Business Specifications for the Climate-Related Risk Returns for Deposit-Taking Institutions (DTIs)

Information

Table of contents

Return files

Purpose

The purpose of the Climate Risk Returns is to collect standardized climate-related emissions and exposure data, directly from all institutions to enable OSFI to carry out evidence-based policy development, regulation, and prudential supervision as it pertains to climate risk management.

These returns capture data to enable quantification of the Deposit-Taking Institutions’ (DTIs’) 1) potential and realized physical risk exposures; and 2) potential transition risk exposures, as at fiscal year-end.

More specifically, these returns collect data on:

- asset exposures that are subject to physical risk, by geophysical location

- absolute greenhouse gas (GHG) emissions (Scopes 1, 2 and 3)

The data collection is confidential and will not be released publicly.

Application

These returns apply to all DTIs, except for foreign bank branches.

Frequency

Annual.

Filing Format

Returns are to be filed through RRS in .CSV format.

Implementation Date

These Returns are effective on or after October 31, for the following fiscal years:

- 2024, for Domestic Systemically Important Banks (DSIBs)

- 2025, for Small and medium size banks (SMSBs)

Reporting Date

The returns must be completed on a fiscal year-end basis and filed within 180 days of the fiscal year-end date.

For example, a DSIB with an October 31 fiscal year-end would complete its first return for the 2024 fiscal year, using data as at October 31, 2024 and file it by the end of April 2025. An SMSB with a December 31 fiscal year end would complete its first return for the 2025 fiscal year, using data as at December 31, 2025 and file it by the end of June 2026.

Contact Agency

Office of the Superintendent of Financial Institutions (OSFI).

Contact Person

For business and/or interpretation questions on the final version of the return, contact us through the Climate Risk Return email address: ClimateRiskReturn-ReleveRisquesClimatiques@osfi-bsif.gc.ca.

Key Terms and Definitions

| Key Term | Definition |

|---|---|

| Absolute emissions |

Volume of greenhouse gas (GHG) emissions expressed in tonnes of carbon dioxide-equivalent (CO2-e). For the purposes of this return, "absolute emissions" refers to generated emissions and not values relating to avoided emissions or emission removals. |

| Asset class |

A group of financial instruments that have similar financial characteristics. |

| Carbon dioxide-equivalent (CO2-e) |

The universal unit of measurement to show the global warming potential (GWP) of each of the seven greenhouse gases, expressed in terms of the GWP of one unit of carbon dioxide for 100 years. This unit is used to evaluate releasing different greenhouse gases against a common basis. |

| Exposure |

The book value of a facility or a position, or asset class thereof. |

| Financed Emissions |

Absolute greenhouse gas (GHG) emissions that DTIs and investors finance through their loans and investments. See absolute emissions. |

| Greenhouse gas (GHG) emissions |

Emissions of the seven greenhouse gases listed in the Kyoto Protocol–carbon dioxide (CO2); methane (CH4); nitrous oxide (N2O); hydrofluorocarbons (HFCs); nitrogen trifluoride (NF3); perfluorocarbons (PFCs); and sulphur hexafluoride (SF6). |

| Peril |

The four types of climate-related perils that may impact DTIs are : 1) wildfire, 2) flood, 3) Severe convective storms, and 4) hurricanes.

|

| Physical risks |

Risks resulting from climate change that can be event-driven (acute) or from longer-term shifts (chronic) in climate patterns. These risks may carry financial implications for entities, such as direct damage to assets, and indirect effects of supply-chain disruption. DTIs’ financial performance may also be affected by changes in water availability, sourcing and quality; and extreme temperature changes affecting entities’ premises, operations, supply chain, transportation needs and employee safety. |

| Scope 1 greenhouse gas (GHG) emissions |

Direct GHG emissions that occur from sources owned or controlled by the DTI —i.e., GHG emissions from combustion in owned or controlled boilers, furnaces, vehicles, etc. |

| Scope 2 greenhouse gas (GHG) emissions |

Indirect greenhouse gas (GHG) emissions from the generation of purchased or acquired electricity, steam, heating, or cooling consumed by the DTI. |

| Scope 3 greenhouse gas (GHG) emissions |

All other indirect GHG emissions (not included in Scope 2) that occur in the value chain of the reporting company. For the purposes of this return, Scope 3 emissions include the following categories (consistent with the GHG Protocol): (1) to (14) – DTI’s own emissions/Non-financed emissions Reporting requirements of these categories are to be determined (TBD) until further notice. Upstream:

Downstream:

See definitions of "Financed Emissions" above. |

| Transition risks |

Moving to a lower-carbon economy may entail extensive policy, legal, technology and market changes to address mitigation and adaptation requirements relating to climate change. Depending on the nature, speed and focus of these changes, transition risks may pose varying levels of financial and reputational risk to DTIs. |

| Value chain |

The full range of activities, resources and relationships related to a DTI’s business model and the external environment in which it operates. |

Units of Measurement for Reporting

Financial Figures

Reported financial figures, such as outstanding loan balances or investment security values, should be expressed in Canadian Dollars or Canadian Dollar Equivalent with no decimals and no commas, unless otherwise specified.

Greenhouse gas (GHG) Emissions

All reporting on Absolute GHG Emissions, including Scope 1, Scope 2 and Scope 3 emissions should be reported in metric tons of carbon dioxide-equivalent (tCO2-e).

Probabilities and Percentages

All probabilities and percentages should be reported as their decimal equivalents. For example, a probability of default (PD) of 1.09% should be reported as 0.01090.

Greenhouse gas emissions accounting

Regarding calculation of GHG emissions, the DTI is expected to use the latest GHG Protocol Corporate Accounting and Reporting Standard and the latest GHG Protocol Corporate Value Chain (Scope 3) Accounting and Reporting Standard.

Regarding calculation of the portion(s) of Scope 3 GHG emissions, pertaining to the DTI’s financed, and/or insurance-associated GHG emissions, the DTI is expected to use the latest Partnership for Carbon Accounting Financials’ (PCAF’s) Global GHG Accounting and Reporting Standard for the Financial Industry (PCAF Standard).

OSFI recognizes that there is often a lag between financial reporting and required data becoming available, such as a bank’s counterparty emissions data. Accordingly, for Financed GHG Emissions, the DTI may use the most recently available emissions-related data from entities within its value chain alongside its own current year financial data. For example, when filing for fiscal year 2024, use financial data for fiscal year 2024 and GHG emissions data for fiscal year 2023.

While there is no defined maximum lookback period, a duration of two years or less is recommended. DTIs should indicate in their supplemental notes if the lookback period exceeds two years.

Structure of the Climate-Related Risk Returns for DTIs

Tabular Structure of the Climate-Related Data Return Templates

Each data return is structured to contain three types of data fields:

- Sub-Table Field

- Categorical Data Fields

- Calculated Data Fields

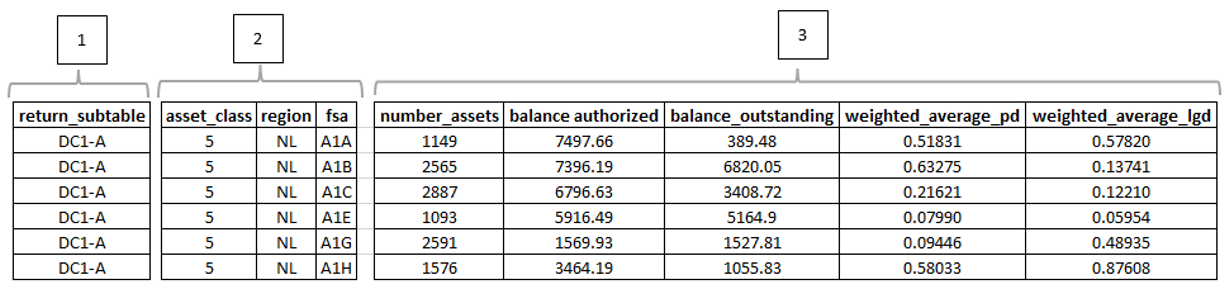

An illustration, using an example from the structure of the DC1 (OSFI 1000) Return, is shown below.

- Sub-Table Field: This data field is used to report the Sub-Table of the return (

return_subtable). See the section Return Sub-Tables below for further details. - Categorical Data Fields: These data fields are used to report qualitative data that are mutually exclusive. Categorical fields used in the Climate-Related Risk Returns for DTIs has submission keys as follows:

asset_class,region,sector,credit_qualityandfsa. - Calculated Data Fields: The data reported in these fields are to be calculated to reflect the maximum granularity established by the applicable Categorical Data Fields, unless otherwise noted. Referencing the illustration above, the number of loans reported as 1149 in the first row in the field

number_assetswould represent (be calculated as) the count of assets (loans) in the Forward Sortation Area (fsa)Footnote 1 A1A that are of theasset_classcode ‘5’ (‘PSE’).

