational Resilience

The onset of COVID-19 saw financial institutions rapidly move to remote working, which placed pressure on their operations, technology, staff, processes, controls and suppliers and caused many to invoke their crisis management plans. By and large, however, the pandemic demonstrated that the Canadian financial services sector has a strong baseline of operational resilience, given that there were no significant disruptions to critical operations.

We learned some important lessons about how FRFIs manage through disruption, including the need for up-to-date, well-tested business continuity plans and crisis playbooks that consider a wide range of possible scenarios and action plans. It is important to note that these lessons appear to be specific to the pandemic, which had a limited impact on many services and did not test institutions' ability to provide critical services during multiple concurrent disruptive events.

In response, we focused on monitoring the development and comprehensiveness of financial institutions' scenario testing, as well as how the transition to the "new normal" may impact operational resilience.

As a member of the Basel Committee on Banking Supervision, OSFI also participated in the work that led to the publication of the revised Principles for the Sound Management of Operational Risk and the new Principles for Operational Resilience in March 2021. Finally, OSFI articulated certain aspects of operational resilience in its September 2020 discussion paper, Developing Financial Sector Resilience in a Digital World.

Third-Party Risk

In September 2020 we published an infographic, Strengthening Third-Party Risk Management (PDF), which featured five focus areas that can contribute to effective management of third-party risk. These areas are the result of an earlier study that highlighted trends in third-party risk, including:

- Increasing use by financial institutions of third-party providers, including offshore providers;

- Rising concentration risk driven by dominant cloud service providers and the trend of offshore outsourcing to a limited group of countries with lower-cost skilled labour; and

- Increasing use of fourth and further parties.

COVID-19 has exacerbated these trends, as the pandemic accelerated the pace of digitalization and the move to cloud computing. Furthermore, the pandemic highlighted the importance of having current information on third parties, well-tested business continuity plans that take into account third parties and strong third-party risk identification and monitoring processes as well as effective key risk indicators. During 2020-21, understanding the quality of institutions' third-party risk management processes was an area of focus.

Demographic changes

As a broader systemic risk facing the Canadian financial system, demographic shifts in Canada—namely, the increasing average age of the population—have the potential to create stress for the insurers we regulate.

The world's population is expected to peak at the end of the 21st century, then begin declining. There is increasing concern globally regarding the societal impacts of aging populations, including government policy and quality of life at older ages.

In 2020-21 our Insurance Supervision Sector created a working group—the Aging Population Project—to study the impact of this demographic trend on the Canadian insurance industry. This working group interviewed life insurers and reinsurance firms. It also sought input from non-insurers such as the Society of Actuaries, Canadian civil society groups and—since the impact of aging has been most profound in Japan thus far—the Japanese Financial Services Authority.

Preliminary conclusions from the Aging Population Project's work include the following insights:

- Canada's population is aging, particularly in the next 10 years, although the impact will not be as severe as is expected in many other countries;

- With the exception of interest rates, insurers anticipate there will be more benefits than challenges arising from the aging population, with time to anticipate and address the impacts;

- The link between interest rates and aging populations is challenging to measure, although data and research point to a correlation in Canada; and

- A prolonged period of low (and even lower) interest rates and declining investment returns could become increasingly likely. This will continue to present significant challenges to the insurance industry going forward.

Increased digitalization

Quite apart from the technology and cyber security risks facing financial institutions (see Technology and Cyber Security Risks earlier in this section), the increased adoption of digital technologies by all segments of the economy has the potential to affect the FRFIs we regulate. For example, increasing numbers of consumers are opting to use payment platforms that lie outside the regulated financial system.

Digital technologies are transforming the financial sector and giving rise to greater competition between federally regulated financial institutions and emerging—and often unregulated—financial technology (fintech) providers. There is a risk that these new providers may create strategic risk that can destabilize the established FRFIs that make up the foundation of the financial services marketplace and threaten the viability of their business models, potentially leading to insolvencies that could undermine financial stability in Canada.

One way these digital technologies have manifested themselves is in the "disintermediation" of financial services. Whereas most FRFIs offer integrated, one-stop services such as credit cards, mortgages and savings accounts, fintech providers may disaggregate or disintermediate those services to focus on one niche and provide one service. This phenomenon fragments the consumer base for traditional FRFIs' products and services, and thus may create prudential concerns by impacting their capital, earnings and other measures of financial health. Such developments, which FRFIs would need to manage internally, could have an adverse impact on depositors, policyholders and creditors as well as financial stability in Canada writ large.

As part of our Near-Term Plan of Prudential Policy Development released on May 6, 2021—slightly after the period covered by this annual report—we made a commitment to providing a draft guideline on technology and cyber risks in late 2021. This guideline will take into consideration some of the issues surrounding the trend toward increased digitization and the risks associated with disintermediation.

Non-bank financial intermediation

In a similar vein to increased digitization, we are monitoring the risks arising from non-bank financial intermediation (NBFI) as another potential area where FRFIs' business models may face increased competition.

Although NBFI is not covered by OSFI's mandate, its implications for financial stability have the potential to be wide-ranging even though the sector makes up just a small portion—approximately 10.9%—of Canada's financial system.

While investment funds were the largest NBFI subsector, accounting for 45% of NBFI assets, since 2008 financing companies have shown strong growth with an average annual growth rate of 5%. These financing companies vary from crowd-funded debt platforms and vendor-issued consumer loans for big-ticked purchases, to credit cards and mortgage loans offered by non-DTIs.

OSFI'S WORK: Deposit-Taking Institutions

We regulate and supervise deposit-taking institutions (DTIs) including domestic and foreign banks, foreign bank branches, trust and loan companies, and federal credit unions.

The federally regulated deposit-taking industry in Canada is comprised of six large domestic banks that have been designated as domestic systemically important banks (D-SIBs), four mid-tier institutions, and many smaller institutions. The Financial Stability Board has also designated two of the D-SIBs as global systemically important banks.

D-SIBs account for about 93 percent of total assets held by federally regulated DTIs in Canada. Their diversified business activities include deposit-taking and lending, trading, investment banking, wealth management and insurance. In addition to their primary domestic focus, most of the D-SIBs operate in other jurisdictions including the United States, United Kingdom, Europe and the Americas.

Small and medium-sized institutions account for the remainder of total assets held by federally regulated DTIs. These institutions engage in various businesses and markets such as mortgage lending, commercial real estate lending and credit card lending.

We closely monitor the financial and non-financial risks facing deposit-taking institutions, including system-wide or sector developments that could have a negative impact on their financial condition.

Deposit-Taking Institutions Environment

The COVID-19 pandemic created a challenging environment for DTIs. The Government of Canada, including OSFI, took extraordinary measures to support the economy, financial markets and DTIs' ongoing resilience throughout this period of uncertainty in 2020-21.

