Actuarial Report on the Canada Student Financial Assistance Program as at 31 July 2021

Accessibility statement

The Web Content Accessibility Guidelines (WCAG) defines requirements for designers and developers to improve accessibility for people with disabilities. It defines three levels of conformance: Level A, Level AA, and Level AAA. This report is partially conformant with WCAG 2.0 level AA. If you require a compliant version, please contact webmaster@osfi-bsif.gc.ca.

Office of the Chief Actuary

Office of the Superintendent of Financial Institutions

Canada

12th Floor, Kent Square Building

255 Albert Street

Ottawa, Ontario

K1A 0H2

E-mail: oca-bac@osfi-bsif.gc.ca

Web site: www.osfi-bsif.gc.ca

© His Majesty the King in Right of Canada, 2022

Cat. No. IN3-16/27E-PDF

ISSN 2564-1026

7 September 2022

Jonathan Wallace

Director General, Canada Student Financial Assistance Program

Employment and Social Development Canada

200 Montcalm Street

Montcalm Building, Tower 2 - 1st Floor

Gatineau, QC

K1A 0J9

Dear Jonathan Wallace:

As per the business plan for 2022-2023 to 2024-2025, I am pleased to submit the Actuarial Report on the Canada Student Financial Assistance Program, prepared as at 31 July 2021. This report is prepared for the CSFA Program to support internal accounting requirements as well as your partners’ needs between statutory reports.

Yours sincerely,

Assia Billig, FCIA, FSA, PhD

Chief Actuary

Office of the Chief Actuary

Table of contents

List of Tables

- Table 1 Demographic and Labour Force Assumptions

- Table 2 Real Wage and Tuition Increases Assumptions

- Table 3 Borrowing Cost (percentage)

- Table 4 Population and Post-secondary Enrolment of Participating Provinces

- Table 5 Loan Recipients

- Table 6 Student Need

- Table 7 Increase in New Loans Issued

- Table 8 Guaranteed and Risk-Shared Regimes Portfolio (in $ million)

- Table 9 Direct Loan Portfolio and Allowances (in $ million)

- Table 10 Defaulted Loans and Allowance for Bad Debt - Principal (in $ million)

- Table 11 Interest on Defaulted Loans and Allowance for Bad Debt - Interest (in $ million)

- Table 12 Allowance for Repayment Assistance Plan - Principal (in $ million)

- Table 13 Direct Loan Portfolio and Allowances (in millions of 2021 constant dollars)

- Table 14 Aggregate Amount of Outstanding Student Loans (in $ million)

- Table 15 Student Related Expenses (in $ million)

- Table 16 Risks to the Government (in $ million)

- Table 17 Summary of Expenses (in $ million)

- Table 18 Total Revenues (in $ million)

- Table 19 Net Annual Cost of the Program ($ million)

- Table 20 Net Annual Cost of the Program (in millions of 2021 constant dollars)

- Table 21 Direct Loans Issued and Number of Students

- Table 22 Direct Loans Consolidated (in $ million)

- Table 23 Direct Loans Default Portfolio - Principal (in $ million)

- Table 24a Repayment Assistance Plan - Principal Payments ($ million)

- Table 24b Repayment Assistance Plan - Interest Payments ($ million)

- Table 25a Full-time Post-Secondary Enrolment Rate by Labour Force Status - In Labour Force (Represents 47% of total enrolment 15-29 in 2020-2021)

- Table 25b Full-time Post-Secondary Enrolment Rate by Labour Force Status - Not In Labour Force (Represents 53% of total enrolment 15-29 in 2020-2021)

- Table 25c Full-time Post-Secondary Enrolment Rate by Labour Force Status - Total Enrolment Over Population 15-29

- Table 26 Short-term Increase of Tuition Expenses (%)

- Table 27 Provision Rates for Bad Debt – Interest

- Table 28 RAP-Stage 1 Utilization Rates

- Table 29 RAP-Stage 2 Utilization Rates

- Table 30 RAP-PD Utilization Rates

- Table 31 Administrative Expense ($ million)

- Table 32 Alternative Interest Scenario - Assumptions (%)

- Table 33 Alternative Interest Scenario - Impact on Total Net Cost of the Program ($ million)

List of Charts

1 Purpose and Summary

Main Findings

Grants

- $3,188M disbursed in 2020-2021

- $3,230M expected in 2021-2022

New Loans Issued

- $3,969M disbursed in 2020-2021

- $2,929M expected in 2021-2022

Direct Loan Portfolio

- $23B as at 31 July 2021

- $39B expected by 2045-2046

- $34B limit projected to be reached in 2035-2036

Program's Net Cost

- $4.9B in 2020-2021

- $4.8B expected in 2045-2046

- Grants represent 66% of net cost in 2020-2021

Defaults (Bad Debt)

- Long-term net default rate is 8.1%

- $3,001M in allowance for bad debt – principal as at 31 July 2021

- $224M in allowance for bad debt – interest as at 31 July 2021

RAP (Repayment Assistance Plan)

- $2,125M in allowance for RAP – principal as at 31 July 2021

Effective 1 August 2000, the Government redesigned the delivery of the Canada Student Financial Assistance Program (CSFA Program) from one delivered by chartered banks to one directly financed by the Government. As part of this redesign, the Office of the Chief Actuary was given the mandate to conduct an actuarial review of the program.