Reference Format

Submission keys that identify each data field being collected are included in the first row of each template. For ease of identification within this document, submission keys are formatted in lower case with underscored spacing, such as return_subtable.

For categorical fields, categorical codes and their related values are listed in single quotes, such as code ‘19’ and ‘Commercial Real Estate’ respectively.

Categorical Field Selections

Tables listing the comprehensive list of the codes (range of expected values) applicable to each of the categorical fields, other than fsa, are provided in the appendices to this document as follows:

- Appendix I – Asset Classes

- Appendix II – Regions

- Appendix III – Sectors

- Appendix IV – Credit Quality Ratings

These tables correspond to those included in the input templates for the DC1 (OSFI 1000) and DC2 (OSFI 1001) returns.

Return Sub-Tables

For reporting purposes, each return consists of a single data table that are divided into sub-tables that group related reporting data elements. The sub-tables for each of the returns are as follows:

| Return Sub-Table Name | Return Sub-Table Code | Applicable DTIs |

|---|---|---|

| Exposures and Credit Risk Metrics – In Canada by FSA | DC1-A | DSIBs, SMSBs |

| Exposures and Credit Risk Metrics – Outside of Canada by Region | DC1-B | DSIBs, SMSBs |

| Return Sub-Table Name | Return Sub-Table Code | Applicable DTIs |

|---|---|---|

| Entity-level DTI’s Own GHG Emissions by Scope | DC2-A | DSIBs, SMSBs |

| Financed GHG Emissions by Asset Class | DC2-B | DSIBs, SMSBs |

Field Applicability by Sub-Table

The fields applicable for each Sub-Table are outlined in the Field Applicability Matrices document (XLSX, 166.86 KB). As shown in the Field Applicability Matrices, the calculated fields are to be reported based upon the Return Sub-Table and the asset_class field value for both the DC1 (OSFI 1000) and DC2 (OSFI 1001) returns. Non-applicable fields should be reported as blank on each row.

Instructions for the Physical Risk Return DC1 (OSFI 1000)

This return collects foundational risk exposures and select credit risk data at an FSA level of geophysical granularity for on-balance sheet loans and securities that may be subject to climate-related physical risk from DTIs within Canada. For exposures outside of Canada, data is collected at a broader regional level.The Physical Risk returns (DC1A and DC1B) apply only to on-balance sheet instruments, specifically loans and securities. The data collected will be combined with other climate peril data to assess DTIs’ exposures to physical risk.

Overview of Return Data Fields

The following fields are included in the DC1 (OSFI 1000) return template:

Sub-Table Field

return_subtable

Categorical Data Fields

asset_classregionfsaapproach_to_credit_risk

Calculated Fields

number_assetsbalance_authorizedbalance_outstandingweighted_average_pdweighted_average_lgd

The above fields are to be reported by completing the template contained in the technical specifications document (XLSX, 34.15 KB) provided, following the instructions below for reporting loan exposures and credit metrics applicable in Canada and outside of Canada.

Field Applicability by Sub-Table

The fields applicable for each Sub-Table are outlined in the Field Applicability Matrices (See Link: Field Applicability Matrices document (XLSX, 166.86 KB)).

Sub-Table DC1-A: Exposures and Credit Risk Metrics – In Canada

Report on all fields in the template loans and securities from borrowers and investees secured by assets residing in Canada on each row, per the instructions by submission key below.

Sub-Table Field

return_subtable– Set field value to ‘DC1-A’

Categorical Data Fields

asset_class– Report the applicableasset_classcode per table in Appendix I – Asset Classes.region– Report the province or territory of Canada of the reportedfsaif applicable.fsa– Report the 3-digit Forward Sortation Area (FSA) location reference of the borrowers/assets, for Canadian addresses only. If the DTI’s reported assets, such as borrowings that are tied to physical location of assets for certain large accounts, such as corporates, banks or sovereign borrowers (e.g. Government of Canada) that cannot be specifically divided across multiple FSAs using available client data, DTIs should report using the code ‘ZZZ’ for the FSA.approach_to_credit_risk– Using Table C, report the codes for the credit risk approach (IRB or Standardized Approach) for each field: number of assets, authorized balance, outstanding balance, and weighted average PDs and LGDs. Code 1 (IRB) applies to DTIs with approved AIRB models only. Standardized banks should always use Code 2.