At the outset of the pandemic Canada's DTIs were well placed in terms of capital and liquidity, and had prepared measures such as business continuity plans that enhanced their operational resilience. This strong position served them well as the pandemic worsened and the economic impact was more profoundly felt.

These DTIs were also able to effectively manage loan deferrals offered during the initial phase of the pandemic with no impact on capital. While there were initial concerns of a "deferral cliff" looming, no such problems have materialized to date. On the liquidity side, liquidity levels actually improved as Canadians increased their deposit levels with Canadian DTIs. This increase in deposit levels reflected the government support provided to Canadian consumers and businesses through the pandemic.

Our supervisory activities related to DTIs focused on key areas such as operational resilience, capital, liquidity and credit risk. Particular subjects of interest included payment deferral programs, delinquencies and allowance for credit losses. Monitoring of technology risk, including cyber security threats, was heightened in 2020-21 given the pandemic and work-from-home environment. We will continue to monitor the financial and non-financial risks posed by the current environment.

Sound Mortgage Underwriting

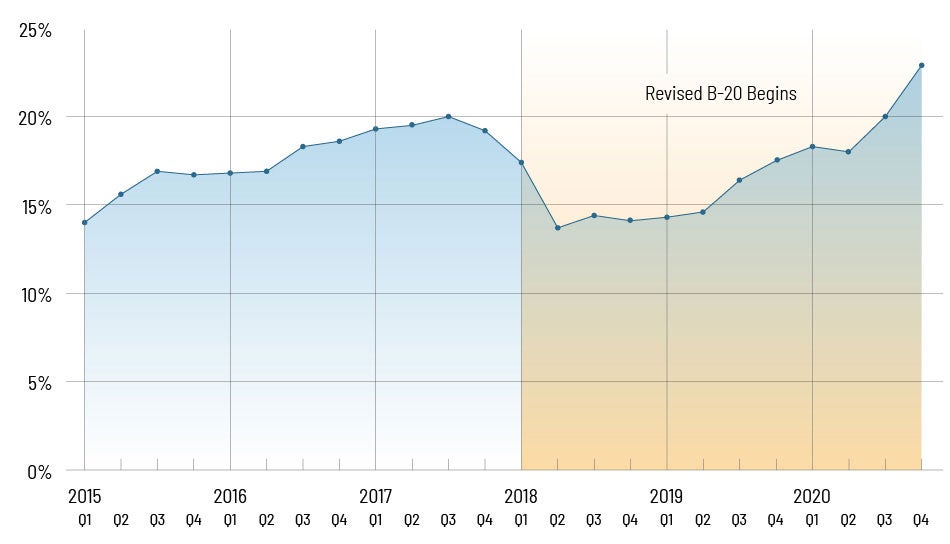

In 2020-21 we acted to promote sound mortgage underwriting practices that reduce the risks to the financial system. Specifically, our supervisory reviews of deposit-taking institutions ensured that the institutions had appropriate standards and adequate controls to assess a borrower's ability to pay their loan under a variety of conditions.

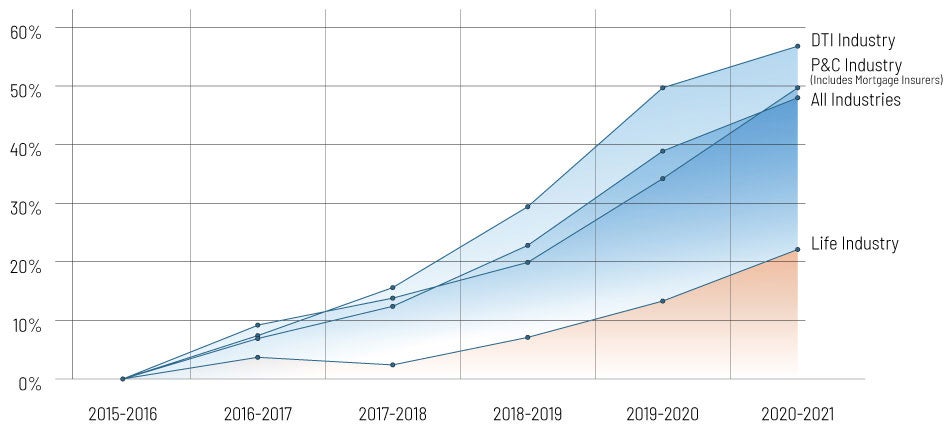

Graphic description - Loan to income greater than 450%

| Fiscal quarter | Percentage |

|---|---|

| 2015 Q1 | 14.0% |

| 2015 Q2 | 15.6% |

| 2015 Q3 | 16.9% |

| 2015 Q4 | 16.7% |

| 2016 Q1 | 16.8% |

| 2016 Q2 | 16.9% |

| 2016 Q3 | 18.3% |

| 2016 Q4 | 18.6% |

| 2017 Q1 | 19.3% |

| 2017 Q2 | 19.5% |

| 2017 Q3 | 20.0% |

| 2017 Q4 | 19.2% |

| REVISED B-20 BEGINS | |

| 2018 Q1 | 17.4% |

| 2018 Q2 | 13.7% |

| 2018 Q3 | 14.4% |

| 2018 Q4 | 14.1% |

| 2019 Q1 | 14.3% |

| 2019 Q2 | 14.6% |

| 2019 Q3 | 16.4% |

| 2019 Q4 | 17.5% |

| 2020 Q1 | 18.3% |

| 2020 Q2 | 18.0% |

| 2020 Q3 | 20.0% |

| 2020 Q4 | 22.9% |

In February 2020 we launched consultations on the B-20 minimum qualifying rate for uninsured mortgages, which were subsequently suspended in March 2020 due to the COVID-19 pandemic. In April 2021, just after the end of the 2020-21 fiscal year covered by this annual report, we released a new proposal for the rate: the higher of the mortgage contract rate plus 2%, or 5.25%. This new rate was implemented on June 1, 2021 and will be reviewed annually at a minimum.

