InfoPensions – Issue 24 – May 2021

InfoPensions includes announcements and reminders on matters relevant to federally regulated private pension plans including pooled registered pension plans. To receive email notifications of new items posted to OSFI’s website, including this newsletter and other pension-related documents, please subscribe using Email Notifications. If you have any questions about the articles you read in InfoPensions or if you have suggestions for future articles, please contact us at pensions@osfi-bsif.gc.ca. We expect to post the next issue of InfoPensions in November 2021.

Table of contents

Supervision

OSFI review of pension investments

The first goal in OSFI’s 2021-22 Departmental Plan is to improve the preparedness and resilience of federally regulated financial institutions (FRFIs) and pension plans to financial risk. This goal applies to both normal conditions and during the next financial stress event. To support this goal, OSFI’s key objectives for 2021-22 as they relate to pension plans include

- improving the consistency, accuracy and timeliness of risk assessments by OSFI and making our intervention more effective; and

- applying a more risk-based and principles-based approach to regulation and supervision.

According to the Departmental Plan, success in this goal will be characterized by pension plans having effective governance and risk management practices that keep pace with existing and emerging risks and that support the early detection of issues, among other things.

An important part of the work that OSFI and its Private Pension Plans Division (PPPD) are advancing to address this goal is to implement the recommendations stemming from our recently completed review of how we supervise defined benefit pension plan investments. This review looked at existing PPPD investment guidance, our supervisory approach and practices and the investment information that we collect through regular pension plan filings.

The PPPD team also engaged with pension investment consultants to understand their perspectives relating to current pension investment trends and potential sources of emerging risk. Finally, PPPD surveyed and had follow-up discussions with selected plans of different sizes and with different investment approaches to learn more about their investment processes, procedures and beliefs, as well as their investment risk management practices.

PPPD staff worked closely with OSFI supervisors of FRFIs to evaluate how their knowledge and perspective from supervising banks and insurance companies could help identify ways of improving PPPD’s own supervisory approach and regulatory guidance on pension plan investment risk management.

The review has enabled OSFI to develop a broad perspective on the general nature and level of inherent pension investment risks, and insights into the nature and quality of risk management. An analysis of findings has identified areas where additional OSFI guidance can help promote more robust investment risk management practices among the pension plans OSFI regulates.

PPPD intends to issue a discussion paper in late autumn 2021 that will propose a broad range of principles-based regulatory expectations relating to investment risk management practices. Because they will be principles-based, the proposed regulatory expectations will be both scalable and proportional, meaning that they can be adapted to reflect the relative complexity of different pension plans’ investment approaches and strategies.

The discussion paper will set out proposed directions for future PPPD regulatory guidance and expectations, and seek stakeholders’ input. PPPD will then consider that input before developing and releasing final guidance on investment risk management practices for pension plans.

Reminder to update contact information

Electronic communication is the method most used to communicate important changes and requirements to the pension plans OSFI regulates. A reminder that plan administrators have a responsibility to review and update their pension plan’s Organization Profile in the Regulatory Reporting System (RRS) as soon as changes occur. On occasion, when OSFI reaches out to plan administrators to provide relevant plan-related information, some emails bounce back which informs us that a number of plan administrators are not updating this information in a timely manner.

The Organization Profile for each pension plan includes primary contact information for individuals or organizations responsible for the various roles associated with the pension plan (e.g. plan administrator, pension fund custodian, actuarial firm, etc.). Instructions on how to update the Organization Profile can be found in the Manage Corporate Returns User Guide on the RRS Training and Support for Private Pension Plans page of OSFI’s website.

As previously communicated in InfoPensions – Issue 16 (November 2016), it is important for RRS users to be aware that updating information in RRS in the Organization Profile does not have the effect of updating the RRS access and filing permissions for the plan. Information on how to create, edit and deactivate RRS Portal Users’ and Local Registration Authority’s accounts is available in the Documents section of RRS. For further assistance, please contact the Bank of Canada at 1-855-865-8636 and follow the instructions to reach RRS Support.

FSRA/OSFI collaboration on defined contribution plans

In December 2020, OSFI and the Financial Services Regulatory Authority of Ontario (FSRA) established a special purpose technical advisory committee that will assist both regulators in developing better processes, guidance and approaches to regulation of the defined contribution plans.

Further information on this committee as well as meeting summaries are available on OSFI’s website.

