Pension Plans for the Canadian Forces – Regular Force and Reserve Force as at 31 March 2019

Accessibility statement

The Web Content Accessibility Guidelines (WCAG) defines requirements for designers and developers to improve accessibility for people with disabilities. It defines three levels of conformance: Level A, Level AA, and Level AAA. This report is partially conformant with WCAG 2.0 level AA. If you require a compliant version, please contact webmaster@osfi-bsif.gc.ca.

The Honourable Jean-Yves Duclos, P.C., M.P.

President of Treasury Board

Ottawa, Canada

K1A 0R5

Dear Minister:

Pursuant to section 6 of the Public Pensions Reporting Act, I am pleased to submit the report on the actuarial review as at 31 March 2019 of the Canadian Forces Pension Plans. This actuarial review is in respect of pension benefits and contributions of both the Regular Force Pension Plan and the Reserve Force Pension Plan. The Regular Force Pension Plan is established by Parts I, III and IV of the Canadian Forces Superannuation Act, includes the Canadian Forces-related benefits provided under the Special Retirement Arrangements Act, and is subject to the Pension Benefits Division Act. The Reserve Force Pension Plan is established by Part I.1 of the Canadian Forces Superannuation Act and subject to the Pension Benefits Division Act.

Yours sincerely,

Assia Billig, FCIA, FSA, PhD

Chief Actuary

Table of contents

Tables

- Table 1 Ultimate Best-Estimate Economic Assumptions

- Table 2 Main Results as at 31 March 2019

- Table 3 Canadian Forces Pension Fund Current Service Cost on a Calendar Year Basis

- Table 4 Reserve Force Pension Fund Current Service Cost on a Calendar Year Basis

- Table 5 RCA Current Service Cost on a Calendar Year Basis

- Table 6 State of the Canadian Forces Superannuation Account

- Table 7 Financial Position - Canadian Forces Pension Fund

- Table 8 Financial Position - Reserve Force Pension Fund

- Table 9 Reconciliation of the Financial Position - Account and Funds

- Table 10 Experience Gains and Losses

- Table 11 Revision of Actuarial Assumptions

- Table 12 Current Service Costs for Plan Year 2020

- Table 13 Reconciliation of Current Service Costs

- Table 14 Member Contribution Rates

- Table 15 Projection of Current Service Cost on a Plan Year Basis - CFPF

- Table 16 Projection of Current Service Cost on a Plan Year Basis - RFPF

- Table 17 Administrative Expenses

- Table 18 Estimated Contributions for Prior Service

- Table 19 Sensitivity of Results to Variation in Longevity Improvement Factors

- Table 20 Sensitivity of Results to Variations in Key Economic Assumptions- Regular Force

- Table 21 Sensitivity of Results to Variations in Key Economic Assumptions - Reserve Force

- Table 22 State of the RCA Account

- Table 23 RCA - Current Service Cost

- Table 24 Estimated Government Credit

- Table 25 Estimated Government Cost

- Table 26 Regular Force Member Contribution Rates

- Table 27 Reconciliation of Balances in Superannuation Account

- Table 28 Reconciliation of Balances in Canadian Forces Pension Fund

- Table 29 Reconciliation of Balances in RCA Account

- Table 30 Reconciliation of Balances in Reserve Force Pension Fund

- Table 31 Interest earnings / Rates of return

- Table 32 Summary of Membership Data

- Table 33 Reconciliation of Regular Force Contributors

- Table 34 Reconciliation of Reserve Force Contributors

- Table 35 Reconciliation of Regular Force Pensioners

- Table 36 Reconciliation of Reserve Force Pensioners

- Table 37 Reconciliation of Spouse Survivors

- Table 38 Reconciliation of Survivors - Children/Students

- Table 39 Actuarial Value of Canadian Forces Pension Fund Assets

- Table 40 Actuarial Value of Reserve Force Pension Fund Assets

- Table 41 Asset Mix

- Table 42 Real Rate of Return by Asset Type

- Table 43 Overall Rate of Return on Assets of the CFPF and RFPF

- Table 44 Rates of Return on Assets in Respect of the CFPF and the RFPF

- Table 45 Transfer Value

- Table 46 Economic Assumptions

- Table 47 Report on Canadian Economic Statistics 1924-2018

- Table 48 Sample of Assumed Seniority and Promotional Salary Increases

- Table 49 Sample of Assumed Rates of Disability Retirement - Reserve Force Plan

- Table 50 Sample of Assumed 3B Disability Incidence Rates (Own Occupation) - Regular Force Plan

- Table 51 Sample of Assumed Rates of Retirement - Regular Force Plan - Old Terms of Service

- Table 52 Sample of Assumed Rates of Retirement - Regular Force Plan - New Terms of Service

- Table 53 Sample of Assumed Rates of Retirement - Reserve Force members

- Table 54 Sample of Assumed Withdrawal Rates - Regular Force Plan - Old Terms of Service

- Table 55 Sample of Assumed Withdrawal Rates - Regular Force Plan - New Terms of Service

- Table 56 Sample of Assumed Withdrawal Rates for Reserve Force Members - Male Officer

- Table 57 Sample of Assumed Withdrawal Rates for Reserve Force Members - Male Other Rank

- Table 58 Sample of Assumed Withdrawal Rates for Reserve Force Members - Female Officer

- Table 59 Sample of Assumed Withdrawal Rates for Reserve Force Members - Female Other Rank

- Table 60 Sample of Assumed Proportions of Members Electing a Deferred Annuity

- Table 61 Sample of Assumed Rates of Mortality

- Table 62 Sample of Assumed Longevity Improvement Factors

- Table 63 Life Expectancy of Contributors and Healthy Pensioners

- Table 64 Sensitivity of Life Expectancy to Variation in Longevity Improvement Factors

- Table 65 Assumptions for Survivor Spouse Allowances

- Table 66 Assumptions for Survivor Children Allowances

- Table 67 Wage Measure - RFPF

- Table 68 Impact of Various Investment Policies - CFPF

- Table 69 Median and 10% Downside Returns, Funding Ratio and Contributions for Various Portfolios - CFPF

- Table 70 Tail Event Portfolio Returns - CFPF

- Table 71 Sensitivity of the Projected CFPF Surplus/(Deficit) as at 31 March 2022

- Table 72 Impact on the Superannuation Account / CFPF of Prolonged Low Bond Yields

- Table 73 Regular Force - Male Officers

- Table 74 Regular Force - Male Officers - Summary

- Table 75 Regular Force - Male Other Ranks

- Table 76 Regular Force - Male Other Ranks - Summary

- Table 77 Regular Force - Female Officers

- Table 78 Regular Force - Female Officers - Summary

- Table 79 Regular Force - Female Other Ranks

- Table 80 Regular Force - Female Other Ranks - Summary

- Table 81 Reserve Force - Male Officers

- Table 82 Reserve Force - Male Officers - Summary

- Table 83 Reserve Force - Male Other Ranks

- Table 84 Reserve Force - Male Other Ranks - Summary

- Table 85 Reserve Force - Female Officers

- Table 86 Reserve Force - Female Officers - Summary

- Table 87 Reserve Force - Female Other Ranks

- Table 88 Reserve Force - Female Other Ranks - Summary

- Table 89 Regular Force - Male Officers - Retirement Pensioners

- Table 90 Regular Force - Female Officers - Retirement Pensioners

- Table 91 Regular Force - Male Other Ranks - Retirement Pensioners

- Table 92 Regular Force - Female Other Ranks - Retirement Pensioners

- Table 93 Regular Force - Male Officers - 3B Pensioners

- Table 94 Regular Force - Female Officers - 3B Pensioners

- Table 95 Regular Force - Male Other Ranks - 3B Pensioners

- Table 96 Regular Force - Female Other Ranks - 3B Pensioners

- Table 97 Regular Force - Male Officers - 3A Pensioners

- Table 98 Regular Force - Female Officers - 3A Pensioners

- Table 99 Regular Force - Male Other Ranks - 3A Pensioners

- Table 100 Regular Force - Female Other Ranks - 3A Pensioners

- Table 101 Reserve Force - Male Officers - Retirement Pensioners

- Table 102 Reserve Force - Female Officers - Retirement Pensioners

- Table 103 Reserve Force - Male Other Ranks - Retirement Pensioners

- Table 104 Reserve Force - Female Other Ranks - Retirement Pensioners

- Table 105 Reserve Force - Officers - Disability Pensioners

- Table 106 Reserve Force - Other Ranks - Disability Pensioners

- Table 107 Regular Force - Surviving Spouses

- Table 108 Reserve Force - Surviving Spouses

Charts

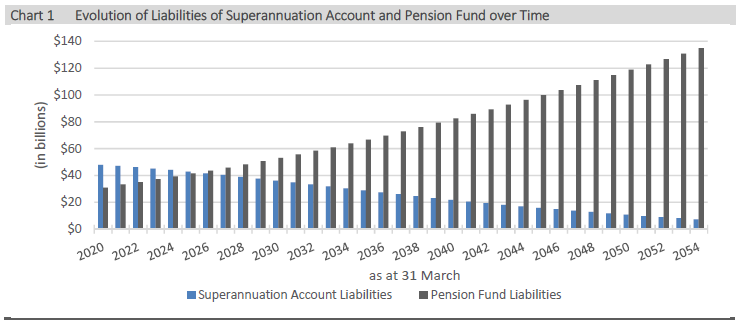

- Chart 1 Evolution of Liabilities of Superannuation Account and Pension Fund over Time

