Financial Highlights for the period ended June 30, 2022

Introduction

Raison d’être

The Office of the Superintendent of Financial Institutions (OSFI) was established in 1987 by an Act of Parliament: the Office of the Superintendent of Financial Institutions Act (OSFI Act). It is an independent agency of the Government of Canada and reports to Parliament through the Minister of Finance.

OSFI supervises and regulates all banks in Canada and federal credit unions in Canada and all federally incorporated or registered trust and loan companies, insurance companies, fraternal benefit societies and private pension plans. Under the OSFI Act, the Superintendent is solely responsible for exercising OSFI's authorities and is required to report to the Minister of Finance from time to time on the administration of the financial institutions legislation.

The Office of the Chief Actuary, which is an independent unit within OSFI, provides actuarial valuation and advisory services for the Canada Pension Plan, the Old Age Security program, the Canada Student Loans and Employment Insurance Programs and other public sector pension and benefit plans.

Responsibilities

OSFI regulates and supervises federally regulated financial institutions including banks, insurance companies and pension plans. By doing so, it builds public confidence in the Canadian financial system and contributes to a marketplace where banks can continue to make loans and take deposits, insurance companies can pay policyholders, and pension plans can continue to make payments to retirees.

OSFI’s legislated mandate was implemented in 1996 and consists of the following:

Fostering sound risk management and governance practices

OSFI advances a regulatory framework designed to control and manage risk.

Supervision and early intervention

OSFI supervises federally regulated financial institutions and pension plans to determine whether they are in sound financial condition and meeting regulatory and supervisory requirements.

OSFI promptly advises financial institutions and pension plans if there are material deficiencies, and takes corrective measures or requires that they be taken to expeditiously address the situation.

Environmental scanning linked to safety and soundness of financial institutions

OSFI monitors and evaluates system-wide or sectoral developments that may have a negative impact on the financial condition of federally regulated financial institutions.

Taking a balanced approach

OSFI acts to protect the rights and interests of depositors, policyholders, financial institution creditors and pension plan beneficiaries while having due regard for the need to allow financial institutions to compete effectively and take reasonable risks.

OSFI recognizes that management, boards of directors and pension plan administrators are ultimately responsible for risk decisions and that financial institutions can fail and pension plans can experience financial difficulties resulting in the loss of benefits.

OSFI also provides supervision services to the Canada Mortgage and Housing Corporation in accordance with the National Housing Act.

The OCA is an independent unit within OSFI that provides a range of actuarial valuation and advisory services to the Government of Canada.

Basis of Presentation

These quarterly financial statements have been prepared by management as required by Section 65.1 of the Financial Administration Act and in accordance with Public Sector Accounting Standards (PSAS), using the accrual basis of accounting.

These quarterly financial statements have not been subject to an external audit or review.

OSFI’s Funding Model

OSFI recovers its costs from several revenue sources. It is mainly funded through assessments on the financial institutions and private pension plans that it regulates and supervises, as well as through a user-pay program for legislative approvals and other selected services. OSFI also receives revenues for cost-recovered services. These include revenues from provinces on behalf of which OSFI supervises institutions on contract, and revenues from other federal organizations to which OSFI provides administrative support.

The accompanying quarterly financial statements reflect OSFI’s legislated authority to spend revenues from assessments and other sources as per Section 17(2) of the OSFI Act as well as any authorities granted by Parliament and used by OSFI. OSFI receives an annual parliamentary appropriation pursuant to Section 16 of the OSFI Act to support the operations of the Office of the Chief Actuary. Such funding is presented as Government Funding in the Statement of Operations and the amount is consistent with the Main and Supplementary Estimates per the Appropriation Act in effect for the reporting period.