The Domestic Stability Buffer

Supporting the resilience of Canada's banking system

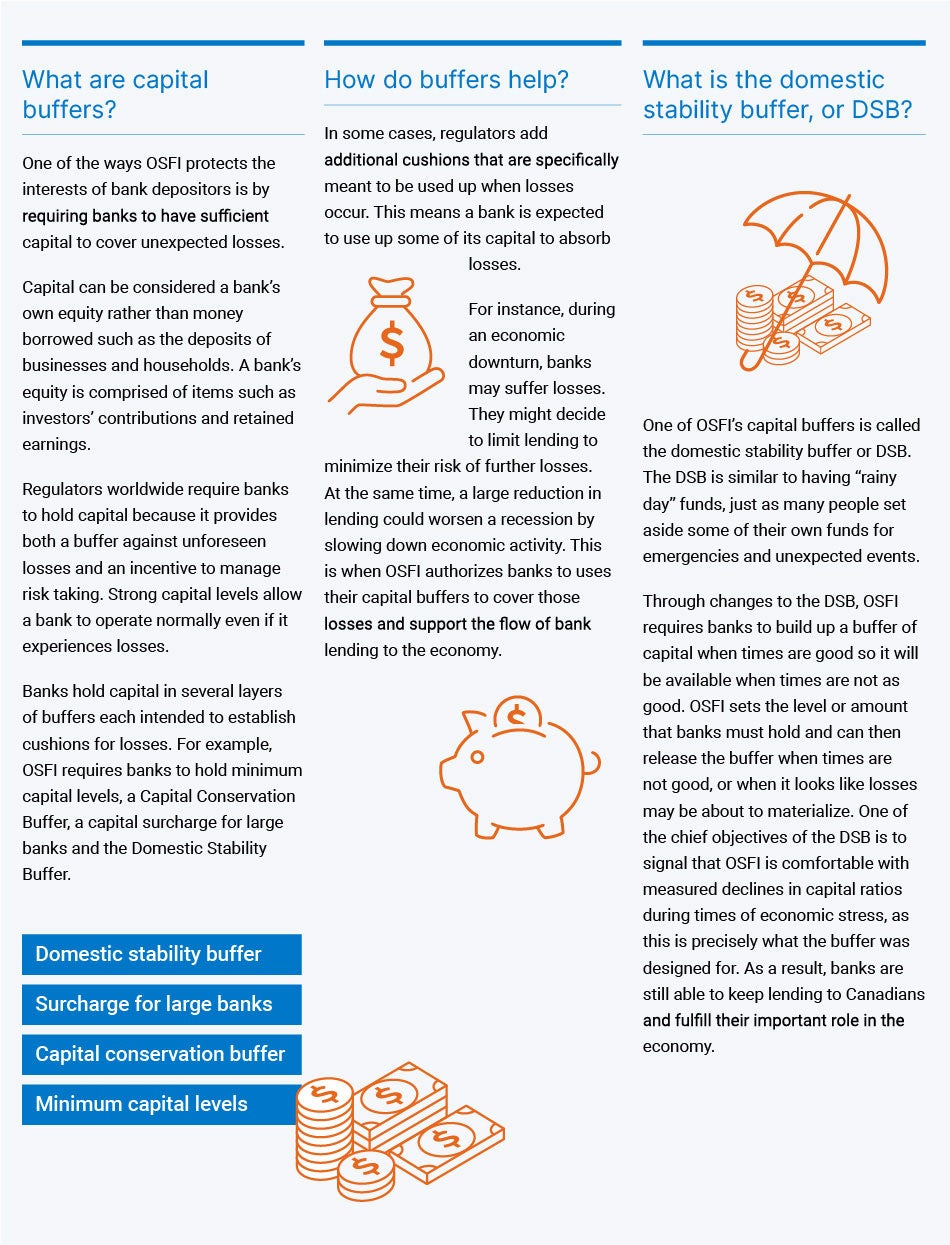

Graphic description - The Domestic Stability Buffer Infographic

What are capital buffers?

One of the ways OSFI protects the interests of bank depositors is by requiring banks to have sufficient capital to cover unexpected losses. Capital can be considered a bank's own equity rather than money borrowed such as the deposits of businesses and households. A bank's equity is comprised of items such as investors' contributions and retained earnings.

Regulators worldwide require banks to hold capital because it provides both a buffer against unforeseen losses and an incentive to manage risk taking. Strong capital levels allow a bank to operate normally even if it experiences losses.

Banks hold capital in several layers of buffers each intended to establish cushions for losses. For example, OSFI requires banks to hold minimum capital levels, a Capital Conservation Buffer, a capital surcharge for large banks and the Domestic Stability Buffer.

How do buffers help?

In some cases, regulators add additional cushions that are specifically meant to be used up when losses occur. This means a bank is expected to use up some of its capital to absorblosses. For instance, during an economic downturn, banks may suffer losses. They might decide to limit lending to minimize their risk of further losses. At the same time, a large reduction in lending could worsen a recession by slowing down economic activity. This is when OSFI authorizes? banks to use their capital buffers to cover those losses and support the flow of bank lending to the economy.

What is the domestic stability buffer, or DSB?

One of OSFI's capital buffers is called the domestic stability buffer, or DSB. The DSB is similar to having "rainy day" funds, just as many people set aside some of their own funds for emergencies and unexpected events.

Through changes to the DSB, OSFI requires banks to build up a buffer of capital when times are good so it will be available when times are not as good. OSFI sets the level or amount that banks must hold and can then release the buffer when times are not good, or when it looks like losses may be about to materialize. One of the chief objectives of the DSB is to signal that OSFI is comfortable with measured declines in capital ratios during times of economic stress, as this is precisely what the buffer was designed for. As a result, banks are still able to keep lending to Canadians and fulfill their important role in the economy.

The Domestic Stability Buffer (DSB) is a capital buffer requirement for domestic systemically important banks (D-SIBs). During challenging times the DSB's countercyclical design enables D-SIBs to use the capital they set aside during more stable economic conditions.

In March 2020, a series of coordinated announcements in response to the uncertainty caused by COVID-19 for Canada's financial system were made in an unprecedented news conference with the Minister of Finance, the Governor of the Bank of Canada and the Superintendent of Financial Institutions. At that news conference, the Superintendent announced the lowering of the DSB by 1.25% of risk-weighted assets, from 2.25% to 1.00%.

The lowering of the DSB supported more than $300 billion in additional lending capacity for the D-SIBs, allowing them to supply credit to the economy during an unexpected period of disruption. We also committed to not increasing the buffer for at least 18 months and signalled our readiness to lower the DSB further if conditions required.

Our June and December 2020 decisions to maintain the DSB at 1% of total risk-weighted assets were based on our assessment that this level remained effective in supporting banking system resilience. This stance was supported by an upward trend in banks' capital levels and strength in pre-provision net revenues, as well as indications that banks were continuing to lend to Canadians.

Canadian banks demonstrated resilience throughout the pandemic in 2020-21, and were well-supported by government programs, monetary policy actions and regulatory relief measures.

The next scheduled DSB announcement was held on June 17, 2021 – after the period covered by this annual report – at which time the DSB was raised to 2.5% of total risk-weighted assets. The process to review the DSB level is ongoing and our focus is on evaluating recent conditions and the status of key vulnerabilities and risks.