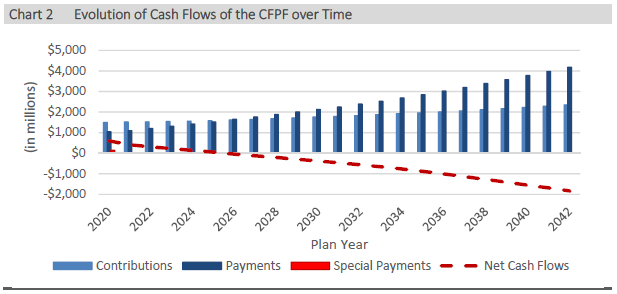

- Chart 2 Evolution of Cash Flows of Superannuation Account and CFPF over Time

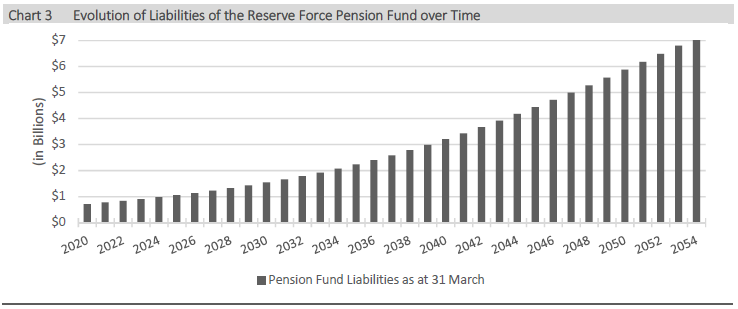

- Chart 3 Evolution of Liabilities of the Reserve Force Pension Fund over Time

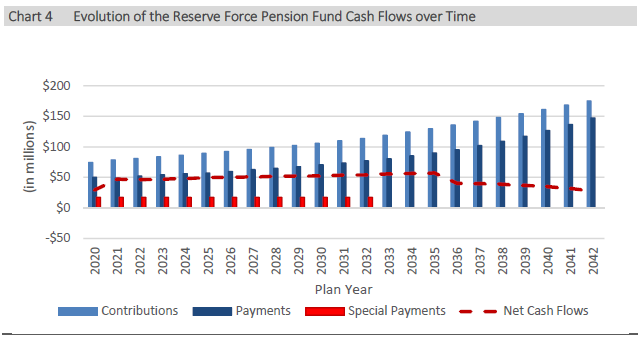

- Chart 4 Evolution of the Reserve Force Pension Fund Cash Flows over Time

- Chart 5 Range of Potential Funding Ratio for the Best-Estimate Portfolio - CFPF

1. Executive Summary

This actuarial report on the pension plans for the Canadian Forces – Regular Force Pension Plan (Regular Force Plan) and the Reserve Force Pension Plan (Reserve Force Plan) was made pursuant to the Public Pensions Reporting Act (PPRA).

This actuarial valuation is as at 31 March 2019 and is in respect of the pension benefits and contributions defined by Parts I, III and IV of the Canadian Forces Superannuation Act (CFSA), the Special Retirement Arrangements Act (SRAA), which covers the Retirement Compensation Arrangements (RCA), and the Pension Benefits Division Act (PBDA) for members of the Regular Force Plan. This valuation is also in respect of the pension benefits and contributions defined by Part I.1 of the CFSA and the PBDA for members of the Reserve Force Plan.

The previous actuarial report was prepared as at 31 March 2016. The date of the next periodic review is scheduled to occur no later than 31 March 2022.

1.1 Purpose of the Report

The purposes of this actuarial valuation are to determine the state of the Regular Force Plan composed of the Canadian Forces Superannuation Account (Superannuation Account), the Canadian Forces Pension Fund (CFPF) and the Retirement Compensation Arrangements (RCA) Account, to determine the state of the Reserve Force Plan composed of the Reserve Force Pension Fund (RFPF), to determine the projected current service costs for the CFPF, the RFPF and the RCA Account as well as to assist the President of the Treasury Board in making informed decisions regarding the financing of the government’s pension benefit obligation. This report may not be suitable for another purpose.

1.2 Valuation Basis

This report is based on pension benefit provisions enacted by legislation, summarized in Appendices A and B.

Contribution rates for Regular Force members for calendar years 2019 to 2021 (as approved by the Treasury Board) and for calendar year 2022 and beyond (estimated) have been updated since the last valuation and are assumed to be equal to the contribution rates of Group 1 contributors under the pension plan for the Public Service of Canada (PS pension plan).

Contribution rates for Reserve Force members are set by regulation.

The Canadian Forces Superannuation Act was amended by Bill C-97 which received Royal Assent on 21 June 2019. The amendment modified the rule regarding the non-permitted surplus, increasing the permitted surplus from 10% to 25% of liabilities. The regulations which outline the corresponding provisions for the Reserve Force Plan remain unchanged. There have been no other changes to the plan provisions of either plan since the previous valuation.

The Funding Policy for the Public Sector Pension Plans (Funding Policy) was approved by the Treasury Board in 2018. The policy provides guidance and rules to support prudent governance of the plansFootnote 1 and ensures that sufficient assets are accumulated to meet the cost of the accrued pension benefits. The methods, assumptions and results of this actuarial valuation are consistent with the provisions of the Funding Policy.

For the Regular Force Plan, the financial data on which this valuation is based are composed of:

- The CFPF invested assets that the government has earmarked for the payment of benefits for service since 1 April 2000;

- the Superannuation Account established to track the government’s pension benefit obligations for service prior to 1 April 2000; and

- the RCA Account for benefits in excess of those that can be provided under the Income Tax Act limits for registered pension plans.

For the Reserve Force Plan, the financial data on which this valuation is based are composed of RFPF invested assets that the government has earmarked for the payment of benefits for Reserve Force service.

These pension assets and accounts balances are summarized in Appendix C.

The membership data are provided by the Department of Public Services and Procurement Canada (PSPC). Membership data and tests performed on them are summarized in Appendix D.

The valuation was prepared using accepted actuarial practices in Canada and is based on methods and assumptions summarized in Appendices E to H.

All actuarial assumptions used in this report are best-estimate assumptions and do not include any margin for adverse deviations. They are independently reasonable and appropriate in aggregate for the purposes of the valuation at the date of this report.

Actuarial assumptions used in the previous report were revised based on economic trends and demographic experience. A complete description of the assumptions is given in Appendices F to H. A summary of the ultimate economic assumptions used in this report and those used in the previous report is shown in the following table.

| 31 March 2019 | 31 March 2016 | |

|---|---|---|

| Assumed level of inflation | 2.00% | 2.00% |

| Real increase in pensionable earnings | 0.70% | 0.80% |

| Real increase in YMPE and MPE Table 1 footnote * | 1.00% | 1.10% |

| Real rate of return on the Pension Fund | 4.00% | 4.00% |

| Real rate of return on the Superannuation Account and RCA Account | 2.50% | 2.70% |

|

||

We have reflected the impacts of the COVID-19 pandemic on the economic assumptions used in this report. It is important to note that the pandemic is a very fluid situation that will likely continue to evolve for some time. We have estimated the impacts based on the information known at the time the report was prepared. The final impacts of this health and economic crisis will likely generate some differences in the future.

1.3 Main Findings

| Superannuation Account | Canadian Forces Pension Fund | Reserve Force Pension Fund | RCA Account | |

|---|---|---|---|---|

| Financial Position | ||||

| Recorded Balance/Actuarial Value of Assets | 45,630 | 31,586 | 538 | 882 |

| Actuarial Liability | 48,057 | 31,007 | 711 | 727 |

| Actuarial Excess(Shortfall)/Surplus(Deficit) | (2,427) | 579 | (173) | 155 |

| Current Service Costs for Calendar Year 2021 | ||||

| Member Contributions | - | 539.8 | 21.4 | 4.8 |

| Government Current Service Cost | - | 939.3 | 54.4 | 32.5 |

| Total Current Service Cost/Credit | - | 1,479.1 | 75.8 | 37.2 |

| Special Credits/Payments in Plan Year 2021 | 2,605 | - | 17.4 | - |

|

||||

1.3.1 Superannuation Account (Service prior to 1 April 2000)

As at 31 March 2019, the recorded balance of the Superannuation Account is $45,630 million and the actuarial liability for service prior to 1 April 2000Footnote 2 is $48,057 million. The resulting shortfall is $2,427 million.

In accordance with the CFSA, the actuarial shortfall could be amortized over a maximum period of 15 years beginning on 31 March 2021. If the shortfall is amortized over the maximum period, 15 equal annual credits of $251 million could be made to the Superannuation Account. The time, manner and amount of such credits are to be determined by the President of the Treasury Board.

It is expected that the government will eliminate the actuarial shortfall of the Superannuation Account by making a one-time credit of $2,605 million as at 31 March 2021 that takes into account the interest on the shortfall accumulated from 31 March 2019.

1.3.2 Canadian Forces Pension Fund (Service since 1 April 2000)

1.3.2.1 Current Service Cost

The estimated total current service cost, borne jointly by the contributors of the CFPF and the government, is $1,479.1 million for calendar year 2021. The estimated member contributions are $539.8 million and the estimated government contributions are $939.3 million for calendar year 2021. Administrative expenses are estimated at $16.1 million (included in the total current service cost) for calendar year 2021.