Financial Review and Highlights - Fiscal Year to Date

Statement of Financial Position and Statement of Cash Flows

The majority of OSFI’s revenue is derived from base assessments on federally regulated financial institutions. Assessments are billed annually, usually in the second quarter of the fiscal year. As a result of this annual cycle, some accounts in OSFI’s Statement of Financial Position can vary significantly throughout the year. In between base assessment billings, OSFI’s cash entitlement balance decreases gradually as payments pertaining to operational costs and asset acquisitions are issued. Similarly, OSFI’s accrued base assessments balance increases, to reflect expenses incurred but not yet billed. After the base assessments are billed and collected, cash and accounts receivable increase, as do unearned base assessments. OSFI last invoiced its base assessments in August 2021.

During the three months ended June 30, 2022, OSFI’s cash entitlement balance decreased by $47.1 million, its trade and other receivables increased by $1.5 million, and its accrued base assessments increased by $50.2 million.

As explained in Note 2 (a) to the financial statements, OSFI has a revolving expenditure authority from the Treasury Board Secretariat to draw upon the Consolidated Revenue Fund to ensure the availability of funds prior to receipt of revenue. Additional information on OSFI’s sources and uses of cash can be found in its Statement of Cash Flows.

Statement of Operations

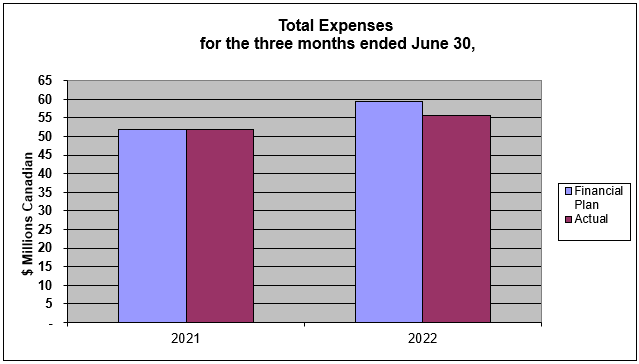

OSFI operates on a cost recovery model. Assessment revenue is recorded at an amount necessary to balance revenue and expenses after all other sources of revenue are taken into account. OSFI’s total expenses for the three months ended June 30, 2022 were $55.6 million, a $3.8 million or 7.4% increase from the same period last year.

- Personnel costs rose by $3.5 million or 8.5% due to the staffing of vacant / new positions in accordance with OSFI’s most recent Operational Plan and normal escalation / merit increases.

- Professional services costs increased by $0.7 million or 17.0% as a result of planned initiatives related to OSFI’s 2022-2025 Strategic Plan.

- Machinery and equipment costs decreased by $0.5 million or 62.9% due to lower equipment purchases this year. Last year’s expenses included the costs related to the purchase of smart phones that was not incurred this year.

OSFI’s total year-to-date expenses of $55.6 million were $3.7 million or 6.2% below plan (versus $0.1 million or 0.2% below plan for the same period last year). OSFI monitors its performance via monthly reporting and quarterly forecast exercises. The variance versus this year’s plan is primarily due to slightly slower than planned growth in accordance with OSFI’s 2022-2025 Strategic Plan. Additional details around the Blueprint for transformation can be found in the Significant changes to Operations, Personnel and Programs section at the end of this document.

Text version - Chart 1

| blank | 2021 | 2022 |

|---|---|---|

| Financial Plan

($millions Canadian) |

$51.9 | $59.3 |

| Actual

($millions Canadian) |

$51.8 | $55.6 |

Government Funding

In addition to its assessment and cost-recovered services revenues, OSFI was granted a parliamentary appropriation of $1.2 million for the fiscal year ending March 31, 2023 (2022 - $ 1.2 million). During the three months ended June 30, 2022, OSFI recognized $0.3 million (2021 - $0.3 million) of this annual amount.

Risks and Uncertainties

OSFI operates in a constantly changing environment reflected in uncertain economic and financial conditions and an industry that can undergo periods of rapid change and that is becoming increasingly complex. The intensity and pace at which the risk environment is changing requires a reimagining of OSFI’s approach to its risk appetite. OSFI needs a more rigorous and future focussed risk appetite framework that grapples with both identified and other yet-to-be foreseen risks. The risks that exist in such circumstances can have financial consequences, thereby affecting financial statements.