Response to COVID-19 - Deposit-Taking Institutions

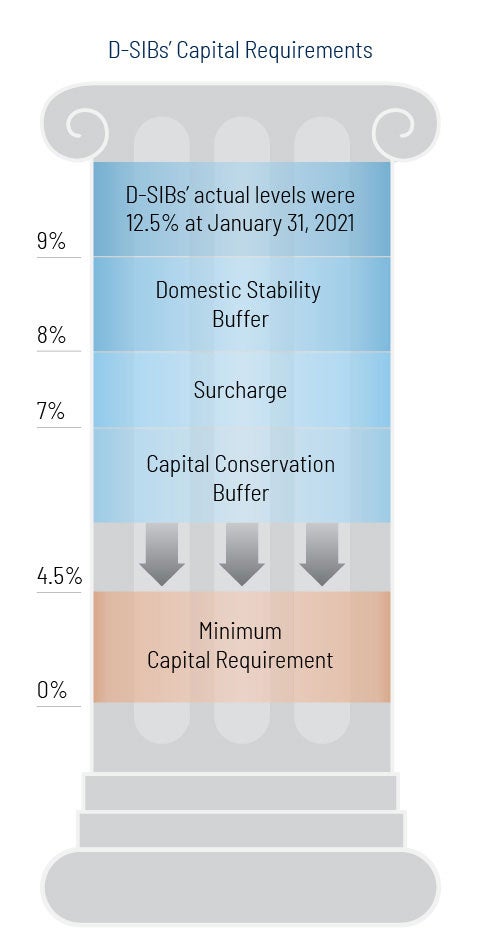

Graphic description - Big Banks Capital Requirements

D-SIBs' Capital Requirements

- 0% to 4.3% Minimum Capital Requirement

- 4.3% to 7.0% Capital Conservation Buffer

- 7.0% to 8.0% Surcharge

- 8.0% to 9.0% Domestic Stability Buffer

D-SIBs' actual levels were 12.5% as of January 31, 2021

In addition to a lower DSB level, in March and April 2020 we announced a series of regulatory adjustments to support the financial and operational resilience of federally regulated banks as COVID-19 spread across Canada. This suite of adjustments to existing capital and liquidity requirements targeted certain requirements that were not appropriate in the extraordinary circumstances created by the pandemic. We took these measures to provide institutions with further flexibility to address conditions while promoting financial resilience and stability.

Over the course of 2020-21 we provided updated guidance—and in some cases unwound certain measures altogether—as financial market conditions stabilized and institutions' operational capacity and management of the economic challenges related to the pandemic improved.

Other specific areas of action include:

-

Payment deferrals: In late August 2020 we updated our guidance on the special capital treatment of loans subject to payment deferrals to gradually phase out this treatment as institutions' positions improved. This change allowed DTIs to employ their business-as-usual alternatives to support troubled borrowers.

- Leverage ratio: In November 2020 we announced an eight-month extension for DTIs to continue to exclude central bank reserves and sovereign-issued securities from their leverage ratio exposure measures.

- Stressed VaR: In March 2021 we announced that federally regulated DTIs subject to market risk requirements should restore their Stressed Value-at-Risk (SVaR) multipliers to levels in place prior to spring 2020.

- Covered bonds: On April 6, 2021—just after the end of the 2020-21 fiscal year covered by this annual report—we announced the immediate unwinding of regulatory relief related to the covered bond limit.

Guidance - Deposit-Taking Institutions

Through our regulation, we play an important oversight role by developing guidelines, policies and procedures for institutions designed to control and manage risk. We balance safety and soundness with institutions' need to take reasonable risks and compete.

In March 2021, we launched a public consultation on revisions to the Capital Adequacy Requirements (CAR) Guideline, Leverage Requirements (LR) Guideline and Liquidity Adequacy Requirements (LAR) Guideline, with a view to implementing these changes in early 2023. The proposed revisions to the CAR and LR guidelines reflect our domestic implementation of the final Basel III reforms. All three guidelines also include proposed revisions to reflect specific capital and liquidity requirements for small and medium-sized institutions (SMSBs).

In March 2021 we also released a draft SMSB Capital and Liquidity Guideline to help stakeholders understand how the CAR, LR and LAR guidelines apply to SMSBs including deposit-taking subsidiaries of D-SIBs.

Guideline E-4: Foreign Entities Operating in Canada on a Branch Basis

In October 2020 we published our draft Guideline E-4: Foreign Entities Operating in Canada on a Branch Basis for public consultation. This draft guideline reflects the responsibilities of foreign entities and their management to oversee day-to-day operations of their Canadian businesses. It also reflects new requirements governing the location of records which came into force in July 2021 under the Bank Act. Once final, this guideline will replace the existing E-4B: Role of the Principal Officer and Record Keeping Requirements guideline.

Anti-Money Laundering/Anti-Terrorist Financing (AML/ATF)

In October 2020 we launched a consultation on our supervisory activities related to anti-money laundering/anti-terrorist financing (AML/ATF). This consultation was part of an initiative by OSFI and the Financial Transactions and Reports Analysis Centre of Canada to eliminate duplication and redundancy in how AML/ATF regulatory requirements are applied to FRFIs.

As a result of this consultation, on May 17, 2021—slightly after the period covered by this annual report—we announced that we will rescind Guideline B-8 (Deterring & Detecting Money Laundering and Terrorist Financing), effective July 26, 2021. While no amendments to Guideline E-13 (Compliance Management) will be made in the near term, we will launch a comprehensive review of this guideline in 2022.

OSFI'S WORK: Insurance

We regulate and supervise life, property and casualty and mortgage insurance companies as well as fraternal benefit societies.

The federally regulated life insurance industry in Canada is comprised of three large internationally active institutions and more than 75 domestic companies that together hold $1.8 trillion in assets. The largest life insurers offer a broad range of wealth management, life and health insurance products through a number of distribution channels, while smaller insurers are more restricted in product breadth and distribution.

We supervise 145 property and casualty (P&C) insurers. The top 10 institutions represent 69 percent or $48 billion of the gross written premium for the industry.The mortgage insurance industry in Canada consists of three participants: two private-sector insurers that we regulate and the Canada Mortgage and Housing Corporation (CMHC), a Crown corporation subject to our oversight. These mortgage insurers provide lending institutions with protection against the risk of default by borrowers and insured $721 billion in residential mortgages at the end of 2020. CMHC provides a further $500 billion of guarantees covering securitized residential mortgage pools.

A fraternal benefit society is an institution operated for fraternal, benevolent or religious purposes, including to insure its members and their spouses or children against accident, sickness, disability or death. There are 12 such societies in Canada, all of which are subject to our supervision and regulation.