The following table shows the projected current service cost expressed as a percentage of the expected pensionable payrollFootnote 3 and in millions of dollars for the three calendar years following the expected laying of this report. The ratio of government current service cost to the members current service cost is also shown. Projected current service costs shown in this table are based on the member contribution rates shown in Section 2.3.2.

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Ratio of Government to Contributors Current Service Cost | ||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2021 | 539.8 | 939.3 | 1,479.1 | 9.98 | 17.36 | 27.34 | 1.74 |

| 2022 | 548.4 | 947.7 | 1,496.1 | 9.92 | 17.15 | 27.07 | 1.73 |

| 2023 | 558.5 | 958.7 | 1,517.2 | 9.86 | 16.93 | 26.79 | 1.72 |

1.3.2.2 Financial position and amortization of actuarial surplus (deficit)

As at 31 March 2019, the actuarial value of the assets in respect of the CFPF is $31,586 million and the actuarial liability is $31,007 million, resulting in an actuarial excess of $579 million. No special payments are required.

1.3.3 Reserve Force Pension Fund

1.3.3.1 Current Service Cost

The estimated total current service cost, borne jointly by the contributors to the RFPF and the government, is $75.8 million for calendar year 2021. The estimated member contributions are $21.4 million and the estimated government contributions are $54.4 million for calendar year 2021. Administrative expenses are estimated at $7.2 million (included in the total current service cost) for calendar year 2021.

Table 4 shows the projected current service cost expressed as a percentage of the expected pensionable payrollFootnote 3 and in millions of dollars for the three calendar years following the expected laying of this report. The ratio of government current service cost to the members current service cost is also shown. Projected current service costs shown in this table are based on the member contribution rates shown in Section 2.3.2.

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Government to Contributors Ratio |

||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2021 | 21.4 | 54.4 | 75.8 | 5.20 | 13.24 | 18.44 | 2.55 |

| 2022 | 22.4 | 56.3 | 78.7 | 5.20 | 13.05 | 18.25 | 2.51 |

| 2023 | 23.5 | 58.0 | 81.5 | 5.20 | 12.84 | 18.04 | 2.47 |

1.3.3.2 Financial position and amortization of actuarial surplus (deficit)

As at 31 March 2019, the actuarial value of the assets in respect of the RFPF is $538 million and the actuarial liability is $711 million, resulting in an actuarial deficit of $173 million.

In accordance with section 87 of the Reserve Force Pension Plan Regulations, the actuarial deficit is amortized with equal annual instalments over a period of 15 years. To amortize the actuarial deficit of $173 million, 15 equal annual special payments of $17.4 million are required to be made to the RFPF beginning on 31 March 2021, considering the special payment of $5.3 million that was made on 31 March 2020.

1.3.4 RCA Account

As at 31 March 2019, the balance of the RCA Account is $882 million and the actuarial liability is $727 million, resulting in an excess of $155 million.

The estimated RCA total current service cost, borne jointly by the contributors of the CFPF and the government, is $37.24 million for calendar year 2021 and is estimated to be $37.86 million and $38.30 million, respectively, for the following two calendar years.

Table 5 shows the projected current service cost expressed as a percentage of the expected pensionable payroll and the ratio of government current service cost to contributor current service cost for the three calendar years following the expected tabling of this report.

| Calendar Year | Current Service Cost ($ millions) |

Current Service Cost (% of pensionable payroll) |

Ratio of Government to Contributors Current Service Cost | ||||

|---|---|---|---|---|---|---|---|

| Contributors | Government | Total | Contributors | Government | Total | ||

| 2021 | 4.76 | 32.48 | 37.24 | 0.09 | 0.60 | 0.69 | 6.82 |

| 2022 | 4.98 | 32.88 | 37.86 | 0.09 | 0.60 | 0.69 | 6.60 |

| 2023 | 5.15 | 33.15 | 38.30 | 0.09 | 0.59 | 0.68 | 6.44 |

2. Valuation Results

This report is based on pension benefit provisions enacted by legislation, summarized in Appendices A and B, and the financial and membership data summarized in Appendices C and D. The valuation was prepared using accepted actuarial practices in Canada as well as methods and assumptions summarized in Appendices E to H. Emerging experience that differs from the corresponding assumptions will result in gains or losses to be revealed in subsequent reports.

Projections of the financial positions of the Superannuation Account, the CFPF and the RFPF are shown in Appendix I.

2.1 Financial Position

Beginning on 1 April 2000, member and government contributions of the Regular Force Plan are no longer credited to the Canadian Forces Superannuation Account. Rather, they are credited to the Canadian Forces Pension Fund, and the total amount of contributions net of benefits paid and administrative expenses is transferred to the Public Sector Pension Investment Board (PSPIB) and invested in the financial markets.

Contributions made by the government and members of the Reserve Force Plan are credited to the Reserve Force Pension Fund. The total amount of contributions net of benefits paid and administrative expenses is transferred to the PSPIB and invested in the financial markets

The valuation results of this section show the financial position as at 31 March 2019 for each financing arrangement under the CFSA. The results of the previous valuation are also shown for comparison.

2.1.1 Canadian Forces Superannuation Account

| 31 March 2019 | 31 March 2016 | |

|---|---|---|

| Assets | ||

| Recorded Account balance | 45,607 | 45,695 |

| Present value of prior service contributions | 23 | 23 |

| Total Recorded Account Balance | 45,630 | 45,718 |

| Actuarial Liability | ||

| Active contributors | 4,153 | 6,045 |

| Retirement pensioners | 40,280 | 37,804 |

| Disability pensioners | 122 | 154 |

| Surviving dependents | 3,356 | 3,138 |

| Outstanding payments | 1 | - |

| Administrative expenses | 145 | 232 |

| Pension Modernization cost | - | 12 |

| Total Actuarial Liability | 48,057 | 47,385 |

| Actuarial Excess/(Shortfall) | (2,427) | (1,667) |

In accordance with the CFSA, the actuarial shortfall of $2,427 million could be amortized over a maximum period of 15 years beginning on 31 March 2021. If the shortfall is amortized over the maximum period, 15 equal annual credits of $251 million could be made to the Superannuation Account. The time, manner and amount of such credits are to be determined by the President of the Treasury Board. It is expected that the government will amortize the actuarial shortfall through a one-time special credit to the Superannuation Account of $2,605 million as at 31 March 2021 that takes into account the interest on the shortfall accumulated from 31 March 2019 to 31 March 2021.

2.1.2 Canadian Forces Pension Fund

| 31 March 2019 | 31 March 2016 | |

|---|---|---|

| Actuarial Value of Assets | ||

| Market value of assets | 33,123 | 23,168 |

| Actuarial smoothing adjustment | (1,928) | (1,078) |

| Present value of prior service contributions | 328 | 267 |

| Amount receivable from Part I.1 - Rollover members | 63 | 57 |

| Remaining contributions for pre-2007 Reserve Force service | - | 64 |

| Total Actuarial Value of Assets | 31,586 | 22,478 |

| Actuarial Liability | ||

| Active contributors | 17,720 | 15,239 |

| Contributors' pre-2007 Reserve Force service | - | 56 |

| Retirement pensioners | 13,061 | 8,601 |

| Disability pensioners | 7 | 8 |

| Surviving dependents | 136 | 84 |

| Outstanding payments | 83 | 51 |

| Pension Modernization cost | - | 9 |

| Total Actuarial Liability | 31,007 | 24,048 |

| Actuarial Surplus/(Deficit) | 579 | (1,570) |

As at 31 March 2019, the actuarial value of assets in respect of the Pension Fund is $31,586 million and the actuarial liability is $31,007 million, resulting in an actuarial surplus of $579 million. No special payments are required.

If there exists a non-permitted surplusFootnote 4 in the CFPF, no further government contributions for current service cost are permitted until, in the opinion of the President of the Treasury Board, the non-permitted surplus no longer exists. The results of this valuation do not indicate the existence of a non-permitted surplus as at 31 March 2019.

2.1.3 Reserve Force Pension Fund

| 31 March 2019 | 31 March 2016 | |

|---|---|---|

| Actuarial Value of Assets | ||

| Market value of assets | 613 | 505 |

| Actuarial smoothing adjustment | (50) | (30) |

| Present value of prior service contributions | 38 | 25 |

| Remaining contributions for processed prior service | 0 | 42 |

| Remaining contributions for unprocessed prior service | 0 | 28 |

| Amount payable to Regular Force pension plan | (63) | (57) |

| Total Actuarial Value of Assets | 538 | 513 |

| Actuarial Liability | ||

| Active contributors | 481 | 370 |

| Contributors' unprocessed prior service | 0 | 30 |

| Retirement pensioners | 215 | 156 |

| Disability pensioners | 1 | 3 |

| Surviving dependents | 4 | 2 |

| Outstanding payments | 10 | 1 |

| Pension modernization cost | 0 | 4 |

| Total Actuarial Liability | 711 | 566 |

| Actuarial Surplus/(Deficit) | (173) | (53) |

In accordance with section 87 of the Reserve Force Pension Plan Regulations, the actuarial deficit is amortized with equal annual instalments over a period of 15 years. Taking into account the special payment of $5.3 million that was made on 31 March 2020, the actuarial deficit of $173 million could be amortized in 15 equal annual payments of $17.4 million beginning on 31 March 2021.