Guidance and legislative matters

Revisions to the Directives and related FAQs

On February 25, 2021, OSFI revised the Directives of the Superintendent pursuant to the Pension Benefits Standards Act, 1985 (the Directives of the Superintendent). The revisions include

- the removal of the requirement to use a projected solvency ratio as of March 31, 2020 or later for portability transfers;

- the reinstatement of the pre-pandemic filing deadline for regulatory returns; and

- additions to recognize the revised commuted value standards issued by the Canadian Institute of Actuaries as they affect transfers from negotiated contribution plans.

New FAQs for the Directives of the Superintendent contain further information on the conditions currently applicable to portability transfers and annuity purchases.

OSFI also revised the Directives of the Superintendent pursuant to the Pooled Registered Pension Plans Act to reinstate the pre-pandemic filing deadline for regulatory returns.

OSFI has communicated changes to its expectations throughout the COVID-19 pandemic and has revised its FAQs to those that remain relevant. If you have a question that is not addressed in these (or other) FAQs, please send your question to information@osfi-bsif.gc.ca.

OSFI discussion paper on climate related risks in the financial sector

On January 11, 2021, OSFI launched a three-month consultation with the publication of a discussion paper Navigating Uncertainty in Climate Change: Promoting Preparedness and Resilience to Climate-Related Risks. The paper outlines climate-related risks that can affect the safety and soundness of federally regulated financial institutions and federally regulated pension plans. The consultation period ended on April 12, 2021 and OSFI is currently reviewing the submissions received from stakeholders.

Guidance Posted on OSFI’s website

This year, OSFI will be conducting a review of all of its pension related guidance to determine where changes are needed to reflect the 2020 Agreement Respecting Multi-Jurisdictional Pension Plans, the revised Standards of Practice for Pension Plans of the Canadian Institute of Actuaries and the revisions to the Directives of the Superintendent pursuant to the Pension Benefits Standards Act, 1985. In the meantime, if you have any questions regarding any existing discrepancies or inconsistencies in our guidance, please contact OSFI at information@osfi-bsif.gc.ca.

In addition to the revisions to the Directives and related FAQs noted in the earlier article, the following documents were posted to the OSFI website since the last edition of InfoPensions:

- May 2021 – the Instruction Guide for Termination of a Defined Benefit Pension Plan and the Instruction Guide for Termination of a Defined Contribution Pension Plan

- April 2021 – the Instruction Guide for Pooled Registered Pension Plan Annual Information Return, Auditor's Report and the Pension Plan Annual Corporate Certification

-

February 2021 – the Instruction Guide and Form for the Replicating Portfolio Information Summary (RPIS)

-

February 2021 – the Instruction Guide and Form for the Actuarial Information Summary (AIS)

-

January 2021 – the Instruction Guide and Form for the Solvency Information Return (SIR)

-

December 2020 – The Instruction Guide for Filing Pension Plan Amendments using the Regulatory Reporting System (RRS) and the revised OSFI 593: Defined Contribution Pension Plan Amendment Information Form and the OSFI 594: Defined Benefit / Combination Pension Plan Amendment Information Form

The InfoPensions – Issue 22 (November 2019) article indicated that plan administrators would be required to file most plan amendments through RRS as of April 1, 2020. The implementation date for this change was delayed to December 1, 2020 when the Instruction Guide was posted. As explained in the InfoPensions 22 article, amendments requiring the Superintendent’s authorization must continue to be submitted electronically to pensions@osfi-bsif.gc.ca.

-

December 2020 – Frequently Asked Questions on the Revised standards of practice for calculating commuted values. Please refer to the InfoPensions - Issue 23 (November 2020) article for more details on the revised standards.

-

December 2020 – The updated Life Income Fund (LIF), Restricted Life Income Funds (RLIF), and Variable Benefits Accounts Maximum Annual Payment Amount Table. The table was updated to include the factors applicable in 2021.

Actuarial

Estimated solvency ratio results

OSFI regularly estimates the solvency ratio for federally regulated pension plans with defined benefit provisions. The Estimated Solvency Ratio (ESR) results help identify any solvency issues that could affect the security of pension benefits promised to members and beneficiaries before a plan files their actuarial report. The ESR results also help identify broader trends.