We closely monitor risks that could affect insurers' financial condition. We conduct risk assessments and intervene if necessary to ensure that the industry remains prepared and resilient to financial risks during stress events.

Insurance Institutions Environment

Starting in early 2020, low long-term interest rates, COVID-19 and heightened market volatility brought increased challenges and uncertainty for the life insurance industry. Insurers managed disruptions to operations by implementing business continuity plans and other responsive measures.

Overall, the P&C industry had strong financial results in 2020, although experiences differed significantly between primary insurers and reinsurers. Reduced exposures related to stay-at-home orders, a hard market for property insurance—where premiums increase while capacity to offer coverage decreases—and commercial lines and relatively low non-catastrophe weather events have meant favourable results for primary insurers. Catastrophe weather losses, COVID-19 business interruption and liability claims and the effect of lower interest rates were the major contributors to reinsurer's poor results in 2020.

Mortgage insurers achieved relatively favourable financial results in 2020. An industry-wide decrease in underwriting income driven mainly by strengthening of reserves for potential COVID-19 related claims was offset by an overall improvement in net investment income. Capital levels also strengthened. Over the course of 2020-21, however, mortgage insurers remained vulnerable to rising consumer debt levels and the risk of a housing price correction in certain markets.

To address the rapidly evolving economic impacts of COVID-19, mortgage insurers acted to support homeowners through mortgage payment deferrals and lending institutions through insurance coverage to facilitate access to liquidity. They also introduced initiatives to ensure their own financial and operational resilience. The impact of COVID-19 on mortgage insurers during 2020-21 is complicated by the asymmetric impacts of the pandemic on vulnerable segments of the population such as renters, oil-dependent provinces and insured homeowners who are employed in lagging industry sectors. We will continue to monitor the mortgage insurance segment of the financial industry closely.

International Financial Reporting Standard (IFRS) 17

International Financial Reporting Standard 17 (IFRS 17) is an international financial accounting standard issued by the International Accounting Standards Board (IASB) in May 2017.

In June 2020 the IASB issued amendments to IFRS 17 for annual periods beginning on or after January 1, 2023. After analyzing the prudential impacts of the accounting amendments by the IASB, in September 2020 we issued a revised IFRS 17 Advisory. Canadian insurers have made a significant effort and allocated considerable resources to prepare for the new insurance contract measurement and disclosure standard. This work includes significant changes to systems, operations and financial reporting.

In fall 2020 we consulted on revised draft capital guidelines updated for IFRS 17. We also conducted another quantitative impact study (QIS) to assess insurers' capital ratios under the draft frameworks. This consultation and quantitative testing resulted in enhancements to the draft capital guidelines. In April 2021 we issued revised regulatory returns for 2023 to comply with IFRS 17, and draft versions of insurance capital guidelines for public consultation in June 2021.

Throughout 2020-21, we monitored progress made on implementing this new standard by insurance companies through our semi-annual progress reporting process. In August 2020, we provided an update to industry on milestones completed and activities underway to support the robust implementation of IFRS 17.

Response to COVID-19 - Insurance

In our March 2020 and April 2020 letters to insurers we announced capital measures offering special capital treatment for loan and insurance premium payment deferrals. Influenced by our monitoring of the evolving COVID-19 situation and our frequent dialogue with insurers, in August 2020 we announced a phasing-out of these special capital measures. We continue to monitor the impacts of COVID-19 on insurers and remain prepared to adjust our guidance as necessary.

Guidance - Insurance

Guideline E-4: Foreign Entities Operating in Canada on a Branch Basis

In October 2020, we published draft Guideline E-4: Foreign Entities Operating in Canada on a Branch Basis for public consultation. This proposed guideline better reflects the responsibilities of foreign entities and their management to oversee day-to-day operations of their Canadian businesses. It also reflects new requirements governing the location of records which came into force in July 2021 under the Insurance Companies Act. Once final, this guideline will replace the existing E-4A Role of the Chief Agent and Record Keeping Requirements guideline.

Reinsurance

Reinsurance is essentially insurance for insurance companies. A comprehensive review of reinsurance practices has been a key OSFI initiative over the past few years. In June 2018 we issued a discussion paper including proposals to enhance and clarify expectations for prudent reinsurance practices and in June 2019 we issued a revised B-3 - Sound Reinsurance Practices and Procedures guideline.

Building on this work, in November 2020 we issued a draft B-2 - P&C Large Exposures and Investment Limits guideline. Both the B-3 and B-2 guidelines reflect valuable feedback received during consultations as well as ongoing discussions with industry. We will issue final B-3 and B-2 guidelines in tandem by December 2021.

Capital Guidance

In November 2020 we released an advisory to formally include in the Life Insurance Capital Adequacy Test (LICAT) framework a smoothing technique for determining interest rate risk (IRR) requirements for participating business (par). Also included in the advisory is clarification of our expectations related to negative DSRs (Dividend Stabilization Reserves or other similar experience leveling mechanisms).

We also continued to develop a new approach for determining capital requirements for segregated fund guarantee (SFG) risk which will reflect IFRS 17. The new approach comes into effect on January 1, 2023 and will replace the current Chapter 7 of the Life Insurance Capital Adequacy Test (LICAT) guideline.

As part of this development work, in December 2020 we launched a consultation of the draft approach as well as a quantitative impact study and sensitivity tests. Submissions were due on March 31, 2021 and are being used to assess whether further refinements to the methodology are necessary.

OSFI'S WORK: Private Pension Plans

We regulate and supervise more than 1,200 federally regulated private pension plans in federally regulated areas of employment such as banking, inter-provincial transportation and telecommunications. These plans include more than 1.18 million active members and other beneficiaries, and hold assets of about $260.5 billion.

We develop guidance on risk management and mitigation, assess whether plans are meeting their funding requirements and managing risks effectively, and intervene promptly if we identify a need for corrective action. Administrators are ultimately responsible for sound and prudent management of their pension plans.