2.2 CFSA - Reconciliation of the Changes in Financial Position

Table 9 presents the reconciliation of the changes in financial positions of the Superannuation Account, CFPF and the RFPF. Explanations of the elements largely responsible for the changes follow the table.

| Superannuation Account | Canadian Forces Pension Fund | Reserve Force Pension Fund | |

|---|---|---|---|

| As at 31 March 2016 | (1,667) | (1,570) | (53.0) |

| Recognized investment gains as at 31 March 2016 | n/a | 1,078 | 30.0 |

| Revised initial financial position as at 31 March 2016 | (1,667) | (492) | (23.0) |

| Expected interest on initial financial position | (219) | (74) | (3.4) |

| Change in methodology | - | - | 0.7 |

| Retroactive changes to the population data | 275 | 49 | 19.2 |

| Special credits/payments | 1,886 | 484 | 15.5 |

| Net experience gains and losses | 86 | 3,940 | (38.7) |

| Revision of actuarial assumptions | (2,839) | (1,482) | (48.1) |

| Pay Restructuring as at 1 January 2019 | n/a | n/a | (32.6) |

| Change in the amount receivable from Part I.1 - Rollover members | n/a | 6 | (6.0) |

| Change in the present value of administrative expenses | 50 | n/a | n/a |

| Change in the present value of prior service contributions | 8 | 112 | 18.8 |

| Change in Outstanding payments | (1) | (32) | (9.1) |

| Change - Pension Modernization cost | (6) | (4) | - |

| Recognition of remaining contributions for processed prior service | n/a | n/a | (16.0) |

| Unrecognized investment gains as at 31 March 2019 | n/a | (1,928) | (50.4) |

| As at 31 March 2019 | (2,427) | 579 | (173.1) |

2.2.1 Recognized Investment Gains as at 31 March 2016

An actuarial asset valuation method that minimizes the impact of short-term fluctuations in the market value of assets was used in the previous valuation, causing the actuarial value of the CFPF assets to be $1,078 million less than their market value. The same actuarial asset valuation method was used for the RFPF, causing the actuarial value of the RFPF assets to be $30.0 million less than their market value.

2.2.2 Expected Interest on Revised Initial Financial Position

The amount of interest expected to accrue during the intervaluation period increased the revised shortfall by $219 million for the Superannuation Account, increased the revised deficit by $74 million for the Canadian Forces Pension Fund and increased the revised deficit by $3.4 million for the Reserve Force Pension Fund.

These amounts of interest were based on the Superannuation Account yields, the CFPF returns and the RFPF returns projected in the previous report for the three-year intervaluation period.

2.2.3 Retroactive Changes to the Population Data

The net impact of the retroactive changes to the population data received from PSPC has resulted in a decrease of $275 million in the Superannuation Account actuarial liabilities, a decrease of $49 million in the CFPF actuarial liabilities and a decrease of $19.2 million in the RFPF actuarial liabilities.

The decrease in the Superannuation Account actuarial liabilities is due to a significant change to the information pertaining to retirement pensioners between the information received at the previous valuation and the information received for this valuation.

2.2.4 Special Payments Made in the Intervaluation Period

A deficit of $1,667 million was reported in the Superannuation Account as at 31 March 2016. The government made a one-time credit of $1,813 million as at 31 March 2017 which resulted in an increase of $1,886 million in the recorded balance of the Account as at 31 March 2019.

A deficit of $1,570 million was reported in the CFPF as at 31 March 2016, and the government took the position to amortize this deficit over the 15 years starting on 31 March 2018. A total of $460 million of special payments were made to the CFPF during the intervaluation period that resulted in an increase of $484 million in asset after factoring the expected interest to 31 March 2019.

A deficit of $53.0 million was reported in the RFPF as at 31 March 2016 which was to be amortized over a period of 15 years in accordance with the Reserve Force Pension Plan Regulations. A total of $14.8 million of special payments were made to the RFPF during the intervaluation period that resulted in an increase of $15.5 million in asset after factoring the expected interest to 31 March 2019.

2.2.5 Experience Gains and Losses

Since the previous valuation, experience gains and losses have decreased the Superannuation Account actuarial shortfall by $86 million. The CFPF and the RFPF actuarial deficit have decreased by $3,940 and increased by $38.7 million respectively due to the experience gains and losses over the three-year intervaluation period. The main experience gain and loss items are described in Table 10.

| Superannuation Account | Canadian Forces Pension Fund | Reserve Force Pension Fund | |

|---|---|---|---|

| Demographic experience (i) | |||

| Terminations (return of contributions) | 2 | 18 | (1.5) |

| Terminations (deferred annuity) | (2) | (339) | 6.1 |

| Terminations (transfer value) | 10 | 245 | (173.5) Table 10 footnote * |

| Disabilities 3B (annuity) Table 10 footnote ** | (9) | (231) | - |

| Rollover from Part I.1 | - | 72 | - |

| Rehired pensioner members | 13 | 6 | 1.8 |

| Retirements (annuity) | 164 | 86 | 1.1 |

| Disabilities 3A (annuity)Table 10 footnote ** | - | 1 | (0.9) |

| Non-disabled pensioner deaths | (68) | (3) | 0.4 |

| Deaths (annuity) | (9) | (16) | 0.2 |

| Widow(er) deaths | 17 | - | - |

| Disabled pensioner deaths | 2 | - | 0.1 |

| Total | 120 | (161) | (166.2) |

| Investment earnings (ii) | (44) | 4,183 | 106.9 |

| Economic salary increases (iii) | 14 | 64 | - |

| Cost/contributions difference (iv) | 4 | 3 | 28.8 |

| Change in service accrual (v) | - | (33) | n/a |

| Pension benefit division payments (vi) | (28) | (68) | n/a |

| Promotional and seniority increases (vii) | (32) | (45) | n/a |

| Expected/Actual earnings | n/a | n/a | (2.0) |

| Pension indexation (viii) | 31 | 8 | 0.2 |

| Administrative expenses | (1) | 1 | (7.2) |

| Expected/actual disbursements (ix) | 43 | (13) | 3.2 |

| YMPE increases | 4 | 12 | - |

| Miscellaneous | (25) | (11) | (2.4) |

| Net experience gains (losses) | 86 | 3,940 | (38.7) |

|

|||

-

The demographic assumptions having a large impact are as follows:

-

The actual number of members opting for a deferred annuity was greater than expected which resulted in an increase of $2 million in the actuarial liability of the Superannuation Account and an increase of $339 million in the CFPF. The actual number of members opting for a deferred annuity was less than expected which resulted in a decrease of $6.1 million in the actuarial liability of the RFPF.

-

The number of terminations with a transfer value was less than expected resulting in a decrease of $10 million in the Superannuation Account shortfall and a decrease of $245 million in the initial CFPF deficit. The number of terminations under the RFPF was more than expected resulting in an increase of $173.5 million in the initial RFPF deficit. A significant proportion of these RFPF terminations were for members rolling over to the Regular Force Pension Plan.

-

The significant increase in the actual number of Disability 3B retirements above the projected number resulted in an increase in the actuarial liability of $9 million in the Superannuation Account and of $231 million in the CFPF.

-

In light of the significant increase in the number of Disability 3B retirements, the number of retirements has decreased over the intervaluation period which resulted in a decrease of $164 million in the actuarial liability of the Superannuation Account and a decrease of $86 million in the actuarial liability of the CFPF.

-

The mortality under the Canadian Forces Pension Plans worsened at ages above 75 for male officers and male other ranks and only improved below age 75 for male officers. The net impact resulted in an increase in the actuarial liabilities of $68 and $3 million for the Superannuation Account and the CFPF, respectively. No loss or gain were observed under the RFPF.

-

The surviving spouse mortality worsened during the intervaluation period which resulted in a decrease of $17 million in the actuarial liability of the Superannuation Account. No loss or gain were observed under both the CFPF and RFPF.

-

-

The rates of interest credited to the Superannuation Account were marginally less than the corresponding projected Superannuation Account yields in the previous valuation. Consequently, the experience loss was $44 million. The investment return on both Pension Funds exceeded expectations during the intervaluation period. This resulted in an investment gain of $4,183 million for the CFPF and an investment gain of $106.9 million for the RFPF.

-

Economic salary increases during the intervaluation period were smaller than expected. This resulted in a decrease in the actuarial liability of $14 million in the Superannuation Account and of $64 million in the CFPF.

-

Higher than expected member and government contributions during the intervaluation period resulted in a gain of $4 million with respect to the Superannuation Account, a gain of $3 million with respect to the CFPF and a gain of $28.8 million with respect to the RFPF. The very large discrepancy in the RFPF is due to the processing of buybacks of pre-2007 Reserve Force service.

-

Service accruals higher than expected increased the CFPF actuarial liability by $33 million.

-

The net impact of the divisions of pension due to marriage breakdown (amount paid out to the former spouse versus the actuarial liability released) accounted for a loss of $28 million in the Superannuation Account and an increase of $68 million in the CFPF actuarial deficit. The Reserve Force Plan is not impacted by pension divisions since no direction is provided under the Pension Benefits Division Regulations regarding the division of pension upon the marriage breakdown of member of the Reserve Force Plan.

-

Promotional and seniority salary increases were higher than expected at many ages resulting in an increase in the actuarial liability of $32 million in the Superannuation Account and of $45 million in the CFPF.