Section 19.1 of the Canada Student Financial Assistance Act defines the mandate given to the Chief Actuary; it states that the Chief Actuary of the Office of the Superintendent of Financial Institutions shall prepare a report on the financial assistance provided under this Act no later than three years apart. Such an actuarial report was prepared as at 31 July 2020 and tabled before Parliament on 7 December 2021. The next triennial statutory report will be prepared as at 31 July 2023 and is scheduled to be tabled before Parliament in 2024.

This actuarial report, prepared as at 31 July 2021, is provided to support Employment and Social Development Canada’s accounting requirements and its partners, the Office of the Auditor General, the Treasury Board Secretariat and the Department of Finance. The report includes a forecast of the Program’s costs and revenues for 25 years (through the 2045-2046 loan year), and shows estimates of:

- the number of students receiving a loan under the CSFA Program and the amount of new loans issued;

- the portfolio of loans in-study, loans in repayment and loans in default;

- the allowances under the direct loan regime in effect since August 2000; and

- the revenues, the expenses and the net resulting cost by type of regime.

COVID-19 Pandemic

More than two years have passed since the beginning of the COVID-19 pandemic. The situation remains fluid and will likely continue to evolve for some time. While employment is returning to a pre-pandemic level, there are still uncertainties regarding the future state of Canada’s economy. For instance, current inflation is higher than historically seen in the last 30 years. Additionally, the temporary measures that were introduced by the Government within the CSFA Program to alleviate the impact of the pandemic on students and borrowers are set to expire at the end of the loan year 2022-2023. The final impacts of this health and economic crisis will likely generate some differences in the future.

This valuation report is based on the program provisions as described in Appendix A. The additional appendices provide information on the data used, a description of assumptions and methodologies used, the net cost to the program under an alternative interest scenario and information on concessionary terms.

Subsequent events occurred after the valuation date. The first subsequent event consists of upcoming permanent changes to the program proposed in Budget 2021 and Budget 2022, as described in Section 2.1. In order to provide projections based on up-to-date information, these changes were considered in our report. However, the allowances determined for Public Accounts as at 31 March 2022 were based on the existing program’s provisions as of that date. Budget 2021 changes are awaiting government approval, and Budget 2022 changes were announced after the Public Accounts valuation date of 31 March 2022 and have expected implementation dates that are later than 31 March 2022.

The second subsequent event consists of the recent evolution of inflation in Canada. Since the purpose of our report is to present results based on the conditions as at 31 July 2021, it is not considered in this report. For information purposes only, allowances determined for the Public Accounts as at 31 March 2022 would not be significantly impacted by a higher than expected inflation over a short-term period.

2 Main Report

The Canada Student Financial Assistance Program (CSFA Program) has been in effect since 1964; it provides Canadians with financial assistance to pursue a post-secondary education. The Office of the Chief Actuary has the mandate to provide an assessment of the current costs of the CSFA Program, a long-term (25 years) forecast of these costs, and a portfolio projection. The results are presented on a loan year basis from 1 August to 31 July.

The following items are considered to determine the net cost of the program:

Expenses

- Canada Student Grants (CSG)

- Interest subsidy on in-study loans and loans in the 6-month non-repayment period

- Interest relief from the Repayment Assistance Plan (RAP)

- Provisions for RAP (principal) and bad debt (principal and interest)

- Alternative payments

- Loan forgiveness expenses

- Administrative expenses

Reduced by Net Interest Revenues

- Interest accrued during the six-month non-repayment period (up to 31 October 2019)

- Student interest payments

- RAP interest payments covered by the Government

- Interest accrued on defaulted loans

2.1 Recent Program Changes

Over the last few years, several changes were made to the CSFA Program. This section summarizes recent changes that were implemented in loan year ending 31 July 2021 or will be implemented in future years. Unless stated otherwise, these measures have been reflected in the projections presented in this report.

| Implementation Date | Description | Source |

|---|---|---|

| 1 August 2020 | Remove the restriction which prevent borrowers who have been out of study for five years and have used the RAP for Students with Permanent Disabilities (RAP-PD) to receive further loans and grants until their outstanding loans are fully paid. | Budget 2019 / Approved |

| 1 October 2020 | Implement interest-free and payment-free leave, for a maximum of 18 months, for borrowers taking temporary leave from their studies for medical or parental reasons, including mental health leave. | Budget 2019 / Approved |

| 1 August 2021 | Flexibility to use current year’s income instead of previous year’s income to determine eligibility for Canada Student Grants (three-year pilot project introduced in 2018-2019 made permanent). | Budget 2021 / Approved |

| 1 August 2022 | Expand access to supports for students and borrowers with persistent or prolonged disabilities that are not necessarily permanent. | Budget 2021 / Approved |

| 1 November 2022 | Increase accessibility to the RAP by increasing RAP income thresholds and reducing the maximum affordable payment. | Budget 2021 / Approved |

| 2023-2024 (expected) |

Increase by 50% the maximum amount of loans that can be forgiven for doctors and nurses working in underserved rural or remote communities. | Budget 2022 / Pending Regulatory Approval |

| To be determined | Expand the list of professionals eligible for loan forgiveness while working in under-served rural or remote communities, and review the definition of “rural communities”. | Budget 2022 / Not considered in this report as details are not finalized |

| Start/End Date | Description | Source |

|---|---|---|

| 30 March 2020 to 30 September 2020 |

Suspend student loan repayments and interest accrual. |

Measures in response to COVID 19 |

| 1 August 2020 to 31 July 2021 |

Double the amount for the following CSGs:

Change the need assessment so that no fixed student contribution or spousal contribution are considered. This helps students qualify for more financial support. Increase the weekly loan limit, from $210 to $350. |

Measures in response to COVID 19 |

| 1 April 2021 to 31 March 2022 |

Waiver of interest accrual on student loans. |

Bill C-14 / Approved |

| 1 August 2021 to31 July 2023 |

Extend the doubling of the grants. Extend the top-up grant of $200 per month for eligible adult learners returning to school full-time after being out of secondary school for at least 10 years (extension of the three-year pilot project introduced in loan year 2018-2019). |

Budget 2021 / Approved |

| 1 April 2022 to 31 March 2023 |

Extend the waiver of interest accrual on student loans. |

Budget 2021 / Approved |

2.2 Best-Estimate Assumptions

Several economic and demographic assumptions are needed to determine the future long-term costs of the CSFA Program. The projections included in this report cover a period of 25 years and the assumptions are determined by considering both historical trends and short-term experience. These assumptions reflect the actuary’s best judgment and are referred to as “best-estimate” assumptions.

2.2.1 Assumptions related to Total Loans Issued Projections

Several assumptions are needed to determine the total amount of loans issued. Tables 1 and 2 summarize the main assumptions used. Other economic assumptions used can be found in Table 3.

Table 1 presents the demographic and labour force assumptions while Table 2 presents the real wages and tuition fee increases assumptions. Assumptions shown in Table 1 and the ultimate real wage increase shown in Table 2 are based on the 30th Actuarial Report on the Canada Pension Plan as at 31 December 2018.

| 1 | Total fertility rate for Canada (ultimate) | 1.62 per woman (for 2027+) |

|---|---|---|

| 2 | Mortality | Statistics Canada Life Tables with CPP 30th assumed future improvements |

| 3 | Net migration rate for Canada (ultimate) | 0.62% of population (for 2021+) |

| 4 | Yearly Youth labour force participation rate (participating provinces/territory, ages 15-29)Table 1 Footnote * | 71.1%Table 1 Footnote ** (2021-2022) |

| 70.7% (2022-2023) | ||

| 70.8% (2023-2024) | ||

| ... | ||

| 72.6% (2045-2046) | ||

Table 1 Footnotes

|

||

| 5 | Real wage increasesTable 2 Footnote * | 0.7% (2021-2022) |

|---|---|---|

| 0.8% (2022-2023) | ||

| 0.9% (2023-2024) | ||

| 1.0% (2024-2025) | ||

| 1.0% (2025-2026) | ||

| 1.0% (2026-2027)+ | ||

| 6 | Tuition fee increases | 1.9% (2021-2022) |

| 2.4% (2022-2023) | ||

| 4.2%Table 2 Footnote ** (2023-2024) | ||

| 4.2% (2024-2025) | ||

| 4.2% (2025-2026) | ||

| 4.3% (2026-2027) | ||

| 4.4% (2027-2028) | ||

| Inflation + 1.75% (2028-2029)+ | ||

Table 2 Footnotes

|

||

2.2.2 Cost of Borrowing

Table 3 presents the interest rates and inflation assumptions used to calculate the cost of borrowing for the Government and for borrowers. The inflation assumption is also used in the projection of total loans issued.

| Loan Year | Government's Cost of Borrowing (1) |

Inflation (2) |

Government's Real Cost of BorrowingTable 3 Footnote * (1) − (2) |

Prime Rate (3) |

Student's Cost of Borrowing (4) |

|---|---|---|---|---|---|

| 2021-2022 | 2.1 | 4.6 | -2.6 | 2.8 | 2.8 |

| 2022-2023 | 2.8 | 3.0 | -0.2 | 3.4 | 3.4 |

| 2023-2024 | 2.9 | 2.3 | 0.6 | 3.5 | 3.5 |

| 2024-2025 | 2.9 | 2.1 | 0.8 | 3.5 | 3.5 |

| 2025-2026 | 3.0 | 2.0 | 1.0 | 3.6 | 3.6 |

| 2026-2027 | 3.0 | 2.0 | 1.0 | 3.6 | 3.6 |

| 2027-2028 | 3.1 | 2.0 | 1.1 | 3.7 | 3.7 |

| 2028-2029 | 3.2 | 2.0 | 1.2 | 3.8 | 3.8 |

| 2029-2030 | 3.3 | 2.0 | 1.3 | 3.9 | 3.9 |

| 2030-2031 | 3.4 | 2.0 | 1.4 | 4.0 | 4.0 |

| 2031-2032 | 3.5 | 2.0 | 1.5 | 4.1 | 4.1 |

| 2032-2033 | 3.6 | 2.0 | 1.6 | 4.2 | 4.2 |

| 2033-2034+ | 3.7 | 2.0 | 1.7 | 4.3 | 4.3 |

Table 3 Footnotes

|

|||||

The average prime rate for the 2021-2022 loan year is 2.8%. It is obtained by adding the government’s cost of borrowing and an interest rate spread. The government’s cost of borrowing is expected to increase to reach an ultimate rate of 3.7% in 2033-2034. The assumption on the interest rate spread is developed based on the analysis of historical data and the expected short-term trajectory of interest rates. The spread is expected to decrease from 0.7% in 2021-2022 to an ultimate value of 0.6% in 2022-2023, resulting in an ultimate prime rate of 4.3% in 2033-2034.