| Plans Subject to the Pension Benefits Standards Act, 1985 | 2020 | 2021 | |

|---|---|---|---|

| Number of Plans | Defined Benefit | 271 | 268 |

| Combination | 122 | 119 | |

| Defined Contribution | 817 | 826 | |

| Total | 1,210 | 1,213 | |

| Active Membership | Defined Benefit | 203,400 | 173,800 |

| Combination | 306,600 | 330,500 | |

| Defined Contribution | 144,900 | 149,200 | |

| Total | 654,900 | 653,500 | |

| Other Beneficiaries | Defined Benefit | 260,900 | 236,400 |

| Combination | 243,400 | 272,300 | |

| Defined Contribution | 21,000 | 22,200 | |

| Total | 525,300 | 530,900 | |

| Assets ($ millions) | Defined Benefit | 118,000 | 119,800 |

| Combination | 113,500 | 131,100 | |

| Defined Contribution | 8,700 | 9,600 | |

| Total | 240,200 | 260,500 | |

Private Pension Plan Environment

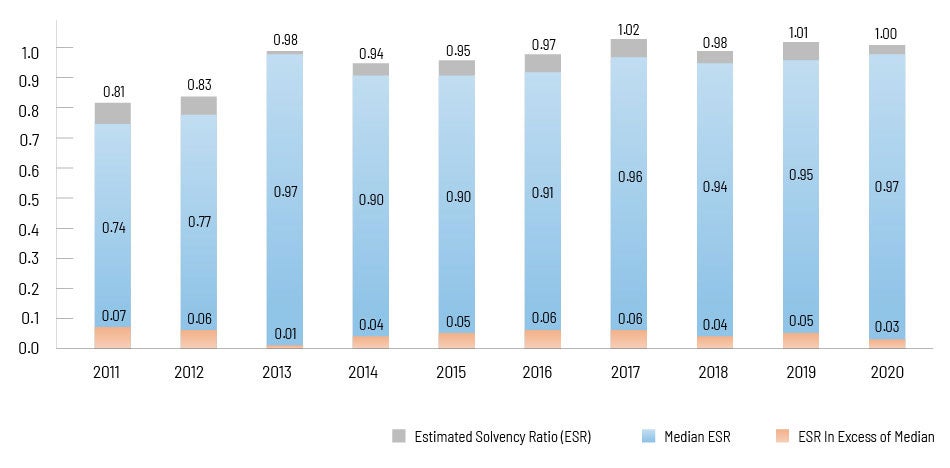

In the first quarter of 2020 the COVID-19 pandemic affected both defined benefit and defined contribution plans. The overall solvency position of defined benefit plans deteriorated significantly at the outset of the pandemic as a decline in equity markets reduced asset values and the continued drop in bond yields increased liabilities. However, the last quarter of 2020 saw equity market returns improve, which helped offset most of the first-quarter decline. By the end of 2020, this resulted in the overall solvency position of pension plans returning to levels similar to those seen at the beginning of the year.

Under the Pension Benefits Standards Act, 1985, solvency funding requirements for plans with defined benefit provisions are based on a plan's three-year average solvency position. This means that the 2020 solvency ratio replaces the 2017 value in calculating the average solvency position. The three-year average solvency position of pension plans is similar to what it was last year. As a result, without taking into account the solvency funding relief available in 2020 described in the next paragraph, plans on average should not need to increase their required solvency funding payments for 2021 above 2020 payment levels.

In April 2020, the Department of Finance announced the Solvency Special Payments Relief Regulations, which established a moratorium on certain solvency special payments due during the period beginning on April 1, 2020, and ending on December 30, 2020. This moratorium took effect in May 2020.Based on the Solvency Information Returns filed by pension plans in February 2021, 18% of plans with defined benefit provisions took solvency funding relief in 2020 for a total amount of $955 million. More than two-thirds (68%) of these plans reduced their solvency special payments for the entire period of the moratorium.

Graphical Description - Solvency Position of Pension Plans as at December 31, 2020

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|---|---|---|

| Median ESR | 0.74 | 0.77 | 0.97 | 0.90 | 0.90 | 0.91 | 0.96 | 0.94 | 0.95 | 0.97 |

| Estimated Solvency Ratio (ESR) | 0.81 | 0.83 | 0.98 | 0.94 | 0.95 | 0.97 | 1.02 | 0.98 | 1.01 | 1.00 |

| ESR in excess of Median | 0.07 | 0.06 | 0.01 | 0.04 | 0.05 | 0.06 | 0.06 | 0.04 | 0.05 | 0.03 |

Response to COVID-19 - Private Pension Plans

In response to COVID-19, we adjusted our policies to continue to protect the interests of pension plan members and beneficiaries, and to allow plan administrators to focus on addressing challenges posed by the pandemic. In addition to extending filing deadlines and suspending a number of consultations and policy development initiatives, we implemented a temporary freeze on portability transfers and annuity purchases relating to defined benefit provisions of pension plans.

By September 2020, we lifted the temporary portability freeze subject to certain conditions. Previously suspended work on developing pension-related guidance had also resumed.

We kept pension plan stakeholders aware of the measures we took to protect plan members and beneficiaries through information posted on our website and through technical briefings. Communication and feedback from stakeholders, as well as information-sharing initiatives with other regulators, proved crucial in developing an effective policy response to COVID-19.

In addition, we increased our monitoring in the areas of risk management, employers' ability to make contributions, business continuity, and employers operating in sectors highly impacted by the crisis. From late March until the end of December 2020 we frequently calculated the estimated solvency ratio of the defined benefit pension plans we regulate. This allowed us to stay on top of the impact of volatility in the financial and economic environment.

In response to these measures plan members, administrators and other industry stakeholders submitted an unprecedented number of enquiries. By the end of December 2020 we responded to nearly 500 written enquiries on these measures. In addition, we received close to 90 requests for the Superintendent's consent to allow for portability transfers or annuity purchases.

Risk-Based Reviews

We advanced our work on two major projects in 2020-21 to identify areas where we can strengthen our principles- and risk-based approach to pension plan supervision.

As part of our review of how we supervise pension plan investments, we worked with plan administrators and pension investment consultants to better understand the factors driving the shift towards non-traditional investments, including leveraged investment strategies and private market assets. Analysis of data collected through a pension investment questionnaire permitted a deeper understanding of the nature and level of inherent pension investment risks, as well as the form and quality of risk management practices. Risk management gaps identified through this review will inform our supervisory approach to pension investments and regulatory expectations.

The second major project we advanced in 2020-21 assessed how we supervise plans with defined contribution provisions. The Financial Services Regulatory Authority of Ontario (FSRA) and OSFI together established a special purpose committee to review our respective approaches to supervising defined contribution plans and, where possible, find opportunities for regulatory harmonization. Through this collaboration, FSRA and OSFI will work towards improving outcomes for plan members and enhancing regulatory efficiency and effectiveness for defined contribution plans.

We also continued work on two additional initiatives related to emerging risks faced by pension plans: a review of the consideration of environmental, social and governance (ESG) factors in plan investment decisions, and the analysis of the potential risks associated with technology, including cyber and third-party risk.