-

Pension indexation was as expected at 1 January 2017, less than expected at 1 January 2018 and more than expected at 1 January 2019 which resulted in a decrease in the actuarial liability of $31 million in the Superannuation Account, of $8 million in the CFPF and no impact in the RFPF.

-

Under the Superannuation Account, $43 million less than expected was paid in lump sum and annuity payments as well as $13 million more from the CFPF and $3.2 million less from the RFPF.

2.2.6 Revision of Actuarial Assumptions

Actuarial assumptions were revised based on economic trends and demographic experience as described in Appendices F and G. This revision has increased the Superannuation Account actuarial liability by $2,839 million, increased the CFPF actuarial liability by $1,482 million and increased the RFPF actuarial liability by $48.1 million. The impacts of these revisions are described in the following table and the most important items are discussed thereafter.

| Superannuation Account | Canadian Forces Pension Fund | Reserve Force Pension Fund | |

|---|---|---|---|

| Economic assumptions | |||

| Yields and Rates of return | (3,440) | (1,435) | (56.8) |

| Increases in average pensionable earnings and YMPE/MPE | 38 | 335 | 4.8 |

| Pension Indexation | 323 | 113 | 2.3 |

| Total | (3,079) | (987) | (49.7) |

| Age difference between spouses | 4 | - | - |

| Survivor mortality rates | 125 | 18 | 0.7 |

| Longevity improvement factors | (284) | (91) | (2.7) |

| Pensioner mortality rates | 347 | 29 | 1.2 |

| Disabled retirements 3B rates | (18) | (499) | - |

| Proportion of Disability 3B with Immediate CPP Offset | 5 | 65 | - |

| Proportion married at death | 90 | 29 | 1.0 |

| Pensionable retirements rates | (17) | (128) | (0.1) |

| Annuity reduction factors | (7) | (17) | - |

| Seniority and promotional salary increases | (5) | (105) | 0.3 |

| Proportion electing a deferred annuity | - | (43) | 0.9 |

| Assumptions related to children and students | 1 | 2 | - |

| Withdrawals rates | - | 247 | 0.8 |

| Disabled retirements 3A | - | 1 | (0.7) |

| Net impact of revision | (2,839) | (1,482) | (48.1) |

The net impact of the revision of the assumptions is largely attributable to the changes in economic assumptions and:

- For the Superannuation Account, the plan year 2020 mortality rates for both pensioners and survivors resulted in a gain which was partially offset by the revised longevity improvement factors;

- For the CFPF, the new disabled retirement 3B assumptions;

- For the RFPF, the revised longevity improvement factors.

The following revisions were made to the economic assumptions used in the previous report:

- ultimate real increase in pensionable earnings decreased from 0.80% to 0.70%; and

- ultimate real increase in YMPE and MPE decreased from 1.10% to 1.00%; and

- ultimate real rate of return on the Superannuation Account and RCA Account decreased from 2.70% to 2.50%.

Details of the changes in economic assumptions are described in Appendix F.

Details of the changes in demographic assumptions, in particular in mortality rates, are described in Appendix G.

2.2.7 Change in the Present Value of Administrative Expenses for the Superannuation Account

The previous report annual administrative expense assumption of 0.75% of total pensionable payroll is reduced to 0.55% in this report. This decrease is based on average administrative expenses observed during the intervaluation period. The reduction of 0.2% of annual administrative expenses resulted in a decrease of $50 million of the Superannuation Account actuarial shortfall.

For plan year 2020, 50.2% of total administrative expenses are being charged to the Superannuation Account; it is assumed that the proportion charged to the Superannuation Account will reduce at the same rate of 2.5% per year as assumed in the previous valuation.

2.2.8 Change in the Present Value of Prior Service Contributions

The expected total government cost is shown in Table 24. The government is expected to make additional contributions in excess of the current service cost for members’ prior service elections. The change in the present value of prior service contributions corresponds to members’ elections since the last report where the members opted to pay for these elections by instalments. Members’ prior service elections paid through instalments has the effect of increasing the Superannuation Account and the CFPF assets by $8 and $112 million respectively as well as increasing the RFPF assets by $18.8 million.

2.2.9 Unrecognized Investment Gains

An actuarial asset valuation method that minimizes the impact of short-term fluctuations in the market value of assets was also used for this valuation. The method, which is described in section E.2, resulted in an actuarial value of the CFPF and the RFPF assets that are $1,928 and $50.4 million less than their respective market values as at 31 March 2019.

2.3 CFSA - Cost Certificate

2.3.1 Current Service Cost

The details of the current service cost for plan yearFootnote 5 2020 and reconciliation with the 2017 current service cost are shown below.

| CFPF | RFPF | |

|---|---|---|

| Members required contributions | 528.9 | 19.3 |

| Government current service cost | 926.5 | 50.2 |

| Total current service cost | 1,455.4 | 69.5 |

| Expected pensionable payroll | 5,254.8 | 371.4 |

| Total current service cost as % of expected pensionable payroll | 27.70% | 18.71% |

| CFPF | RFPF | |

|---|---|---|

| For plan year 2017 | 25.86 | 17.48 |

| Valuation methodology change | - | (0.41) |

| Retroactive changes to the population data | 0.06 | 0.08 |

| Expected current service cost change | (0.71) | (0.43) |

| Experience (gains)losses | (0.04) | (0.57) |

| Changes in assumptions | ||

| Economic Assumptions | 1.72 | 2.76 |

| Withdrawals | (0.45) | (0.17) |

| Pensionable retirements | 0.15 | - |

| Annuity reduction factors | 0.03 | - |

| Proportion electing a deferred annuity | 0.07 | (0.07) |

| Disabled retirements 3A | - | 0.02 |

| Disabled retirements 3B | 1.00 | - |

| Mortality Rates | (0.15) | (0.03) |

| Longevity improvement factors | 0.08 | 0.06 |

| Seniority and promotional salary increases | 0.20 | 0.01 |

| Proportion married at death | (0.02) | (0.02) |

| Assumptions related to children and students | - | - |

| Administrative expenses | (0.10) | - |

| For plan year 2020 | 27.70 | 18.71 |

2.3.2 Projection of Current Service Costs

The current service cost is borne jointly by the plan members and the government. The Regular Force member contribution rates are determined on a calendar year basis and they have been changed since the last valuation. Contribution rates are set equal to the contribution rates of Group 1 contributors under the PS pension plan. Contribution rates for the Reserve Force members are set by regulation. The contribution rates are as follows:

| Calendar Year | Regular Force | Reserve Force | |

|---|---|---|---|

| Below YMPE | Above YMPE | ||

| 2019 | 9.56% | 11.78% | 5.20% |

| 2020 | 9.53% | 11.72% | 5.20% |

| 2021 | 9.49% | 11.67% | 5.20% |

| 2022 | 9.44% | 11.62% | 5.20% |

| 2023 | 9.38% | 11.58% | 5.20% |

Current service costs on a plan year basis, expressed in percentage of the projected pensionable payroll as well as in dollar amount are shown in Table 15 for Regular Force members and Table 16 for Reserve Force members. Member contributions and the government current service costs are also shown on a calendar year basis in the Executive Summary.

| Plan Year |

$ Millions | % of Pensionable Payroll | Split Members : Government |

||||

|---|---|---|---|---|---|---|---|

| Members | Government | Total | Members | Government | Total | ||

| 2020 | 528.9 | 926.5 | 1455.4 | 10.07 | 17.63 | 27.70 | 36% : 64% |

| 2021 | 535.5 | 935.8 | 1471.3 | 10.02 | 17.51 | 27.54 | 36% : 64% |

| 2022 | 542.0 | 939.7 | 1481.7 | 9.98 | 17.29 | 27.27 | 37% : 63% |

| 2023 | 551.2 | 949.8 | 1501.0 | 9.92 | 17.09 | 27.00 | 37% : 63% |

| 2024 | 562.5 | 960.1 | 1522.6 | 9.87 | 16.85 | 26.72 | 37% : 63% |

| Plan Year |

$ Millions | % of Pensionable Payroll | Split Members : Government |

||||

|---|---|---|---|---|---|---|---|

| Members | Government | Total | Members | Government | Total | ||

| 2020 | 19.3 | 50.2 | 69.5 | 5.20 | 13.51 | 18.71 | 28% : 72% |

| 2021 | 20.6 | 53.3 | 73.9 | 5.20 | 13.45 | 18.65 | 28% : 72% |

| 2022 | 21.6 | 54.9 | 76.5 | 5.20 | 13.19 | 18.39 | 28% : 72% |

| 2023 | 22.7 | 56.8 | 79.5 | 5.20 | 13.02 | 18.22 | 29% : 71% |

| 2024 | 23.8 | 58.4 | 82.2 | 5.20 | 12.79 | 17.99 | 29% : 71% |

2.3.3 Administrative Expenses

Based upon the assumptions described in Appendix G.2.3, the CFPF and the RFPF administrative expenses are included in the total current service costs. As for the previous report, the expected administration expenses exclude the PSPIB operating expenses as these are recognized implicitly through a decrease in the real rate of return. The estimated administrative expenses are shown in the following table:

| Plan Year | Superannuation Account | CFPF | RFPF |

|---|---|---|---|

| 2020 | 14.5 | 14.4 | 6.5 |

| 2021 | 14.0 | 15.4 | 6.9 |

| 2022 | 13.5 | 16.4 | 7.3 |

| 2023 | 13.1 | 17.5 | 7.6 |

| 2024 | 12.6 | 18.7 | 8.0 |

The Superannuation Account administrative expenses have been capitalized and increase the liability for service accrued prior to 1 April 2000.