| Code | Approach to credit risk |

|---|---|

| 1 | Internal Ratings-Based (IRB) Approach |

| 2 | Standardized Approach |

Calculated Data Fields

number_assets– Report the count of the assets (e.g., non-residential mortgage loans) outstanding for a givenasset_classin each reportedfsa. The number of assets should align with the credit risk approach identified by the financial institution.balance_authorized– Report the sum of the maximum gross dollar amounts of exposure authorized within a givenasset_classin each reportedfsa.The balance authorized should align with the credit risk approach identified by the financial institution.balance_outstanding– The sum of gross amounts of exposures outstanding for a givenasset_classin each reportedfsa. The balance outstanding should align with the credit risk approach identified by the financial institution.weighted_average_pd– Report the exposure weighted (i.e. weighted by the outstanding balance) average probability of default for theasset_classin each reportedfsawhere applicable.Please refer to Table C and specify the credit risk approach used to calculate PD.weighted_average_lgd– Report the exposure weighted (i.e. weighted by the outstanding balance) average LGD for theasset_classin each reportedfsa. Please refer to Table C and specify the credit risk approach used to calculate LGD.

Amounts reported for balance_authorized and balance_outstanding should be calculated as the sums of each type of exposure at the appropriate level of granularity. weighted_average_pd and weighted_average_lgd reported should reflect the exposure weighted average (weighted by the outstanding balance) for each asset_class for each fsa.

Note

General guidance:

- The Climate Risk Returns (CRRs) utilize BCAR asset classes; however, they are not intended as a capital assessment exercise.

- Asset class balances reported in the DC1 returns should reflect pre-CAR capital adjustments and align with the corresponding notional amounts in BCAR.

Asset Classes not in scope for Physical Risk DC1 Returns:

- Exposures related to Guarantees and Letters of credit, Counterparty Credit Risk, including Derivatives, Securities Financing Transactions, Repo-style exposures, and CVA exposures, fall outside the scope of the Physical Risk DC1 Return.

Clarifications of source for Forward Sortation Area (FSA) Codes:

- DTIs should use the latest version of the Canada Post FSA codes.

Definition of the “Equity Investment in Fund – Public/Private Equity” asset classes:

- The “Equity Investment in Fund – Public/Private Equity” asset classes in DC1 - Physical Risk Returns and “Equity Investment in Fund - Public Equity” in DC2 - Transition Risk Returns includes only on-balance sheet investments.

Scope 3 – Non-Financed (DTI’s Own) and Financed Emissions Categories:

- Scope 3 Categories 1–14 (DTI’s Own Emissions) removed from the CRR and related documents.

- Scope 3 Category 15 (financed emissions): disaggregation by Scope 1 and 2 components is optional.

Sub-Table DC1-B: Exposures and Credit Risk Metrics – Outside Canada (By Region)

Report on all fields in the template loans and investments to borrowers and investees secured by assets residing outside Canada per the instructions by submission key below. However, the fsa data field should be reported as blank on each reported row.

Sub-Table Field

return_subtable– Set field value to ‘DC1-B’ on each row reported

Categorical Data Fields

asset_class– Report the applicableasset_classcode per table in Appendix I – Asset Classes.region– Report the applicable code for eachregionof the USA and the ‘Other’ geographic region per the table in Appendix II – Regions on each row reported. If the DTI’s reported assets, such as borrowings that are tied to physical location of assets by for large client accounts in the USA, such as corporates, banks or sovereign borrowers that cannot be specifically divided across multiple regions using available client data, DTIs should report using theregion‘USA-Other’.fsa– Report as blank (this field is applicable In Canada only)approach_to_credit_risk– Using Table C, report the codes for the credit risk approach (IRB or Standardized Approach) for each field: number of assets, authorized balance, outstanding balance, and weighted average PDs and LGDs. Code 1 (IRB) applies to DTIs with approved AIRB models only. Standardized banks should always use Code 2.

| Code | Approach to credit risk |

|---|---|

| 1 | Internal Ratings-Based (IRB) Approach |

| 2 | Standardized Approach |

Calculated Data Fields

number_assets– Report the count of the loans or securities outstanding for a givenasset_classin each reportedregion. The number of assets should align with the credit risk approach identified by the financial institution.balance_authorized– Report the sum of the maximum gross dollar amounts of exposure authorized within a givenasset_classin each reportedregion. The balance authorized should align with the credit risk approach identified by the financial institution.balance_outstanding– The sum of gross amounts of exposures outstanding for a givenasset_classin each reportedregion. The balance outstanding should align with the credit risk approach identified by the financial institution.weighted_average_pd– Report the exposure weighted (weighted by the outstanding balance) average probability of default for theasset_classin each reportedregion. Please refer to Table C and specify the credit risk approach used to calculate PD.weighted_average_lgd– Report the exposure-weighted (weighted by the outstanding balance) average LGD for each applicableasset_classin each reportedregion. Please refer to Table C and specify the credit risk approach used to calculate LGD.