While these reviews and initiatives are still ongoing based on preliminary findings, we expect recommendations to include adjusted annual reporting requirements and/or updated guidance.

| Asset Class | 2019 | 2020 | ||

|---|---|---|---|---|

| $ Millions | % | $ Millions | % | |

| Debt securities and cash | 122,632 | 51.1 | 124,587 | 47.8 |

| Equity | 88,999 | 37.1 | 92,926 | 35.7 |

| Diversified investments | 13,472 | 5.6 | 15,021 | 5.8 |

| Other investments | 38,786 | 16.1 | 47,730 | 18.3 |

| Accounts receivable net of liabilities | (23,689) | -9.9 | (19,729) | -7.6 |

| TOTAL NET ASSETS | 240,200 | 100.0 | 260,535 | 100.0 |

Asset breakdown of private pension plans table footnotes

|

||||

Actuarial Reports

We review actuarial reports for defined benefit plans, and conduct a more in-depth review of these reports where risks are noted. Nearly 290 actuarial reports were filed with us in 2020-21 — approximately 20% of these were subjected to a more in-depth review. Any issues revealed during an in-depth review are raised with plan actuaries, particularly when these concerns have an impact on current and future funding requirements. Our interventions have resulted in some plans being required to amend and re-submit their actuarial reports.

Examinations

During 2020-21, to allow plan administrators to focus their efforts on addressing challenges posed by the COVID-19 pandemic, we suspended all but one examination being conducted as part of our risk-based supervisory approach. We expect to resume examinations in 2021-22 with a focus on desk reviews.

Guidance

In September 2020 we resumed our consultation on the draft revisions to the Instruction Guide for the Preparation of Actuarial Reports for Defined Benefit Pension Plans. The final guide was posted in November 2020.

In November 2020 we resumed our consultation on the draft revisions to the Instruction Guide for the Termination of a Defined Benefit Pension Plan and began consultations on the Instruction Guide for the Termination of a Defined Contribution Pension Plan. The final guides for both defined benefit and defined contribution plans were posted in May 2021.

In December 2020 we posted an Instruction Guide for Filing Plan Amendments Using the Regulatory Reporting System (RRS) as well as the revised OSFI 593: Defined Contribution Pension Plan Amendment Information Form and OSFI 594: Defined Benefit/Combination Pension Plan Amendment Information Form.

Throughout the first quarter of 2021, we issued revised instruction guides and forms to improve the quality and usefulness of data collected and assist plan administrators in completing and submitting annual regulatory filings. Revisions were made to the instruction guides and accompanying forms for completing and filing the Solvency Information Return (SIR), the Actuarial Information Summary (AIS) and the Replicating Portfolio Information Summary (RPIS).

Although scheduled for publication in May 2020, InfoPensions 23 was postponed until November 2020 due to the pandemic. This regular newsletter includes announcements and reminders for plan administrators, pension advisors and other stakeholders as well as descriptions of how we apply provisions of the pension legislation and its guidance. The November 2020 edition also provided an update on measures taken in response to COVID-19.

Approvals

Federally regulated private pension plans are required to seek our approval for several types of transactions, including plan registrations and terminations, asset transfers between registered defined benefit pension plans, refunds of surplus and reductions of accrued benefits.

In 2020-21, 31 such pension transactions were submitted for approval, compared to 40 in 2019-20. We processed 37 applications for approval in 2020-21, compared to 42 the previous year.

In 2020-21, 10 new plans were registered (two defined benefit/combination plans and eight defined contribution plans), 10 plan termination reports were approved (eight defined benefit/combination plans and two defined contribution plans) and nine defined benefit asset transfer requests were authorized.

| Approvals | Cases Processed | |||||

|---|---|---|---|---|---|---|

| Fiscal Year | Cases Submitted | Total | Registrations | Terminations | DB Asset Transfers | Other |

| 2018-2019 | 63 | 47 | 14 | 16 | 12 | 5 |

| 2019-2021 | 40 | 42 | 16 | 19 | 1 | 6 |

| 2020-2021 | 31 | 37 | 10 | 10 | 9 | 8 |

OSFI'S WORK: Regulation

In addition to creating, implementing and enforcing regulatory guidance and expectations to the industries we supervise, we regulate by interpreting legislation and providing approvals for some transactions.

Legislation

The federal statutes governing financial institutions generally restrict the use of words that could lead a person to believe that a company or business is a federal financial institution when it is not. We may, however, approve the use of such words in certain circumstances by entities that are not federally regulated financial institutions.

In order to enhance transparency and efficiency in this approval process, in December 2020 we published a webpage that provides an application form for such approval requests as well as responses to frequently asked questions on this subject.

Approvals

The Bank Act, Trust and Loan Companies Act and Insurance Companies Act require federally regulated financial institutions to seek regulatory approval from OSFI or the Minister of Finance prior to engaging in certain transactions or business undertakings.Regulatory approval is also required by persons wishing to incorporate an institution, and by foreign banks or foreign insurance companies wishing to establish a presence or to make certain investments in Canada.