2.3.4 Contributions for Prior Service Elections

Based on the valuation data and the assumptions described in Appendices F.2 and F.3 and recent statistical information provided by the PSPC, member and government contributions for prior service elections were estimated as follows:

| Plan Year | Superannuation Account | CFPF | RFPF | |||

|---|---|---|---|---|---|---|

| Members | Government | Members | Government | Members | Government | |

| 2020 | 1.6 | 1.6 | 15.2 | 26.2 | 3.6 | 3.6 |

| 2021 | 1.5 | 1.5 | 15.7 | 27.0 | 3.2 | 3.2 |

| 2022 | 1.4 | 1.4 | 16.2 | 27.6 | 3.1 | 3.1 |

| 2023 | 1.3 | 1.3 | 16.7 | 28.3 | 3.1 | 3.1 |

| 2024 | 1.2 | 1.2 | 17.3 | 28.9 | 3.1 | 3.1 |

|

||||||

2.4 Sensitivity of Valuation Results to Variations in Longevity Improvement Factors

This valuation assumes that the current mortality rates applicable to members of the Canadian Forces Pension Plans will improve over time in line with the longevity improvement assumptionFootnote 6 contained in the 30th Canada Pension Plan (CPP) actuarial report.

Table 19 presents the effect of varying the longevity improvement assumptions on the actuarial liabilities as 31 March 2019 and the plan year 2020 current service cost. The best-estimate longevity improvement assumption is described in Table 62 of Appendix G.

| Current Service Cost (% of Pensionable Payroll) |

Actuarial Liability as at 31 March 2019 ($ millions) |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Canadian Forces Pension Fund | Reserve Force | Superannuation Account | Canadian Forces Pension Fund | Reserve Force | ||||||

| 2020 | Effect | 2020 | Effect | Effect | Effect | 2020 | Effect | |||

| Best-Estimate | 27.70 | None | 18.71 | None | 47,385 | None | 24,048 | None | 711 | None |

| - if 0% | 26.71 | (0.99) | 17.71 | (1.00) | 45,241 | (2,144) | 23,131 | (917) | 681 | (30) |

| - if ultimate 50% higher | 27.92 | 0.23 | 18.96 | 0.25 | 47,600 | 215 | 24,216 | 168 | 717 | 6 |

| - if ultimate 50% lower | 27.46 | (0.23) | 18.45 | (0.26) | 47,170 | (215) | 23,876 | (172) | 705 | (6) |

| - if kept at 2020 level | 28.54 | 0.84 | 19.59 | 0.88 | 48,685 | 1,300 | 24,765 | 717 | 735 | 24 |

The sensitivity of the life expectancy at age 65 to the variation in longevity improvement factors is shown in Table 64.

2.5 Sensitivity to Variations in Key Economic Assumptions

The information required by statute, which is presented in the main report, has been derived using best-estimate assumptions regarding future demographic and economic trends. The key best-estimate assumptions, i.e. those for which changes within a reasonable range have the most significant impact on the long-term financial results, are described in Appendices F and G.

Given the length of the projection period and the number of assumptions required, it is unlikely that the actual experience will develop precisely in accordance with best-estimate assumptions that underlie the actuarial estimates. Individual sensitivity tests have been performed using alternative assumptions.

Table 20 presents the effect on the plan year 2 current service cost and the liabilities as at 31 March 2019 for the Regular Force Plan when key economic assumptions are varied by one percentage point per annum. Similarly, Table 21 presents the effect on the plan year 2020 current service cost and the liabilities for the Reserve Force Plan when key economic assumptions are varied by one percentage point per annum.

| Assumption(s) Varied | Current Service Cost for Plan Year 2020 (% of pensionable payroll) |

Actuarial Liability as at 31 March 2019 ($ millions) |

||||

|---|---|---|---|---|---|---|

| Superannuation Account | Canadian Forces Pension Fund | |||||

| 2020 | Effect | Effect | Effect | |||

| Best-Estimate | 27.70 | None | 48,057 | None | 31,007 | None |

| Investment yield | ||||||

| - if 1% higher | 22.47 | (5.23) | 42,265 | (5,792) | 26,278 | (4,729) |

| - if 1% lower | 34.91 | 7.21 | 55,290 | 7,233 | 37,220 | 6,213 |

| Pension Indexation | ||||||

| - if 1% higher | 32.91 | 5.21 | 54,938 | 6,881 | 35,942 | 4,935 |

| - if 1% lower | 23.76 | (3.94) | 42,431 | (5,626) | 27,117 | (3,890) |

| Salary, YMPE and MPE | ||||||

| - if 1% higher | 29.97 | 2.27 | 48,149 | 92 | 32,145 | 1,138 |

| - if 1% lower | 25.88 | (1.82) | 47,978 | (79) | 30,068 | (939) |

| Inflation Table 20 footnote * | ||||||

| - if 1% higher | 27.15 | (0.55) | 47,907 | (150) | 30,710 | (297) |

| - if 1% lower | 28.31 | 0.61 | 48,227 | 170 | 31,351 | 344 |

|

||||||

| Assumption(s) Varied | Current Service Cost (% of Pensionable Payroll) |

Actuarial Liability as at 31 March 2019 ($ millions) |

||

|---|---|---|---|---|

| 2020 | Effect | Effect | ||

| Best-Estimate | 18.71 | None | 711.1 | None |

| Investment yield | ||||

| - if 1% higher | 15.95 | (2.76) | 599.1 | (112.0) |

| - if 1% lower | 22.61 | 3.90 | 863.1 | 152.0 |

| Pension Indexation | ||||

| - if 1% higher | 23.85 | 5.14 | 856.1 | 145.0 |

| - if 1% lower | 15.15 | (3.56) | 602.1 | (109.0) |

| Salary, YMPE and MPE | ||||

| - if 1% higher | 20.44 | 1.73 | 754.1 | 43.0 |

| - if 1% lower | 17.27 | (1.44) | 674.1 | (37.0) |

| InflationTable 21 footnote * | ||||

| - if 1% higher | 18.62 | (0.09) | 707.1 | (4.0) |

| - if 1% lower | 18.81 | 0.10 | 715.1 | 4.0 |

|

||||

The differences between the results above and those shown in the valuation can also serve as a basis for approximating the effect of other numerical variations in a key assumption to the extent that such effects are linear.

2.6 RCA - Financial Position

This section shows the financial position of the RCA Account as at 31 March 2019. The results of the previous valuation are also shown for comparison.

| 31 March 2019 | 31 March 2016 | |

|---|---|---|

| Recorded Account balance | 443 | 392 |

| Tax Credit (CRA Refundable tax) | 439 | 382 |

| Total Recorded Account Balance | 882 | 774 |

| Actuarial Liability | ||

| Pensionable excess earnings | ||

|

415 | 238 |

|

264 | 163 |

| Survivor Allowance | ||

|

7 | 5 |

|

41 | 35 |

| Total Actuarial Liability | 727 | 441 |

| Actuarial Excess/(Shortfall) | 155 | 333 |

The sum of the recorded balance of the RCA Account and the tax credit (CRA refundable tax) is $882 million; it exceeds the actuarial liability of $727 million by 21% as at 31 March 2019 (76% as at 31 March 2016). The SRAA does not allow for an adjustment to be made to the RCA Account that would allow the recorded balance to track the actuarial liability when there is an actuarial excess.

2.7 RCA - Current Service Cost

The projected current service cost, borne jointly by the members and the government, of 0.44% for plan year 2020 calculated in the previous valuation has increased to 0.68% of pensionable payroll in this valuation. The RCA current service cost for plan year 2020 is estimated to marginally increase to 0.69% of pensionable payroll over the following three years and reduced to 0.67% by plan year 2024 as shown the following table.

| Total current service cost | Plan Year | ||||

|---|---|---|---|---|---|

| 2020 | 2021 | 2022 | 2023 | 2024 | |

| Pensionable excess earnings | 34.9 | 35.7 | 36.4 | 37.0 | 37.3 |

| Survivor Allowance | 0.9 | 1.0 | 1.0 | 1.0 | 1.1 |

| Total | 35.8 | 36.7 | 37.4 | 38.0 | 38.4 |

| Member contributions | 4.4 | 4.6 | 4.8 | 5.0 | 5.2 |

| Government current service cost | 31.4 | 32.1 | 32.6 | 33.0 | 33.2 |

| Current service cost as % of total pensionable payroll | 0.68% | 0.68% | 0.69% | 0.68% | 0.67% |

2.8 Summary of Estimated Government Cost

The following tables summarize the estimated total government credit and cost on a plan year basis.

| Plan Year | RCA Account | Superannuation Account | Total Government Credit | |

|---|---|---|---|---|

| Current Service Cost | Total Prior Service Contributions | Special Credits |

||

| 2020 | 31.4 | 1.6 | 0.0 | 33.0 |

| 2021 | 32.1 | 1.5 | 2,605.0 | 2,638.6 |

| 2022 | 32.6 | 1.4 | 0.0 | 34.0 |

| 2023 | 33.0 | 1.3 | 0.0 | 34.3 |

| 2024 | 33.2 | 1.2 | 0.0 | 34.4 |

| Plan Year | Current Service Cost | Total Prior Service Contributions | Special Payments |

Total Government Cost | ||

|---|---|---|---|---|---|---|

| CFPF | RFPF | CFPF | RFPF | RFPF | ||

| 2020 | 926.6 | 50.2 | 26.2 | 3.6 | 5.3 | 1,011.9 |

| 2021 | 935.8 | 53.3 | 27.0 | 3.2 | 17.4 | 1,036.7 |

| 2022 | 939.6 | 54.9 | 27.6 | 3.1 | 17.4 | 1,042.6 |

| 2023 | 949.7 | 56.8 | 28.3 | 3.1 | 17.4 | 1,055.3 |

| 2024 | 960.1 | 58.4 | 28.9 | 3.1 | 17.4 | 1,067.9 |

3. Actuarial Opinion

In our opinion, considering that this report was prepared pursuant to the Public Pensions Reporting Act,

- the valuation data on which the valuation is based are sufficient and reliable for the purposes of the valuation;

- the assumptions used are individually reasonable and appropriate in aggregate for the purposes of the valuation; and

- the methods employed are appropriate for the purposes of the valuation.