2.2.3 Assumptions related to Allowances

Since August 2000, the CSFA Program has been delivered and financed directly by the Government. Three allowances exist to cover future costs: Bad debt – principal, Bad debt – interest and Repayment Assistance Plan (RAP) – principal.

A summary of the assumptions used to determine the allowances is provided below. Additional details can be found in Appendix C.

Long-Term Defaulted Principal Assumptions

Several assumptions are used to determine the expected future amount of defaulted principal that will not be recovered. These assumptions are revised each year. The gross default assumption was increased to reflect recent experience as well as uncertainty regarding the impact of the projected increase in interest rates in the short-term. However, recalls and rehabilitations have been higher than expected, resulting in an ultimate net default rate that is the same as the one in the previous actuarial report. The following ultimate assumptions are used:

Gross Default

- 15.25% of future consolidations

- Increased from 15.0% in the previous report

Recalls and Rehabilitations

- 14.0% of future long-term gross default rate

- Increased from 13.5% in the previous report

Recoveries

- 32.8% of future long-term gross default rate

- Same as the previous report

Resulting Net Default

- 8.1% [15.25% x (1 - 14.0% - 32.8%)

- Same as the previous report

Interest Recovery Assumption

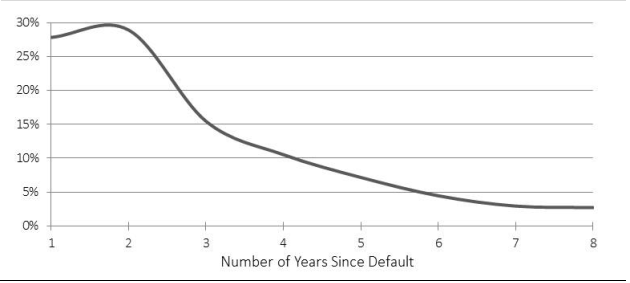

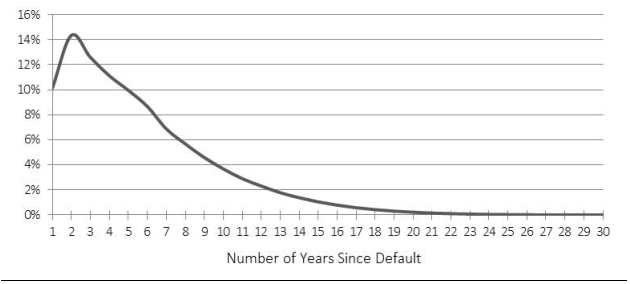

The interest recovery assumption is used to project the future expected non-recoverable interest. It is determined by a distribution that varies according to the time elapsed since the interest defaulted. The recovery rates are based on historical observations. Overall, the recovery rate for future accrued default interest is 55.8%.

Repayment Assistance Plan (RAP) Assumptions

Several assumptions are used to determine the dollar amount of loans that will ultimately be repaid by the Government through the RAP rather than by borrowers. These assumptions are reviewed each year based on new experience available:

RAP-Stage 2 and RAP-PD Utilization

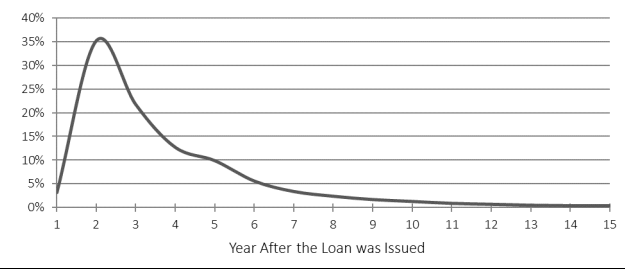

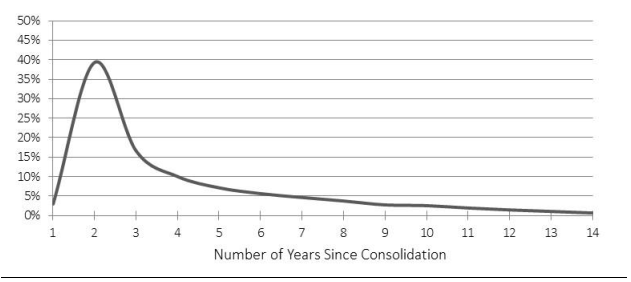

- Share of loans in RAP according to the number of years since consolidation as well as the number of years spent in RAP (Tables 29 and 30 of Appendix C).

Required Payments

- Total payments for borrowers in RAP, i.e., portion covered by the affordable payments paid by the borrowers and portion covered by the Government.