The ESR results are calculated using the most recent actuarial, financial and membership information filed with OSFI for each plan before the analysis date. Assets are projected based on either the rate of return provided on the Solvency Information Return or an assumed rate of return for the plan. Solvency liabilities are projected using relevant commuted value and annuity proxy rates from the Canadian Institute of Actuaries. Expected contributions, benefit payments, and expenses are taken into account and an ESR based on the estimated adjusted market value of the fund and estimated liabilities is then calculated for each plan.

The median ESR for all 342 plans (down from 348 last year) increased to 0.97 as at December 31, 2020, up from 0.95 at the end of 2019. In contrast, the liability-weighted average ESR for all plans decreased slightly to 1.00 as at December 31, 2020, from 1.01 at the end of 2019. The graph below shows the current and previous ESRs and median ESRs dating back to December 2011.

Solvency Position of Pension Plans as at December 31 - Graph Description

| 2009 | 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Median ESR | 0.88 | 0.88 | 0.74 | 0.77 | 0.97 | 0.90 | 0.90 | 0.91 | 0.96 | 0.94 | 0.95 | 0.97 |

| Estimated Solvency Ratio (ESR) | 0.90 | 0.93 | 0.81 | 0.83 | 0.98 | 0.94 | 0.95 | 0.97 | 1.02 | 0.98 | 1.01 | 1.00 |

| ESR in excess of Median | 0.02 | 0.05 | 0.07 | 0.06 | 0.01 | 0.04 | 0.05 | 0.06 | 0.06 | 0.04 | 0.05 | 0.03 |

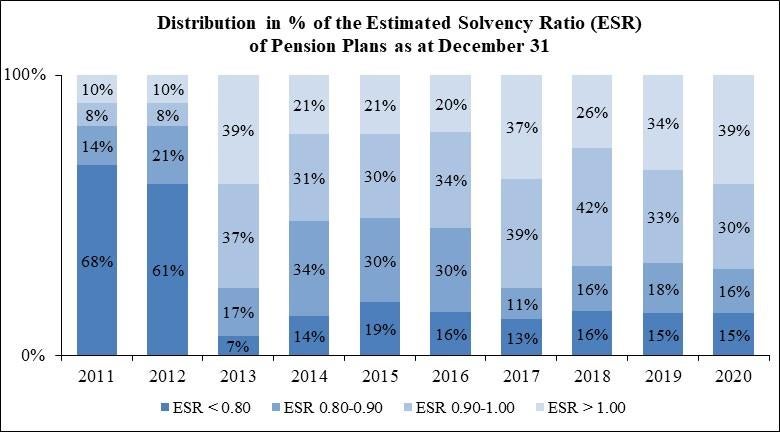

The most recent ESR results show a reduction in the percentage of plans that were underfunded (61% in 2020 versus 66% in 2019) while the number of plans that were significantly underfunded (ESRs below 0.80) did not change (15%). The bar graph below illustrates the distribution of the ESR results as at December 31 of each year since 2011. It shows the percentage of plans with ESRs below 0.80, between 0.80 and 0.90, between 0.90 and 1.00, and over 1.00 in each year.

Distribution in % of the Estimated Solvency Ratio (ESR) of Pension Plans as at December 31 - Graph Description

| 2011 | 2012 | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | |

|---|---|---|---|---|---|---|---|---|---|---|

| ESR < 0.80 | 68% | 61% | 7% | 14% | 19% | 16% | 13% | 16% | 15% | 15% |

| ESR 0.80-0.90 | 14% | 21% | 17% | 34% | 30% | 30% | 11% | 16% | 18% | 16% |

| ESR 0.90-1.00 | 8% | 8% | 37% | 31% | 30% | 34% | 39% | 42% | 33% | 30% |

| ESR > 1.00 | 10% | 10% | 39% | 21% | 21% | 20% | 37% | 26% | 34% | 39% |

| Average ESR | 81% | 83% | 98% | 94% | 95% | 97% | 102% | 98% | 101% | 100% |

Actuarial reports – Items warranting review

Actuarial reports submitted to OSFI are generally reviewed by each plan’s Relationship Manager in PPPD, who may refer the report to the division’s actuarial team for a more detailed review.

The Instruction Guide for the Preparation of Actuarial Reports for Defined Benefit Pension Plans sets out the reporting requirements for actuarial reports filed with OSFI. Based on the Canadian Institute of Actuaries (CIA) Standards of Practice, it is expected that plan actuaries provide sufficient details in their actuarial report to enable another actuary to assess the reasonableness of the data, assumptions, and methods used.