This report has been prepared, and our opinion given, in accordance with accepted actuarial practice in Canada. In particular, this report was prepared in accordance with the Standards of Practice (General Standards and Practice – Practice-Specific Standards for Pension Plans) published by the Canadian Institute of Actuaries.

We have reflected the impacts of the COVID-19 pandemic on the economic assumptions used in this report. It is important to note that the pandemic is a very fluid situation that will likely continue to evolve for some time. We have estimated the impacts based on the information known at the time the report was prepared. The final impacts of this health and economic crisis will likely generate some differences in the future.

In August 2020, the Treasury Board of Canada Secretariat communicated the Government of Canada’s pension funding risk appetite for the public sector pension plans to the Public Sector Pension Investment Board (PSPIB). This communication could result in changes to the allocation of the PSPIB assets but the timing and the details of those potential changes are uncertain. It is expected that expected rates of returns on assets used in future actuarial reports for the Plans will reflect any changes in the asset allocation when they occur.

To the best of our knowledge, after discussion with the Department of National Defence, there were no other events between the valuation date and the date of this report that would have a material impact on the results of this valuation.

Assia Billig, FCIA, FSA

Chief Actuary

Daniel Hébert, FCIA, FSA

Christopher Dieterle, FCIA, FSA

Ottawa, Canada

30 September 2020

Appendix A ― Summary of Pension Benefit Provisions

Pensions for members of the regular force were first provided under the Militia Pension Act of 1901, when in 1950 it became the Defence Services Pension Act until the Defence Services Pension Continuation Act and the Canadian Forces Superannuation Act (CFSA) were enacted in 1959. Benefits are also provided to members of the regular force under the Special Retirement Arrangements Act.

The enactment of Bill C-78 on 21 September 1999 gave authority to create a pension plan for the members of the reserve force. The Reserve Force Plan was established on 1 March 2007 and provides pension benefits to part-time members of the reserve force who meet the threshold requirements for becoming plan members. The benefit eligibility rules under this plan are the same as the rules that apply to Regular Force members starting on 1 March 2007.

Benefits under both the Regular Force Plan and the Reserve Force Plan may be reduced in accordance with the Pension Benefits Division Act if there is a breakdown of a spousal union.

Summarized in this appendix are the pension benefits, for both the Regular Force members and the Reserve Force members, provided under the CFSA registered provisions, which are in compliance with the Income Tax Act. For the Regular Force Plan, the portion of the benefits in excess of the Income Tax Act limits for the registered is provided under the RCA described in Appendix B.

The legislation shall prevail if there is a discrepancy between it and this summary.

A.1 Changes since the last valuation

The previous valuation report was based on the pension benefit provisions as they stood as at 31 March 2016. There were no changes to the plan provisions since the last valuation.

A.2 Membership

Regular Force membership in the Regular Force Plan is compulsory for all full-time members of the Canadian Forces.

As of 1 March 2007, a member of the reserve force is considered to be a member of the regular force and will become a member of the Regular Force Plan,

- on 1 March 2007 if, on that date,

- the member’s total number of days of paid Canadian Forces service during any period of 60 months beginning on or after 1 April 1999 was no less than 1,674,

- the member already was or became a member of the Canadian Forces during the first month of the period and remained a member of the Canadian Forces throughout the period without any interruption of more than 60 days,

- the member is not a person required to contribute to the Public Service Pension Fund or the Royal Canadian Mounted Police Pension Fund, and

- the member does not have any pensionable service to their credit under Part I of the CFSA;

- in any other case, on the first day of the month following a period of 60 months ending after 1 March 2007 if

- the member’s total number of days of paid Canadian Forces service during the period was no less than 1,674,

- the member already was or became a member of the Canadian Forces during the first month of the period and remained a member of the Canadian Forces throughout the period without any interruption of more than 60 days, and

- the member does not have any pensionable service to their credit under Part I of the CFSA.

The general rule is that, once a Reserve Force member is deemed a Regular Force member for the purposes of Part I of the CFSA and does not fail to receive pensionable earnings in any 12 consecutive months, the member remains a contributor under Part I of the CFSA as long as they remain a member of the Reserve Force. There are exceptions to the general rule previously described but for the purpose of this report, these were considered immaterial.

A member of the reserve force is deemed to become a participant in the Reserve Force Plan, defined under Part I.1 of the CFSA, if,

- during each of any two consecutive periods of 12 months beginning on or after 1 April 1999 and ending no later than 1 March 2007, the earnings that the member was entitled to receive were at least 10 per cent of the Annual Earnings ThresholdFootnote 7, provided that the member already was or became a member of the Canadian Forces during the first month of the first period and remained a member of the Canadian Forces, without any interruption of more than 60 days, until 1 March 2007; or

- in any other case, on the first day of the month following two consecutive periods of 12 months, the second of which ending after 1 March 2007 and during each of which the earnings that they were entitled to receive were at least 10 per cent of the Annual Earnings Threshold, provided that the member already was or became a member of the Canadian Forces during the first month of the first period and remained a member of the Canadian Forces, without any interruption of more than 60 days, throughout those two periods.

A.3 Contributions

A.3.1 Members

For Regular Force members, during the first 35 years of pensionable service, members contribute according to the rates shown in the following table. The contribution rates shown after calendar year 2021 are not final and are subject to change. After 35 years of pensionable service, members contribute only 1% of pensionable earnings.

| Calendar Year | 2019 | 2020 | 2021 | 2022 |

|---|---|---|---|---|

| Contribution rates on earnings up to the maximum covered by the Canada Pension Plan |

9.56% | 9.53% | 9.49% | 9.44% |

| Contribution rates on any earnings over the maximum covered by the Canada Pension Plan |

11.78% | 11.72% | 11.67% | 11.62% |

For Reserve Force members, during the first 35 years of pensionable service, members contribute 5.2% on all earnings up to 66 2/3 times the defined benefit limit as determined under the Income Tax Regulations. After 35 years of pensionable service, members contribute only 1% of pensionable earnings.

A.3.2 Government

A.3.2.1 Current Service

The government determines its normal monthly contribution as that amount which, when combined with the required member contributions in respect of current service and expected interest earnings, is sufficient to cover the cost, as estimated by the President of the Treasury Board, of all future payable benefits that have accrued in respect of pensionable service during that month and the administrative expenses incurred during that month.

A.3.2.2 Elected Prior Service

The government matches Regular Force member contributions credited under the Superannuation Account for prior service elections; however, no contributions are credited if the member is paying the double rate.

Government credits to the Canadian Forces Pension Fund in respect of elected prior service are as described for current service; however, if the member is paying the double rate the government contribution rate is generally adjusted so that total member and government contributions match the current service cost.

For Reserve Force members, this valuation assumes that the government will match member contributions for prior service elections.

A.3.2.3 Actuarial Excess and Surplus

In accordance with the CFSA, the government has the authority to:

- debit the excess of accounts available for benefits over the actuarial liability from the Superannuation Account subject to limitations, and

- deal with any actuarial surplus, subject to limitations, in the Canadian Forces Pension Fund as it occurs, either by reducing members and/or employer contributions or by making withdrawals.

The regulations under Part I.1 of the CFSA give the government the authority to deal with any actuarial surplus, subject to limitations, in the RFPF as it occurs by reducing employer contributions.

A.3.2.4 Actuarial Shortfall and Deficit

In accordance with the CFSA, if an actuarial shortfall under the Superannuation Account is identified through a statutory actuarial report, the actuarial shortfall can be amortized over a period of up to 15 years, such that the amount that in the opinion of the President of the Treasury Board will, at the end of the fifteenth fiscal year following the tabling of that report or at the end of the shorter period that the President of the Treasury Board may determine, together with the amount that the President of the Treasury Board estimates will be to the credit of the Superannuation Account at that time, meet the cost of the benefits payable in respect of pensionable service prior to 1 April 2000.

If an actuarial deficit under the CFPF is identified through a statutory actuarial report, the actuarial deficit can be amortized over a period of up to 15 years, such that the amount that in the opinion of the President of the Treasury Board will, at the end of the fifteenth fiscal year following the tabling of that report or at the end of the shorter period that the President of the Treasury Board may determine, together with the amount that the President of the Treasury Board estimates will be to the credit of the Canadian Forces Pension Fund at that time, meet the cost of the benefits payable in respect of pensionable service since 1 April 2000.