- Based on:

- Interest Rate

- Number of years remaining in the amortization period as determined under the plan’s provision

- Outstanding balance of the loan

Affordable Payments

- Average portion of the total required payments to be paid by borrowers (the remaining portion is covered by the Government):

- For RAP-Stage 2, it corresponds to 4% of total required payments

- For RAP-PD, it corresponds to 1% of total required payments

These assumptions include the expected program changes in the RAP as well as the expected change to the disability definition, both announced in Budget 2021. The impact, for RAP changes, was revised from the previous report resulting in lower expected affordable payments.

2.3 Projection of Total Loans Issued

The following formula illustrates a simplification of the elements considered in the projection of the total amount of loans issued under the CSFA Program:

Total Amount of Loans Issued = Population × Post-Secondary Enrolment Rates × Loan Uptake Rates × Average Loan Size

2.3.1 Projection of the Population

Demographic projections are based on the population projected in the 30th Actuarial Report on the Canada Pension Plan as at 31 December 2018. Subsets of the population ineligible to participate in the CSFA Program are then removed, such that the “population” used corresponds to Canada less Quebec, Northwest Territories, Nunavut and non-permanent residents.

As shown in Table 4, the population aged 15-29 is expected to decrease from 4,958,000 in 2020-2021 to 4,949,000 in 2021-2022. After that, it is expected to increase for the remainder of the projection period to reach 5,906,000 in 2045-2046. Over the 25-year projection period, the population aged 15-29 is expected to increase by 948,000.

2.3.2 Projection of Post-Secondary Enrolment

Projections of post-secondary enrolment are based on enrolment data from Statistics Canada’s Labour Force Survey up to January 2022.

The enrolment rates vary according to the following:

Overall, the aggregate enrolment rate for students aged 15 to 29 is expected to remain between 22% and 24% over the next 25 years.

Table 4 shows the evolution of the number of students enrolled full-time in a post-secondary institution (age group 15-29 and total). The total number of enrolled students is expected to increase from its current level of 1,278,000 to 1,532,000 at the end of the projection period. Students aged 15-29 are used for illustrative purposes as they represent more than 85% of the total post-secondary enrolment and better demonstrate the movement of this population across time.

| Loan Year | Population of Canada Less Quebec, Nunavut, and NWT (15-29)Table 4 Footnote ** (thousands) |

Students Enrolled Full-Time (15-29)Table 4 Footnote *** (thousands) |

All Students Enrolled Full-Time (Total)Table 4 Footnote *** (thousands) |

Increase (thousands) |

Increase (%) |

|---|---|---|---|---|---|

| 2020-2021 | 4,958 | 1,124 | 1,278 | N/A | N/A |

| 2021-2022 | 4,949 | 1,147 | 1,311 | 33 | 2.5 |

| 2022-2023 | 4,957 | 1,153 | 1,313 | 2 | 0.2 |

| 2023-2024 | 4,978 | 1,153 | 1,312 | -1 | -0.1 |

| 2024-2025 | 5,001 | 1,154 | 1,312 | 0 | 0.0 |

| 2025-2026 | 5,023 | 1,159 | 1,318 | 6 | 0.5 |

| 2026-2027 | 5,045 | 1,169 | 1,329 | 11 | 0.8 |

| 2027-2028 | 5,080 | 1,179 | 1,338 | 9 | 0.7 |

| 2028-2029 | 5,116 | 1,189 | 1,347 | 9 | 0.7 |

| 2029-2030 | 5,148 | 1,197 | 1,355 | 8 | 0.6 |

| 2030-2031 | 5,177 | 1,206 | 1,363 | 8 | 0.6 |

| 2031-2032 | 5,216 | 1,213 | 1,371 | 8 | 0.6 |

| 2032-2033 | 5,260 | 1,219 | 1,377 | 6 | 0.4 |

| 2033-2034 | 5,305 | 1,223 | 1,380 | 3 | 0.3 |

| 2034-2035 | 5,347 | 1,226 | 1,384 | 4 | 0.3 |

| 2035-2036 | 5,397 | 1,232 | 1,390 | 6 | 0.4 |

| 2036-2037 | 5,448 | 1,242 | 1,401 | 11 | 0.8 |

| 2037-2038 | 5,495 | 1,252 | 1,412 | 11 | 0.8 |

| 2038-2039 | 5,537 | 1,262 | 1,424 | 12 | 0.8 |

| 2039-2040 | 5,582 | 1,274 | 1,437 | 13 | 0.9 |

| 2040-2041 | 5,631 | 1,288 | 1,452 | 15 | 1.0 |

| 2041-2042 | 5,687 | 1,303 | 1,468 | 16 | 1.1 |

| 2042-2043 | 5,742 | 1,318 | 1,485 | 17 | 1.2 |

| 2043-2044 | 5,797 | 1,333 | 1,502 | 17 | 1.1 |

| 2044-2045 | 5,852 | 1,348 | 1,518 | 16 | 1.1 |

| 2045-2046 | 5,906 | 1,361 | 1,532 | 14 | 0.9 |

Table 4 Footnotes

|

|||||

2.3.3 Projection of the Number of Students Receiving a Loan

The projection of the loan uptake rates is based on the historical number of students receiving a loan under the CSFA Program according to:

Educational Institution

- University

- Public college

- Private college

The product of the number of students enrolled full-time and the CSFA Program loan uptake rate gives the number of students receiving a loan under the CSFA Program. Table 5 shows that the increasing loan uptake rate, from 45.1% in 2020-2021 to 52.2% in 2045-2046, combined with the increase in students enrolled in post-secondary education, results in 223,000 more students in the program (from 576,000 students in 2020-2021 to 799,000 in 2045-2046).