Enterprise Risks

Through its Enterprise Risk Management (ERM) framework and processes, OSFI identifies its key external and internal risksFootnote 1. While OSFI continues to actively address the suite of risks covered by its framework, it also monitors for new ones during each reporting period. As part of the Blueprint for OSFI’s Transformation 2022-25, OSFI is investing additional resources to fortify its risk management capabilities.

External Risks

Macroeconomic and geopolitical uncertainty / COVID-19 Pandemic. This risk relates to the possibility that OSFI may not promptly identify the causes and/or consequences of financial contagion stemming from macroeconomic, geopolitical, or pandemic events and may not proactively respond to them. To address this risk, OSFI actively monitors changes in portfolios and investigates the reasons for such changes in order to assess the implications for financial institutions.

Financial institution (FI) cyber-security vulnerability. There is a risk that OSFI may not respond effectively to cyber threats to Canadian FIs or a major FI cyber-security incident. OSFI continues to actively monitor this risk and the mitigation measures being applied by FIs given the rapid evolution of cyber-attacks, their increasing number, and system interdependencies that could create multiple points of vulnerability for institutions. Issues regarding cyber breaches or service disruption threats are discussed with FIs, including with their Board and Risk Committee.

Innovation in the financial industry. Given the scale and pace of digital innovation within in the financial industry, there is a risk that OSFI may not keep pace with advancements/developments (e.g., FinTech, Insurtech, Cryptoassets, shadow banking, insurance companies alternative investments, use of non-regulated retrocession reinsurers). OSFI has been further investing in its regulatory / supervisory capabilities and resources in these risk areas.

Climate change. Weather and climate threats are among the top risks that will have the biggest global impact over the next ten years according to the 2018 Global Risks Report from the World Economic Forum. There is a risk that OSFI may not keep pace with the impacts this could have on financial industry. OSFI has created a new Climate Risk division to address this risk. OSFI is also working with partners such as the Bank of Canada and international partners to develop new models and leverage existing models to monitor the impact of such climate changes and addresses issues, as appropriate.

Internal Risks

OSFI manages a suite of internal risks that can also affect resources, given the investments needed to mitigate them appropriately. Areas of focus pertain to:

Internal change agenda and organizational change management maturity. OSFI has undergone several significant business changes and adaptations in the areas of technology renewal, organizational re-structuring, and supervisory process reviews. OSFI will continue to undergo significant organizational change as a result of the Blueprint for OSFI’s Transformation 2022-25 (Blueprint) released on December 20, 2021. There is a risk that development and delivery of OSFI’s internal change agenda may be detrimental to the effective delivery of its core mandate or its workforce due to change fatigue and diminishing morale. To mitigate this risk, OSFI has developed a new 3-year strategic plan that forms the basis for a single, enterprise-wide Operational Plan that replaces the structure of individual Sector Plans to guide this transformation. Additionally, extensive efforts are being deployed in the area of change management, including the creation of a Transformation Office to manage OSFI’s transformation and a dedicated Enterprise Change Management function.

Human resources capacity and capability. OSFI’s success is dependent upon having employees with highly specialized knowledge, skills, and experience to regulate and supervise FIs. There is a risk that OSFI’s human capital may be inadequate to deliver on its mandate due to skill gaps, experience gaps, a lack of technical knowledge to keep pace with FIs’ evolving business models (FinTech), turnover, succession planning/ key person risk, or poor performers. In response to this risk, OSFI continues the implementation of its comprehensive Human Capital Strategy. Risks related to employee wellness and resilience have increased because of the COVID-19 Pandemic and a primarily virtual work environment. OSFI is also consulting with employees as it plans its eventual return to the Office in a hybrid model.