OSFI would like to share with plan actuaries its expectations relating to the following items that warranted a more detailed review in some actuarial reports:

Solvency valuation – Provision for termination expenses

In accordance with subsection 2(1) of the Pension Benefits Standards Regulations, 1985, solvency assets used in the determination of the solvency ratio for a pension plan with defined benefit provisions are equal to the market value of assets plus the face value of letters of credit minus the estimated expenses of winding-up the plan. OSFI expects the assumed termination expenses (also referred to as wind-up expenses) to be sufficient to provide for expenses that may reasonably be expected to be paid from the pension fund between the valuation date and the wind-up of the plan, i.e. the date when all plan benefits are settled and assets are distributed.

A comparison of the provision for termination expenses in recently filed termination reports to the assumed termination expenses in prior funding valuation reports for those plans shows that assumed termination expenses in the solvency valuation for an ongoing pension plan are often underestimated, sometimes by a significant amount.

While size can be a good indicator to assess the reasonableness of the provision for termination expenses, plan specific characteristics such as membership profile and the complexity of the plan’s provisions should also be considered. The determination of the provision should be consistent with the postulated termination scenario.

The termination expense provision would usually include

- actuarial, administrative, legal, and other consulting expenses incurred in terminating the plan up to its wind-up, including costs associated with locating individuals;

- expenses associated with benefit settlement, and, if applicable, fees associated with a replacement administrator or designated actuary;

- regulatory fees;

- custodial and auditing related expenses;

- investment expenses, including management and transaction fees relating to the liquidation of assets; and

- expenses associated with revising the investment policy.

In addition, the termination expense provision should allow time to

- prepare and file the termination report with OSFI;

- have the termination report reviewed by OSFI and approved by the Superintendent; and

- effectively pay the benefits.

Going concern valuation – Application of OSFI’s maximum discount rate

In accordance with the Instruction Guide for the Preparation of Actuarial Reports for Defined Benefit Pension Plans, it is OSFI’s position that the best estimate rate of return on assets used in the determination of the going concern discount rate should not exceed a certain level to ensure the assumption used by actuaries in their actuarial reports remains reasonable. OSFI monitors financial market conditions and future expected returns and is currently of the view that generally the discount rate for a plan with a fixed-income allocation of no more than 50% should not exceed 5.75%, before implicit margins for adverse deviations and expenses.

The actuary should ignore the return and expenses related to active investment management for determining whether the discount rate used in the actuarial report satisfies this requirement. However, the actuary should adjust the maximum rate for a plan using an asset mix expected to generate a lower return, and may adjust the maximum rate for a plan using an asset mix expected to generate a higher return, than that obtained by using a 50% fixed-income allocation.

The following examples illustrate how to apply OSFI’s maximum in the determination of the going concern discount rate under three scenarios:

- Scenario 1: the actuary has applied the unadjusted maximum of 5.75%

- Scenario 2: the actuary has adjusted the maximum to 6.00% based on the plan’s asset mix

- Scenario 3: the actuary has applied the unadjusted maximum of 5.75%, and can justify an assumption for value-added return of 0.10% due to active management

| Scenario 1 (%) |

Scenario 2 (%) |

Scenario 3 (%) |

|

|---|---|---|---|

| Best-estimate gross rate of return on assetsTable footnote 1 | 6.00 | 6.15 | 6.00 |

| Application of OSFI's maximum discount rate | (0.25) | (0.15) | (0.25) |

| Adjusted gross rate of return on assets | 5.75 | 6.00 | 5.75 |

| Margin for passive investment management expensesTable footnote 2 | (0.05) | (0.05) | (0.05) |

| Margin for administrative expenses | (0.20) | (0.20) | (0.20) |

| Margin for adverse deviations | (0.25) | (0.25) | (0.25) |

| Net rate of return on assets | 5.25 | 5.50 | 5.25 |

| Additional return due to active investment management | 0.15 | 0.15 | 0.25 |

| Margin for active investment management expenses | (0.15) | (0.15) | (0.15) |

| Going concern discount rate | 5.25 | 5.50 | 5.35 |

Regulatory filings and important dates

Filing through RRS and BoC Connect

In January 2021, the Bank of Canada and the Regulatory Reporting System (RRS) Support team sent emails to all filers regarding BoC Connect, the new login portal for RRS. The email provided instructions on setting up a BoC Connect account and temporary password. Please note that filers must now access RRS through the BoC Connect Login Page.