The number of students in the CSFA Program shown in Table 5 does not include students who only receive a CSG since their entire need is covered by the grant (no loans are issued to them). According to the ESDC data file, the total number of students who received a grant in the 2020-2021 loan year is 542,000. Most grant recipients (82%Footnote 1) received both a loan and a grant.

| Loan Year | Students Enrolled Full-Time (thousands) (1) |

Loan Uptake Rate (%) (2) |

Students in CSFATable 5 Footnote * (thousands) (1) × (2) |

Annual Increase in CSFA Students (thousands) |

Annual Increase in CSFA Students (%) |

|---|---|---|---|---|---|

| 2020-2021 | 1,278 | 45.1 | 576 | N/A | N/A |

| 2021-2022 | 1,311 | 42.3 | 554 | -23 | -3.9 |

| 2022-2023 | 1,313 | 42.0 | 552 | -2 | -0.3 |

| 2023-2024 | 1,312 | 48.5 | 637 | 84 | 15.3 |

| 2024-2025 | 1,312 | 49.1 | 644 | 7 | 1.1 |

| 2025-2026 | 1,318 | 49.3 | 650 | 6 | 1.0 |

| 2026-2027 | 1,329 | 49.4 | 656 | 6 | 0.9 |

| 2027-2028 | 1,338 | 49.5 | 662 | 6 | 0.9 |

| 2028-2029 | 1,347 | 49.6 | 669 | 6 | 0.9 |

| 2029-2030 | 1,355 | 49.8 | 674 | 5 | 0.8 |

| 2030-2031 | 1,363 | 49.9 | 680 | 6 | 0.9 |

| 2031-2032 | 1,371 | 50.0 | 686 | 6 | 0.8 |

| 2032-2033 | 1,377 | 50.2 | 690 | 5 | 0.7 |

| 2033-2034 | 1,380 | 50.3 | 694 | 4 | 0.6 |

| 2034-2035 | 1,384 | 50.4 | 698 | 4 | 0.6 |

| 2035-2036 | 1,390 | 50.6 | 703 | 5 | 0.7 |

| 2036-2037 | 1,401 | 50.7 | 710 | 7 | 1.1 |

| 2037-2038 | 1,412 | 50.8 | 718 | 7 | 1.1 |

| 2038-2039 | 1,424 | 51.0 | 726 | 8 | 1.1 |

| 2039-2040 | 1,437 | 51.1 | 735 | 9 | 1.2 |

| 2040-2041 | 1,452 | 51.2 | 744 | 10 | 1.3 |

| 2041-2042 | 1,468 | 51.4 | 754 | 10 | 1.4 |

| 2042-2043 | 1,485 | 51.5 | 765 | 11 | 1.4 |

| 2043-2044 | 1,502 | 51.6 | 775 | 10 | 1.4 |

| 2044-2045 | 1,518 | 51.8 | 786 | 10 | 1.3 |

| 2045-2046 | 1,532 | 52.2 | 799 | 13 | 1.7 |

Table 5 Footnotes

|

|||||

2.3.4 Projection of the Average Loan Issued per Borrower

The projection of the average loan issued is based on the projection of the student net need, capped at the maximum weekly loan limit:

Step 1: Determining the student net need

Student NeedFootnote 2 (excess of expenses over resources):

- Expenses: tuition and compulsory fees, books and supplies, living allowance, return transportation, child care and a few other allowable expenses depending on the student’s situation.

- Resources: student contributionsFootnote 3 and, when applicable, parental or spousal contributions.

- Projected to increase using economic assumptions.

Grants reduction:

- Grants are the first component that reduce the student need, resulting in the student net need.

- Grants may fulfill the entire student need, in which case no loan is issued.

- Different grants are available (details can be found in Appendix A).

- Grants other than those for disability are projected using inflation indexed thresholds and expected gross annual family income.

Table 6 summarizes the main elements of the student net need calculation. All students who receive a loan are included.

| Loan Year | Resources (A) |

Tuition (B) |

Other Expenses (C) |

Total Expenses (D) = (B) + (C) |

Average Student Need (E) = (D) − (A) |

Average Grant for Net Need CalculationTable 6 Footnote 2 (F) |

CSFA Average Student Net Need (G) = (E) × 60% − (F) |

CSFA Average Student Net Need Increase |

|---|---|---|---|---|---|---|---|---|

| 2020-2021 | 1,600Table 6 Footnote 3 | 8,300 | 13,100 | 21,400 | 19,800 | 4,500 | 7,400 | N/A |

| 2021-2022 | 3,400 | 8,500 | 13,700 | 22,200 | 18,800 | 4,400 | 6,900 | -500 |

| 2022-2023 | 3,500 | 8,700 | 14,100 | 22,800 | 19,300 | 4,600Table 6 Footnote 4 | 7,000 | 100 |

| 2023-2024 | 3,600 | 9,000 | 14,500 | 23,500 | 19,900 | 2,200Table 6 Footnote 5 | 9,700 | 2,700 |