Financial institution information and data. There is a risk that OSFI may over-rely on information provided by FIs’ management to assess the quality of portfolios or that the FI data collected and OSFI’s management of it are inadequate to effectively deliver on OSFI’s mandate. OSFI has developed an Enterprise Data Management Strategy, which it continues to execute on to respond to this risk.

Protection of Information. OSFI’s information holdings include sensitive and personal information. As such, there is a risk that OSFI’s systems may be inappropriately accessed by external parties or inappropriately used by its employees. To address this risk OSFI is implementing a Cyber Security Strategy and Action Plan while also optimizing the use of existing security technologies.

Financial Risks

Financial risks, primarily liquidity risk and credit risk, are closely managed and continue to be rated low. Please refer to Note 11 to the financial statements for a full analysis of the financial risks to which OSFI is exposed.

Significant Changes in Relation to Operations, Personnel and Programs

On December 20, 2021 OSFI released A Blueprint for OSFI’s Transformation 2022-25, which articulated the direction for a transformation of the organization that takes into account a rapidly changing risk environment and aims to ensure that OSFI continues to contribute to confidence in Canada’s financial system. At the heart of the transformation are three foundational elements:

- Refocus the delivery of OSFI’s mandate.

- Expand and fortify risk management capabilities and risk appetite.

- Enhance the organization’s culture to thrive in increasing uncertainty.

In the fourth quarter of 2021-22 OSFI completed its Strategic / Operational Planning exercises building upon on the vision of the Blueprint and establishing the organization’s goals and priorities for the next three years.

The 2022-2025 Strategic Plan was released on April 22, 2022. It presents six priority initiatives:

- Culture

- Risk Strategy and Governance

- Strategic Stakeholder and Partner Engagement

- Policy Innovation

- Supervisory Framework

- and Data Management and Analytics

These changes resulted in the reorganization of OSFI’s operations into four sectors:

- Supervision

- Policy, Innovation and Stakeholder Affairs

- Strategic Risk and Governance

- Corporate Services and Transformation

Implementing the underlying initiatives will grow OSFI’s financial and human resource footprint over the three years of the plan from an annual spend of $212.5 million for the year ended March 31, 2022, to approximately $290 million by March 31, 2025. This represents a growth of 31.8% over three years from OSFI’s pre transformation budget for the year ending March 31, 2023 of $220 million. The pace of growth will be dependent in part upon how quickly OSFI can add the staff needed to implement these six priority initiatives.

On June 9th, 2022, OSFI announced the appointment of Mr. Tolga Yalkin as Assistant Superintendent of the Policy, Innovation and Stakeholder Affairs Sector. This appointment completes a series of moves within OSFI’s Executive Committee to align with the new structure. In addition to Mr. Yalkin, OSFI’s Executive committee includes Peter Routledge, Superintendent; Ben Gully, Deputy Superintendent, Supervision; Jamey Hubbs, Vice Superintendent; Michelle Doucet, Assistant Superintendent and Chief Operating Officer; Angie Radiskovic, Assistant Superintendent and Chief Strategy and Risk Officer; and Assia Billig, Chief Actuary.

On May 26th, 2022, Mr. Jamey Hubbs, Vice Superintendent announced his retirement effective October 2022. As part of his Vice Superintendent role Mr. Hubbs was responsible for managing two new sectors: 1) Policy Innovation and Stakeholder Affairs, and 2) Strategy, Risk, and Governance, established as part of the reorganization arising from the implementation of the new Strategic Plan. Given the transitory nature of this role and the fulfillment of its purpose, the position is no longer required.

There have been no other significant changes in relation to Operations, Personnel and Programs during the quarter ended June 30, 2022.

Approval by Senior Officials

Approved by,

Marc Desautels,

Chief Financial Officer

Peter Routledge,

Superintendent

Footnotes

- Footnote 1

-

External risks are those driven by external factors that can directly impact the organization’s ability to deliver on its expected results. Internal risks, while sometimes resulting from external pressures, are mainly driven by internal decisions and investments.