The recommended browsers for use with BoC Connect are Google Chrome or Microsoft Edge.

If you require assistance accessing RRS, please email the Bank of Canada at operations-consultation@bankofcanada.ca or call 1-855-865-8636.

Electronic filing of documents with OSFI – Update

In the 2016 article on Electronic Filing of Documents with OSFI, OSFI encouraged plan administrators, custodians, and other pension plan professionals and service providers to submit documents electronically where these documents were not required to be filed through the Regulatory Reporting System (e.g. applications that require the authorization of the Superintendent).

Please note that OSFI no longer expects scanned versions of pen and ink signed documents and will accept electronic signatures on electronically submitted documents. OSFI has also posted several FAQs regarding Electronic Communications.

Important reminders and dates

Annual filings must be filed using the Regulatory Reporting System (RRS).

Documents submitted in support of an application that requires the Superintendent’s authorization should be submitted electronically at pensions@osfi-bsif.gc.ca. There is no need to mail a hard copy of the application in addition to the electronic one.

Under the Pension Benefits Standards Act, 1985:

| Action or Required Filing | Deadline |

|---|---|

| All Plans: | |

| Annual Information Return (OSFI 49) and Schedule A – Canada Revenue Agency Information Requirements (OSFI 49A) | 6 months after plan year end |

| Pension Plan Annual Corporate Certification (PPACC) | 6 months after plan year end |

| Certified Financial Statements (OSFI 60), Auditor’s Report Filing Confirmation (ARFC) and, if required, an Auditor's Report | 6 months after plan year end |

| Plan Assessments | Payable upon receipt of the OSFI-issued invoice |

| Annual Statements to members and former members and their spouses or common-law partners | 6 months after plan year end |

| Defined Benefit Plans Only: | |

| Actuarial Report and Actuarial Information Summary and, if required, Replicating Portfolio Information Summary | 6 months after plan year end |

| Solvency Information Return (OSFI 575) | The later of 45 days after the plan year end or February 15 |

Under the Pooled Registered Pension Plans Act:

| Action or Required Filing | Deadline |

|---|---|

| Pooled Registered Pension Plan Annual Information Return (includes financial statements) | April 30 (4 months after the end of the year to which the document relates) |

| Pension Plan Annual Corporate Certification (PPACC) | April 30 (4 months after the end of the year) |

| Plan Assessments | Payable upon receipt of the OSFI-issued invoice |

| Annual statements to members and their spouses or common-law partners | February 14 (45 days after the end of the year) |

Other topics

ACPM Roundtable Broadcast

On May 13, 2021, Jeremy Rudin, the Superintendent of Financial Institutions, was the speaker for the Association of Canadian Pension Management’s (ACPM’s) Roundtable Broadcast – Emerging from 2020 into 2021 and Beyond: The Pension and Financial Sector Environment of Today and Tomorrow.

In his remarks, Superintendent Rudin addressed the importance of thinking beyond measures of financial risk to consider climate risk and other Environmental, Social and Corporate Governance (ESG) factors. The Superintendent then joined moderator and ACPM board member Ken Burns for a question and answer session with the audience.

A video recording of the ACPM’s Roundtable Broadcast can be found at the following link.

Pension Plans Survey

As part of its ongoing commitment to be responsive to stakeholder input and to continually improve performance, OSFI periodically consults with pension plan administrators and professional advisors through an online survey. Results from the last survey conducted in fall 2017 can be found on OSFI’s website.

This year’s survey was conducted by means of an online questionnaire and was administered by Phoenix Strategic Perspectives Inc., an independent third party. In the survey, respondents answered questions about their perceptions of OSFI’s performance including effectiveness at supervising pension plans and the measures OSFI put in place due to the COVID-19 pandemic. Thank you to all stakeholders who participated in the survey.

The results of the survey are expected to be available on OSFI’s website in late summer/early fall.

Upcoming retirements in the Private Pension Plans Division

Sylvia Bartlett, Manager of the Policy team in OSFI’s Private Pension Plans Division will be retiring at the end of June 2021. Claire Ezzeddin, who is currently on parental leave, will be taking on this role upon her return in July 2021.

Linda Steele, Senior Approvals Officer in OSFI’s Private Pension Plans Division will be retiring at the end of June 2021.