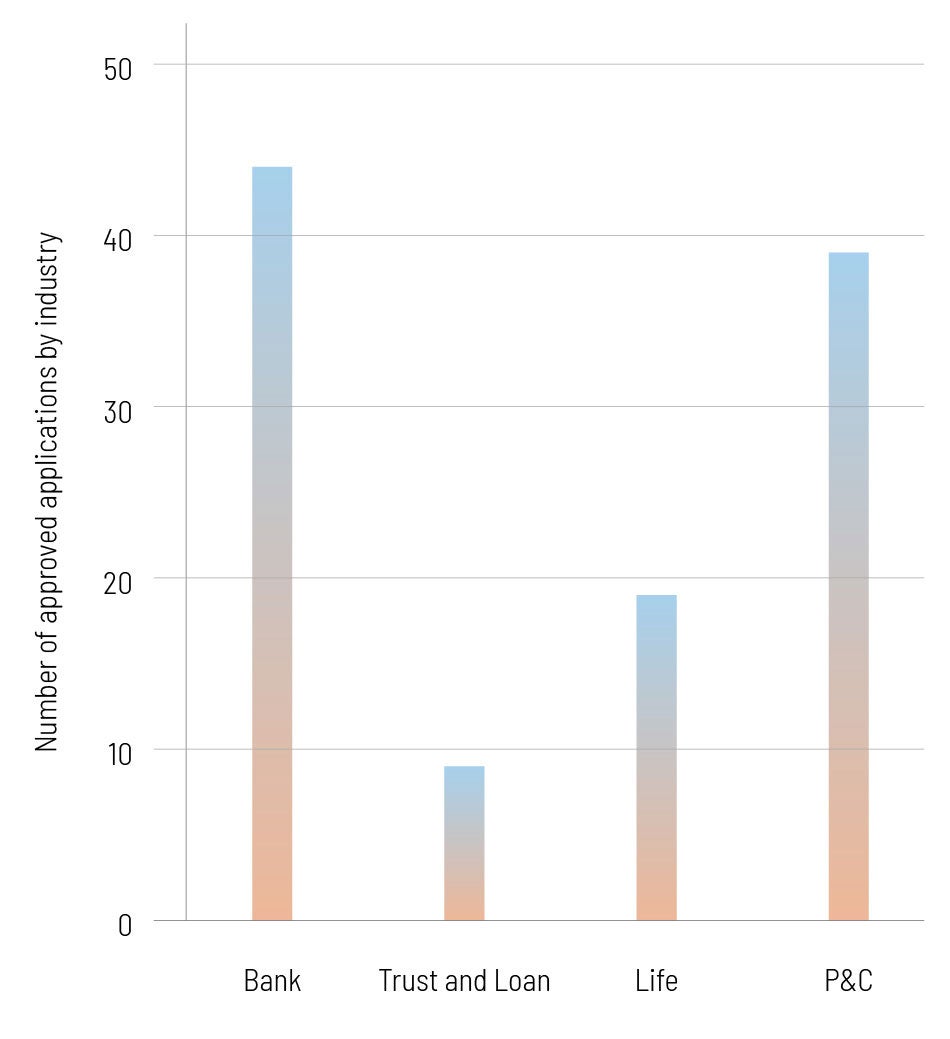

Graphic description - Number of Approved Applications from Federally Regulated Financial Institutions

| Approved Applications | |

|---|---|

| Bank | 44 |

| Trust and Loan | 9 |

| Life | 19 |

| P&C | 39 |

In 2020-21 we processed 123 applications of this nature, 111 of which were approved and 12 of which were withdrawn. The majority of approved applications are related to banks (40%) and P&C insurers (35%).

The most common applications processed from DTIs were for purchases or redemptions of shares or debentures, transfers of assets in excess of 10 percent, exemption from requirements for solicitation of proxies and substantial investments.

For insurance companies, the most common applications were for purchases or redemptions of shares or debentures, amending orders to commence and carry on business or insure in Canada risks, and non-cash consideration for shares.

Regulatory approval and letters patent were granted to PNB Trust, allowing it to incorporate as a trust company. In addition, orders to insure in Canada risks under the Insurance Companies Act were issued to Shelter Mutual Insurance Company and Hudson Insurance Company, establishing them as foreign insurance branches in Canada.

Upon request, we also provide advance capital confirmations on the eligibility of proposed regulatory capital instruments. We provided a total of 27 such opinions and validations in 2020-21, compared to 21 in the previous year.

We have performance standards that establish timeframes for processing applications for regulatory approvals and for other services, all of which were met during the year. More information on service standards is located at the Application and Approvals section of our website.

OSFI'S WORK with Partners

Canada's financial system is one of the safest and strongest in the world. This is due in part to effective financial sector policy, regulation and supervision, liquidity support, deposit insurance, recovery and resolution strategies and consumer protection and financial education.

Domestic

Oversight of Canada's Financial System

Graphic description - Oversight of Canada's Financial System

- Office of the Superintendent of Financial Institutions

- Bank of Canada

- Department of Finance Canada

- Canada Deposit Insurance Corporation

- Financial Consumer Agency of Canada

We report to Parliament through the Minister of Finance and work closely with federal partners, including the Department of Finance, the Bank of Canada, the Canada Deposit Insurance Corporation (CDIC) and the Financial Consumer Agency of Canada. We also work with the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) and consult with provincial counterparts and industry stakeholders.

In 2020-21 we continued to hold regular meetings with our partners and industry stakeholders despite the COVID-19 pandemic. We also participated in an annual crisis management exercise with CDIC to assess institutional preparedness.

Domestic Accounting, Auditing and Actuarial Standards

Our supervision and regulation of financial institutions relies on high-quality audited financial statements. For this reason, we actively participate in domestic standard-setting and oversight bodies related to Canadian auditing and accounting standards.

In September 2020, we co-hosted a virtual meeting on audit quality with the Canadian Public Accountability Board (CPAB). The forum provided an opportunity for more than twenty-five of Canada's public accounting and regulatory leaders to discuss ways to support continued financial system stability by enhancing public confidence in audit quality.

In 2020-21, we continued to participate in the CIA IFRS 17 steering committee and several CIA standards and guidance committees. We also participated in two Actuarial Standards Board (ASB) designated groups related to the implementation of IFRS 17, including the impact on the role of the actuary.

Canadian Association of Pension Supervisory Authorities

We are a member of the Canadian Association of Pension Supervisory Authorities (CAPSA), a national association of pension regulators with a mission to facilitate an efficient and effective pension regulatory system in Canada.

CAPSA developed the 2020 Agreement Respecting Multi-jurisdictional Pension Plans which came into force July 1, 2020. The Agreement provides a clear legal framework for the administration and regulation of multi-jurisdictional pension plans in Canada. Alberta, British Columbia, New Brunswick, Nova Scotia, Ontario, Quebec, Saskatchewan and the federal government have all signed onto the Agreement.

International

Our work with international organizations plays a key role in developing regulatory frameworks for banks and insurers and contributes to a strong, stable and resilient global financial system. We have earned a strong international reputation through our active participation in these organizations, allowing us to share the Canadian perspective and help shape new international regulatory and supervisory rules and accounting and actuarial standards that are fit for purpose for the Canadian financial system.

Working with partner organizations in other jurisdictions has also allowed us to expand our knowledge of international best practices in the regulatory domain and leverage established international relationships that proved useful during the pandemic.

Financial Stability Board

Canadian representation on the Financial Stability Board (FSB) includes the Department of Finance, the Bank of Canada and OSFI. During 2020-21 our role included membership on the FSB Plenary, Steering Committee, and Standing Committee on Supervisory and Regulatory Cooperation as well as:

-

helping coordinate the global response to the COVID-19 pandemic;

- publishing a toolkit of effective practices for cyber incident response and recovery;

- working with other jurisdictions in advancing reform around major interest rate benchmarks and the transition away from London Inter-Bank Offered Rate (LIBOR);

- publishing an issues note on the regulatory issues associated with the emergence of global stablecoins;

- publishing a report assessing the financial stability implications of Big Tech firms' entry into finance as well as third-party dependencies associated with cloud services;

- initiating work to examine the financial stability implications of climate change;

- building on a stock-take of financial authorities' experience with climate risk inclusion in their financial stability monitoring;

- publishing a final report on the evaluation of the effects of reforms to end the concept of too-big-to-fail as well as work to address the risk of market fragmentation;

- working with standard-setting bodies to finalize and operationalize the implementation of G20 post-crisis financial sector reforms in insurance and resolution regimes; and

- co-hosting and chairing the FSB's Roundtable on External Audit in a virtual format this past year.

In September 2020 OSFI Superintendent Jeremy Rudin chaired the Financial Stability Board's Roundtable on External Audit.