Amounts reported for balance_authorized and balance_outstanding should be calculated as the sum of each type of exposure for each asset_class for each region that is outside of Canada. weighted_average_pd and weighted_average_lgd should be calculated to reflect the exposure weighted average (weighted by the outstanding balance) for each applicable asset_class for each region that is outside of Canada.

Additional Reporting Guidance

The technical specifications document for the DC1 (OSFI 1000) return (XLSX, 34.15 KB), that includes a template sheet, field definitions and reference tables is available. For a reference example of a completed template that contains an abbreviated listing of completed rows following the above DC1 (OSFI 1000) template instructions, see the sample DC1 (OSFI 1000) Return template (CSV, 3.66 KB).

Instructions for the Transition Risk Return DC2 (OSFI 1001)

This return collects entity-level absolute GHG emissions by scope, including scope 3 financed emissions associated with on-balance sheet loans and investments. Therefore, the Transition Risk returns (DC2A and DC2B) cover only on-balance sheet instruments, specifically loans and investment.

Overview of Return Data Fields

The following fields are included in the DC2 (OSFI 1001) Return templates:

Sub-Table Field

return_subtable

Categorical Data Fields

asset_classsectorregioncredit_quality

Calculated Fields

scope_1_dti_own_emissionsscope_2_dti_own_emissionsscope_1_counterparty_absolute_emissionsscope_2_counterparty_absolute_emissionsscope_3_counterparty_absolute_emissionsweighted_avg_scope_1_counterparty_data_quality_scoreweighted_avg_scope_2_counterparty_data_quality_scoreweighted_avg_counterparty_data_quality_scoreweighted_avg_scope_3_counterparty_data_quality_scoreasset_balanceweighted_average_maturitybalance_5_maturitybalance_10_maturity

The above fields are to be reported by completing the template contained in the technical specifications document (XLSX, 37.74 KB) provided, following the instructions below for reporting loan exposures and credit metrics applicable in Canada and outside of Canada.

Field Applicability by Sub-Table

The fields applicable for each Sub-Table are outlined in the Field Applicability Matrices (See Link: Field Applicability Matrices document (XLSX, 166.86 KB)).

Sub-Table DC2-A: Entity-level GHG Emissions by Scope

Report emissions by scope for each row using the instructions by submission key below.

Sub-Table Field

return_subtable– Report field value as ‘DC2-A’

Categorical Data Fields

asset_class– Set field value to code ‘17’ (‘Unattributable – GHG emissions unattributable to a specific asset’) for each row reported; reporting on other asset categories is not applicable for Sub-Table DC2-A (see Field Applicability by Sub-Table section above for details)sector– Not applicable; report as blankregion– Report theregioncode applicable province or territory of Canada, Region of USA or ‘Other’ geographic region per the table in Appendix II – Regionscredit_quality– Not applicable; report as blank

Calculated Data Fields

scope_1_dti_own_emissions– Report the DTI’s own Scope 1 Absolute GHG Emissions (in tCO2-Equivalent) produced within each reportedregionscope_2_dti_own_emissions– Report the DTI’s own Scope 2 Absolute GHG Emissions (in tCO2-Equivalent) within each reportedregion- Report the following fields as blank on each row:

asset_balanceweighted_average_maturitybalance_5_maturitybalance_10_maturity

Sub-Table DC2-B: Financed GHG Emissions by Asset Class

For purposes of reporting Scope 3 Financed Emissions, report on each row using the instructions by submission key below.