| 2024-2025 | 3,700 | 9,400 | 14,800 | 24,200 | 20,500 | 2,200 | 10,100 | 400 |

| 2025-2026 | 3,800 | 9,800 | 15,100 | 24,900 | 21,100 | 2,200 | 10,500 | 400 |

| 2026-2027 | 3,900 | 10,200 | 15,400 | 25,600 | 21,700 | 2,200 | 10,800 | 300 |

| 2027-2028 | 4,000 | 10,600 | 15,700 | 26,300 | 22,300 | 2,200 | 11,200 | 400 |

| 2028-2029 | 4,100 | 11,100 | 16,000 | 27,100 | 23,000 | 2,200 | 11,600 | 400 |

| 2029-2030 | 4,200 | 11,500 | 16,300 | 27,800 | 23,600 | 2,100 | 12,100 | 500 |

| 2030-2031 | 4,300 | 11,900 | 16,600 | 28,500 | 24,200 | 2,100 | 12,400 | 300 |

| 2031-2032 | 4,400 | 12,400 | 17,000 | 29,400 | 25,000 | 2,100 | 12,900 | 500 |

| 2032-2033 | 4,600 | 12,800 | 17,300 | 30,100 | 25,500 | 2,100 | 13,200 | 300 |

| 2033-2034 | 4,700 | 13,300 | 17,700 | 31,000 | 26,300 | 2,100 | 13,700 | 500 |

| 2034-2035 | 4,800 | 13,800 | 18,000 | 31,800 | 27,000 | 2,100 | 14,100 | 400 |

| 2035-2036 | 5,000 | 14,400 | 18,400 | 32,800 | 27,800 | 2,000 | 14,700 | 600 |

| 2036-2037 | 5,100 | 14,900 | 18,700 | 33,600 | 28,500 | 2,000 | 15,100 | 400 |

| 2037-2038 | 5,300 | 15,500 | 19,100 | 34,600 | 29,300 | 2,000 | 15,600 | 500 |

| 2038-2039 | 5,500 | 16,100 | 19,500 | 35,600 | 30,100 | 2,000 | 16,100 | 500 |

| 2039-2040 | 5,600 | 16,700 | 19,900 | 36,600 | 31,000 | 2,000 | 16,600 | 500 |

| 2040-2041 | 5,800 | 17,300 | 20,300 | 37,600 | 31,800 | 2,000 | 17,100 | 500 |

| 2041-2042 | 6,000 | 18,000 | 20,700 | 38,700 | 32,700 | 2,000 | 17,600 | 500 |

| 2042-2043 | 6,200 | 18,700 | 21,100 | 39,800 | 33,600 | 1,900 | 18,300 | 700 |

| 2043-2044 | 6,400 | 19,400 | 21,500 | 40,900 | 34,500 | 1,900 | 18,800 | 500 |

| 2044-2045 | 6,600 | 20,200 | 22,000 | 42,200 | 35,600 | 1,900 | 19,500 | 700 |

| 2045-2046 | 6,800 | 20,900 | 22,400 | 43,300 | 36,500 | 1,900 | 20,000 | 500 |

Table 6 Footnotes

|

||||||||

Step 2: Adjusting for the loan limit

Loans are capped at a maximum of $210 per weekFootnote 4:

- Projected to remain fixed at $210

The constant loan limit restricts the growth of new loans issued. Over time, more students reach the loan limit without their needs being completely fulfilled. This is shown in Table 7, where the percentage of students at the loan limit is projected to increase from 58.1% in 2023-2024 to 92.6% in 2045-2046.

2.3.5 Total Amount of Loans Issued

Table 7 presents the resulting projection of new amount of loans issued.

| Loan Year | Average Student Need ($) (1) |

Increase (%) |

% of Students at LimitTable 7 Footnote 1 (2) |

New Loans Issued ($ million) (3) |

Increase (%) |

Students in CSFA (thousands) (4) |

Increase (%) |

Average Loan Size ($) (3) / (4) |

Increase (%) |

|---|---|---|---|---|---|---|---|---|---|

| 2020-2021 | 19,800 | N/A | 17.7 | 3,969 | N/A | 576 | N/A | 6,885 | N/A |

| 2021-2022 | 18,800 | -5.1Table 7 Footnote 2 | 41.4Table 7 Footnote 3Table 7 Footnote 4 | 2,929 | -26.2Table 7 Footnote 5 | 554 | -3.9 | 5,288 | -23.2 |

| 2022-2023 | 19,300 | 2.7 | 42.5Table 7 Footnote 4 | 2,872 | -1.9 | 552 | -0.3 | 5,202 | -1.6 |

| 2023-2024 | 19,900 | 3.1 | 58.1 | 3,847 | 33.9Table 7 Footnote 6 | 637 | 15.3 | 6,043 | 16.2 |