Similarly, if an actuarial deficit under the RFPF is identified through a statutory actuarial report, the RFPF is to be credited with such annual amounts that will fully amortize the actuarial deficit over a period of 15 years.

A.4 Summary Description of Benefits under the Regular Force Plan and the Reserve Force Plan

The objective of the Regular Force Plan and the Reserve Force Plan is to provide an employment earnings–related lifetime retirement pension to eligible members. Benefits to members in case of disability and to the spouse and children in case of death are also provided.

Regular Force member’s pension benefits are coordinated with the pensions paid by the CPP. The initial rate of a Regular Force member’s retirement pension is equal to 2% of the highest average of annual pensionable earnings over any period of five consecutiveFootnote 8 years, multiplied by the number of years of pensionable service not exceeding 35. The pension is indexed annually with the Consumer Price Index (CPI) and the accumulated indexation may be payable at age 55 at the earliest as defined in Note A.5.6. Entitlement to benefits depends on either the qualifying service in the Canadian Forces or the pensionable service, as defined below in Notes A.5.7 and A.5.8.

Reserve Force member’s pension benefits are equal to 1.5% of the greater of the Reserve Force member’s total pensionable earnings and total updated pensionable earnings over the most recent 35 years of pensionable service (i.e. Updated Career Average Plan). The Reserve Force Plan also provides a bridge benefit equal to 0.5% of the greater of the pensioner’s total bridge benefit earnings and total updated bridge benefit earnings over the most recent 35 years of pensionable service. Reserve Force pension and bridge benefits are indexed annually with the Consumer Price Index and the accumulated indexation may be payable at age 55 at the earliest, as defined in Note A.5.6.

Entitlement to benefits depends on either the qualifying service in the Canadian Forces or the pensionable service, as defined below in Notes A.5.7 and A.5.8.

Detailed notes on the following overview are provided in the following section.

A.4.1 Regular Force Member Benefit Entitlement on the Basis of Qualifying Service

A.4.1.1 Active Regular Force Members

| Type of Termination | Qualifying Service in the Canadian Forces (Note A.5.7) |

Benefit |

|---|---|---|

| Retirement on completion of short engagement (an officer other than a subordinate officer who has not reached retirement age and is not serving on an intermediate engagement or for an indefinite period of service) (Note A.5.9) | Less than 2 years | Return of contributions (Note A.5.11) |

| At least 2 but less than 25 years (less than 20 years – old terms of service) |

At option of member (1) deferred annuity (Note A.5.13); or (2) transfer value if under age 50 (Note A.5.14) |

|

| 25 years or more (20 years or more – old terms of service) |

See “Retirement for reasons other than those previously mentioned” |

|

| Retirement during an indefinite period of service after having completed an intermediate engagement and prior to reaching retirement age, for reasons other than disability or, to promote economy or efficiency | Any length | Immediate annuity to which member was entitled upon completion of intermediate engagement increased to such extent as prescribed by regulationTable A footnote * (Note A.5.15) |

| Retirement on completion of intermediate engagement (a member who has not reached retirement age and is not serving for an indefinite period of service) (Note A.5.10) |

25 years or more (20 years or more – old terms of service) |

Immediate annuity (Note A.5.12) |

| Compulsory retirement because of disabilityTable A footnote ** | Less than 2 years | Return of contributions (Note A.5.11) |

| At least 2 but less than 10 years |

At option of member (1) deferred annuity (Note A.5.13); or (2) transfer value if under age 50 (Note A.5.14) |

|

| 10 years or more | Immediate annuity | |

| Compulsory retirement to promote economy or efficiency | Less than 2 years | Return of contributions |

| More than 2 but less than 10 years |

At option of member (1) deferred annuity (Note A.5.13); or (2) transfer value if under age 50 (Note A.5.14) |

|

| At least 10 but less than 25 years (less than 20 years – old terms of service) |

At option of member (1) return of contributions; or (2) deferred annuity; or (3) transfer value if under age 50 (Note A.5.14) (4) with consent of the Minister of National Defence, an immediate reduced annuity (Note A.5.16) |

|

| 25 years or more (20 years or more – old terms of service) |

Immediate annuity (Note A.5.12) | |

| Retirement for reasons other than those previously mentioned | Less than 2 years | Return of contributions (Note A.5.11) |

| At least 2 but less than 25 years (less than 20 years – old terms of service) |

At option of member (1) deferred annuity (Note A.5.13); or (2) transfer value if under age 50 (Note A.5.14) |

|

| (At least 20 but less than 25 years – old terms of service) |

Immediate reduced annuity | |

| 25 years or more | Officer: - immediate reduced annuity (Note A.5.16); Other than officer: - immediate annuity (Note A.5.12) |

|

|

||

A.4.1.2 Benefits in Case of Death of an Active Regular Force Member

| Status at Death | Qualifying Service in the Canadian Forces (Note A.5.7) |

Benefit |

|---|---|---|

| Leaving no eligible spouse or children under 25 (Notes A.5.18 and A.5.19) |

Less than 2 years | Return of contributions |

| 2 years or more | Five times the annual amount of retirement pension to which the member would have been entitled at the date of death | |

| Leaving eligible spouse and/or children under 25 | Less than 2 years | Return of contributions or an amount equal to one month’s earnings of the deceased member for each year of credited pensionable service, whichever is the greater |

| 2 years or more | Annual allowance (Note A.5.20) |

A.4.1.3 Benefits in Case of Death of a Regular Force Pensioner

| Status at Death | Benefit |

|---|---|

| Leaving no eligible spouse or children under 25 | Minimum death benefit (Note A.5.21) |

| Leaving eligible spouse and/or children under 25 | Annual allowance (Note A.5.20) |

A.4.1.4 Regular Force Member Benefit Entitlement on the Basis of Pensionable Service

| Member’s Type of Termination | Benefit |

|---|---|

| With two or more years of pensionable service; and | |

|

|

| - With 20 years of service or more | Immediate annuity (Note A.5.12) |

| - Age 50 or over and 10 years of service or more | |

|

Deferred annuity (Note A.5.13) or Transfer Value (Note A.5.14) |

|

|

| - Age 60 or over, or age 55 or over and service 30 years or more | Immediate annuity (Note A.5.12) |

| - Otherwise | Deferred annuity (Note A.5.13) or annual allowance (Note A.5.20) |

A.4.2 Reserve Force Member Benefit Entitlement on the basis of “Pensionable” Service

| Member’s Type of Termination | Benefit |

|---|---|

| With less than two years of pensionable service | Return of contributions (Note A.5.11) |

| With two or more years of pensionable service; and | |

|

|

| - With 20 years of service or more | Immediate annuity (Note A.5.12) |

| - Age 50 or over and 10 years of service or more | |

|

|

| - Because of disability | Immediate annuity (Note A.5.12) |

| - Otherwise | Deferred annuity (Note A.5.13) or Transfer Value (Note A.5.14) |

|

|

| - Age 60 or over, or age 55 or over and service 30 years or more | Immediate annuity (Note A.5.12) |

| - Otherwise | Deferred annuity (Note A.5.13) or annual allowance (Note A.5.20) |

A.4.3 Reserve Force Member Benefit Entitlement on the basis of “Qualifying” Service

| Member’s Type of Termination | Benefit |

|---|---|

| Retirement on completion of 25 years or more of Canadian Forces service (Note A.5.7) | Immediate annuity (Note A.5.12) |

A.5 Explanatory Notes

A.5.1 Pensionable Earnings

For the Regular Force Plan, pensionable earnings means the salary at the annual rate prescribed by the regulations made pursuant to the National Defence Act together with the allowancesfor medical and dental care costs. Pensionable payroll means the aggregate pensionable earnings of all members with less than 35 years of pensionable service.

For the Reserve Force Plan, earnings means pay earned by a member of the Canadian Forces at the rates prescribed by the regulations made pursuant to the National Defence Act together with premiums in lieu of leave. Pensionable earnings means the earnings of a member with less than 35 years of pensionable service, who has completed the required two-year waiting period. Pensionable payroll means the aggregate pensionable earnings of all members.

A.5.2 Wage measure for Reserve Force Plan

Wage measure is

- for a calendar year prior to 2021, the corresponding rate of pay shown in Table 67 of this report; and

- for a calendar year after 2020, the greater of

- the standard basic rate of pay for a period of duty or training of six hours or more, before any retroactive adjustment, that was prescribed or established under the National Defence Act, to be paid on October 1 of the preceding year to a member at the rank of Corporal (class A), and

- the wage measure of the previous year.

A.5.3 Updated Pensionable Earnings for Reserve Force Plan

The updated pensionable earnings for a calendar year are the Reserve Force member’s pensionable earnings for that year, subject to the Income Tax Act limits, times A/B, rounded to the nearest fourth decimal place, where

A = the average of the wage measures for five years consisting of the year the member most recently ceased to be a member and the most recent years during which the member was a member and, if necessary, the years preceding all of those years, and

B = the wage measure for that calendar year.

A.5.4 Bridge Benefit Earnings for Reserve Force Plan

Bridge benefit earnings for a calendar year are the lesser of

- the member’s pensionable earnings for that year, and

- the Year’s Maximum Pensionable Earnings (YMPE) for that year.

A.5.5 Updated Bridge Benefit Earnings for Reserve Force Plan

Updated bridge benefit earnings for a calendar year are the lesser of