Sub-Table Field

return_subtable– Set field value to ‘DC2-B’

Categorical Data Fields

asset_class– Report on each of the defined asset categories (see table in Appendix I – Asset Classes for reference). Do not report usingasset_classcode ‘17’ (‘Unattributable – GHG emissions unattributable to a specific asset’) for reporting on Financed GHG Emissions. For each selection within theasset_class, certain categorical fields may be applicable (see Field Applicability by Sub-Table section above for reference). Asset Classes 17 (Unattributable Emissions) is applicable only to non-financed emissions (DTI’s own).sector– If applicable per the Field Applicability Matrices, report the applicablesectorcode for eachasset_classper the table in Appendix III – Sectors; otherwise report thesectorfield for each of the non-applicable rows as blankregion– If applicableregioncode for the applicableasset_classper the Field Applicability Matrices, report the applicable province or territory of Canada, Region of USA or ‘Other’ geographic region per the table in Appendix II – Regions; If the DTI’s reported assets, such as borrowings that are tied to physical location of assets by for certain large accounts, such as corporates, banks or sovereign borrowers that cannot be specifically divided across multiple regions using available client data, filers should report using ‘Canada-Other’ and/or ‘USA-Other’ in theregionfield.credit_quality– If applicable for theasset_classper the Field Applicability Matrices, report the applicablecredit_qualitycode for each row per the table in Appendix IV – Credit Quality Ratings; otherwise, report thecredit_qualityfield for the non-applicable rows as blank

Calculated Fields

The disaggregation of Scope 3 Category 15 (financed emissions) into Scope 1 and 2 components is optional.

Finance GHG Emissions Reporting

Optional disaggregation:

scope_1_counterparty_absolute_emissions– Report the applicable amount of the DTI’s counterparty Scope 1 Absolute GHG Financed Emissions for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).scope_2_counterparty_absolute_emissions– Report the applicable amount of the DTI’s counterparty Scope 2 Absolute GHG Financed Emissions for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).

Mandatory (if combined Scope 3 reporting is used):

scope_3_counterparty_absolute_emissions– Report the applicable amount of the DTI’s counterparty Scope 3 Absolute GHG Financed Emissions for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).

Data Quality Scores

Optional disaggregation:

weighted_avg_scope_1_counterparty_data_quality_score– Report the PCAF Data quality score for the DTI's counterparty Total Absolute Emissions (Scope 1) weighted by outstanding amount for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).weighted_avg_scope_2_counterparty_data_quality_score– Report the PCAF Data quality score for the DTI's counterparty Total Absolute Emissions (Scope 2) weighted by outstanding amount for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).weighted_avg_counterparty_data_quality_score– Report the PCAF Data quality score for the DTI's counterparty Total Absolute Emissions (Scope 1) and (Scope 2) weighted by outstanding amount for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).

Mandatory (if combined Scope 3 reporting is used):

weighted_avg_scope 3_counterparty_data_quality_score– Report the PCAF Data quality score for the DTI's counterparty Total Absolute Emissions (Scope 3) weighted by outstanding amount for eachasset_classby eachregioncategory (if applicable) by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).

Exposure and Maturity Metrics

asset_balance– report the applicable (on-balance sheet) amount outstanding in dollar for eachasset_classby eachregioncategory (if applicable) split by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).weighted_average_maturity– report the applicable exposure weighted (weighted by the outstanding balance) remaining maturity of the contract (not the effective maturity used in the IRB RWA formula), measured in years, for eachasset_classsplit by eachregioncategory by eachsectorcategory (if applicable) by eachcredit_qualitycategory (if applicable).balance_5_maturity– report the dollar amount of theasset_balancewith a remaining maturity of either exactly 5 years or between 5 and 10 years.balance_10_maturity– report the dollar amount of theasset_balancewith a remaining maturity greater or equal to 10 years.

Additional Reporting Guidance

The technical specifications document for the DC2 (OSFI 1001) return (XLSX, 37.74 KB), that includes a template sheet, field definitions and reference tables is available. For a reference example of a completed template that contains an abbreviated listing of completed rows following the above DC2 (OSFI 1001) template instructions, see the sample DC2 (OSFI 1001) Return template (CSV, 5.5 KB).

Appendix I – Asset Classes

- The coding selections below reflect the asset classifications of the Capital Adequacy Requirements (CAR) Guideline.

- The DC1 (OSFI 1000) – Physical Risk Returns cover only on-balance sheet instruments loans and securities.

DC1 (OSFI 1000) – Physical Risk Returns

The coding provided in the table below should be used for the asset_class field when completing the following DC1 (OSFI 1000) Returns:

- Sub-Table DC1-A: Exposures and Credit Risk Metrics – In Canada by FSA

- Sub-Table DC1-B: Exposures and Credit Risk Metrics – Outside of Canada

Report in the asset_class field using the codes shown below.

asset_class |

Asset Class Names |

|---|---|

| 1 | Sovereign and Central Bank - Bond |

| 2 | Sovereign and Central Bank - Loan |

| 5 | PSE |

| 7 | Corporate - Loans |

| 8 | Regulatory Retail |

| 9 | Other Retail - Auto Loan |

| 10 | Residential Real Estate - Mortgage - CMHC Insured |

| 11 | Residential Real Estate - Mortgage - Other Insured |

| 12 | Residential Real Estate - Mortgage - Not Insured |

| 13 | Residential Real Estate - HELOC |

| 14 | Commercial Real Estate |

| 15 | Reverse Mortgages |

DC2 (OSFI 1001) – Transition Risk Returns

- The DC2 (OSFI 1001) – Transition Risk Returns cover only on-balance sheet instruments loans and investments.

Sub-Table DC2-A: Entity-level DTI Own GHG Emissions by Scope (Canada and outside of Canada)

The ‘Unattributable – GHG emissions unattributable to a specific asset’ asset class is to be used for reporting on entity-wide emissions in the DC2 return sub-table 'DC2-A' only, and it is not intended to be used in lieu of reporting emissions by specific asset classes in DC2 return sub-table 'DC2-B'.

The coding provided in the table below should be used for the the asset_class field when completing the DC2 (OSFI 1001) Returns.

asset_class |

Asset Class Names |

|---|---|

| 17 | Unattributable – GHG emissions unattributable to a specific asset |

Note

Asset Classes 17 (Unattributable GHG Emissions) is applicable only to non-financed emissions (DTI’s own).

Sub-Table DC2-B: Financed GHG Emissions by Scope (Canada and outside of Canada)

The coding selections below reflect the asset classifications of the Capital Adequacy Requirements (CAR) Guideline except:

- “Sovereign and central bank – bond” excludes sub-sovereigns, central banks and supranationals

- “Sovereign and central bank – loan” excludes sub-sovereigns, central banks and supranationals

Sub-table DC2-B should be completed using the selected coding included in the table below.

asset_class |

Asset Class Names |

|---|---|

| 3 | Sovereign and central bank - Bond (excluding sub-sovereigns, central banks and supranationals) |

| 4 | Sovereign and central bank - Loan (excluding sub-sovereigns, central banks and supranationals) |

| 6 | Corporate - Securities |

| 7 | Corporate - Loans |

| 9 | Other Retail - Auto Loan |

| 10 | Residential Real Estate - Mortgage - CMHC Insured |

| 11 | Residential Real Estate - Mortgage - Other Insured |

| 12 | Residential Real Estate - Mortgage - Not Insured |

| 14 | Commercial Real Estate |

| 15 | Reverse Mortgages |

| 16 | Equity Investment in Fund - Public Equity |

Appendix II – Regions

The categorical codes shown in the table below are to be used for the region field when completing the DC1 (OSFI 1000) Return and the DC2 (OSFI 1001) Return. The name for each region, along with a Region Description that lists the constituent region(s) associated to each Region code are also listed in the table below. For example, the region code ‘US2’, described as ‘USA Midwest’ is constituted of a grouping of states of the USA including: ‘IA’, ‘IL’, ‘IN’, ‘KS’, ‘MI’, ‘MN’, ‘MO’, ‘ND’, ‘NE’, ‘OH’, ‘SD’, and ‘WI’.

Report in the region field using the codes shown below.

region |

Region Name | Region Description |

|---|---|---|

| AB | Alberta, Canada | Alberta, Canada |

| BC | British Columbia, Canada | British Columbia, Canada |

| MB | Manitoba, Canada | Manitoba, Canada |

| NB | New Brunswick, Canada | New Brunswick, Canada |

| NL | Newfoundland and Labrador, Canada | Newfoundland and Labrador, Canada |

| NT | Northwest Territories, Canada | Northwest Territories, Canada |

| NS | Nova Scotia, Canada | Nova Scotia, Canada |

| NU | Nunavut, Canada | Nunavut, Canada |

| ON | Ontario, Canada | Ontario, Canada |

| PE | Prince Edward Island, Canada | Prince Edward Island, Canada |

| QC | Quebec, Canada | Quebec, Canada |

| SK | Saskatchewan, Canada | Saskatchewan, Canada |

| YK | Yukon, Canada | Yukon, Canada |

| C1 | Canada-Other | Unattributable to a single location in Canada |

| U1 | USA West | Region of USA that includes the following US States: AK, CA, CO, HI, ID, MT, NV, OR, UT, WA, WY |

| U2 | USA Midwest | Region of USA that includes the following US States: IA, IL, IN, KS, MI, MN, MO, ND, NE, OH, SD, WI |

| U3 | USA Northeast | Region of USA that includes the following US States: CT, MA, ME, NH, NJ, NY, PA, RI, VT |

| U4 | USA Southwest | Region of USA that includes the following US States: AZ, NM, OK, TX |

| U5 | USA Southeast | Region of USA that includes the following US States: AL, AR, DE, FL, GA, KY, LA, MD, MS, NC, SC, TN, VA, WV as well as DC |

| U6 | USA-Other | Unattributable to a single location in the USA |

| ZZ | Other | All other regions worldwide |

| ZZZ | FSA level reporting | Unattributable to a single FSA in Canada for DC1-A reporting |

Appendix III – Sectors

The coding selections shown in Table 1 below are to be used for the sector field when completing the DC2 Return.

Table 1 lists 17 Sectors, most of which are sensitive to the transition toward a low-carbon economy, starting with Sector codes ‘1’ (‘COAL – Coal Industry and Support ’) and ending with codes ‘17’ (‘OTHR’- ‘Other Industries).

Report the sector field using the codes shown below (Table 1).

| Code | Sector | Sector description | Industry |

|---|---|---|---|

| 1 | COAL | Coal Industry and Support | Fossil Fuels |

| 2 | CROP | Crop Production and Support | Agriculture and Forestry |

| 3 | EINT-MANF | Manufacturing | Energy Intensive Industries |

| 4 | EINT-OTHR | Paper and Pulp; Mining; Water and Sewage System and Waste Management | Energy Intensive Industries |

| 5 | ELEC-FOSS | Fossil Fuel Electricity Production | Electricity Support and Distribution |

| 6 | ELEC-OTHR | Electricity Production from Renewable Sources and Nuclear; Electricity Support and Distribution; Hydro Electricity Production; | Electricity Support and Distribution |

| 7 | GAS | Natural Gas Industry and Support | Fossil Fuels |

| 8 | LIVE | Livestock Production and Support | Agriculture and Forestry |

| 9 | OIL-EXTR | Oil Extraction | Fossil Fuels |

| 10 | OIL-OTHR | Oil Extraction Support | Fossil Fuels |

| 11 | OIL-SAND | Sand Oil Extraction and Support | Fossil Fuels |

| 12 | REST | Real Estate and Rental and Leasing | Other Sectors |

| 13 | RFND | Fossil Fuel Refinery | Fossil Fuels |

| 14 | TRNS-AIR | Air Transportation | Transportation |

| 15 | TRNS-OTHR | Other Transportation | Transportation |

| 16 | TRNS-RAIL | Rail Transportation | Transportation |

| 17 | OTHR | All other sectors | Other Industries |

Appendix IV – Credit Quality Ratings

Externally assigned ratings of long-term borrower creditworthiness are assigned on debt security issuers and wholesale borrowers including corporates, banks and sovereigns. To facilitate comparison, ratings from several recognized credit rating organizations should be mapped into the credit_quality categories shown in the table below. For reporting purposes on the DC2 (OSFI 1001) return, borrowers should be grouped within each credit_quality category; borrowers are not to be reported individually.

Report in the credit_quality field using the codes shown below.

credit_quality |

S&P | DBRS | Moody’s | Fitch | KBRA |

|---|---|---|---|---|---|

| 1 | AAA to AA− | AAA to AA (low) | Aaa to Aa3 | AAA to AA− | AAA to AA− |

| 2 | A+ to A− | A (high) to A (low) | A1 to A3 | A+ to A− | A+ to A− |

| 3 | BBB+ to BBB− | BBB (high) to BBB (low) | Baa1 to Baa3 | BBB+ to BBB− | BBB+ to BBB− |

| 4 | BB+ to BB− | BB (high) to BB (low) | Ba1 to Ba3 | BB+ to BB− | BB+ to BB− |

| 5 | B+ to B− | B (high) to B (low) | B1 to B3 | B+ to B− | B+ to B− |

| 6 | Below B− | CCC or lower | Below B3 | Below B− | Below B− |

| 7 | Not Rated | Not Rated | Not Rated | Not Rated | Not Rated |