| 2024-2025 | 20,500 | 3.0 | 59.9 | 3,927 | 2.1 | 644 | 1.1 | 6,100 | 0.9 |

| 2025-2026 | 21,100 | 2.9 | 61.9 | 4,008 | 2.1 | 650 | 1.0 | 6,164 | 1.1 |

| 2026-2027 | 21,700 | 2.8 | 64.2 | 4,101 | 2.3 | 656 | 0.9 | 6,247 | 1.3 |

| 2027-2028 | 22,300 | 2.8 | 66.3 | 4,189 | 2.2 | 662 | 0.9 | 6,324 | 1.2 |

| 2028-2029 | 23,000 | 3.1 | 68.2 | 4,274 | 2.0 | 669 | 0.9 | 6,391 | 1.1 |

| 2029-2030 | 23,600 | 2.6 | 70.4 | 4,352 | 1.8 | 674 | 0.8 | 6,455 | 1.0 |

| 2030-2031 | 24,200 | 2.5 | 72.5 | 4,429 | 1.8 | 680 | 0.9 | 6,514 | 0.9 |

| 2031-2032 | 25,000 | 3.3 | 75.0 | 4,502 | 1.6 | 686 | 0.8 | 6,567 | 0.8 |

| 2032-2033 | 25,500 | 2.0 | 77.2 | 4,566 | 1.4 | 690 | 0.7 | 6,615 | 0.7 |

| 2033-2034 | 26,300 | 3.1 | 79.1 | 4,622 | 1.2 | 694 | 0.6 | 6,657 | 0.6 |

| 2034-2035 | 27,000 | 2.7 | 80.7 | 4,674 | 1.1 | 698 | 0.6 | 6,695 | 0.6 |

| 2035-2036 | 27,800 | 3.0 | 82.2 | 4,731 | 1.2 | 703 | 0.7 | 6,730 | 0.5 |

| 2036-2037 | 28,500 | 2.5 | 83.5 | 4,803 | 1.5 | 710 | 1.1 | 6,762 | 0.5 |

| 2037-2038 | 29,300 | 2.8 | 84.7 | 4,875 | 1.5 | 718 | 1.1 | 6,791 | 0.4 |

| 2038-2039 | 30,100 | 2.7 | 85.8 | 4,948 | 1.5 | 726 | 1.1 | 6,817 | 0.4 |

| 2039-2040 | 31,000 | 3.0 | 86.9 | 5,025 | 1.6 | 735 | 1.2 | 6,841 | 0.4 |

| 2040-2041 | 31,800 | 2.6 | 88.0 | 5,107 | 1.6 | 744 | 1.3 | 6,863 | 0.3 |

| 2041-2042 | 32,700 | 2.8 | 89.1 | 5,192 | 1.7 | 754 | 1.4 | 6,882 | 0.3 |

| 2042-2043 | 33,600 | 2.8 | 90.1 | 5,278 | 1.7 | 765 | 1.4 | 6,900 | 0.2 |

| 2043-2044 | 34,500 | 2.7 | 91.2 | 5,362 | 1.6 | 775 | 1.4 | 6,914 | 0.2 |

| 2044-2045 | 35,600 | 3.2 | 92.0 | 5,443 | 1.5 | 786 | 1.3 | 6,926 | 0.2 |

| 2045-2046 | 36,500 | 2.5 | 92.6 | 5,600 | 2.9 | 799 | 1.7 | 7,006 | 1.1 |

Table 7 Footnotes

|

|||||||||

Table 7 shows the annual increase in new loans issued over the 25-year projection period. Overall, the total new loans issued is expected to decrease from $3,969 million in 2020-2021 to $2,929 million in 2021-2022 due to the weekly loan limit decreasing from $350 in 2020-2021 to $210 in 2021-2022. In 2045-2046, projected new loans issued total $5,600 million, which corresponds to an average annual increase of 1.4%Footnote 5. This average annual increase can be attributed to two factors: an average annual increase in the number of students in the program of 1.3% and an average annual increase in the average loan size of 0.1% over the 25-year projection period. The average loan size is calculated as the ratio of new loans issued over the number of students receiving a loan under the CSFA Program. The growth rate of the average loan size is moderated due to the constant loan limit.

2.4 Portfolio Projections

This section presents projections of the portfolio for all three regimes described in Appendix A, as well as projections of the three allowances under the direct loan regime. The amounts for loans in-study represent loans issued to students who are still in the post-secondary educational system. Interest on loans in-study is fully subsidized by the Government for students in the CSFA Program. Loans in repayment consist of outstanding loans consolidated by students with financial institutions (or the Government).

2.4.1 Guaranteed and Risk-Shared Regimes

The guaranteed and risk-shared regimes apply to loans issued before August 2000. Some loans in these regimes are still outstanding since there are still students under these regimes attending post-secondary institutions or repaying their loans. Table 8 presents the projections of the guaranteed and risk-shared loans owned by financial institutions and by the GovernmentFootnote 6 as well as the loans returned to the Government because of default (principal only). The projection for defaulted loans is shown separately for guaranteed and risk-shared regimes as the latter is necessary to determine when the limit on the aggregate amount of outstanding loans prescribed through the Canada Student Financial Assistance Regulations will be reached, as presented in Table 14. The guaranteed and risk-shared regimes are gradually being phased out.

| As at July 31 |

Loans in Study or Repayment (with financial institutions)Table 8 Footnote * - Guaranteed and Risk‑Shared |

Loans in Study or Repayment (bought back by the Government) - Guaranteed and Risk‑Shared |

Loans in Default (Returned to the Government) - Guaranteed |

Loans in Default (Returned to the Government) - Risk‑Shared |

Total |

|---|---|---|---|---|---|

| 2021 | 732 | 10 | 44 | 30 | 815 |

| 2022 | 708 | 9 | 37 | 27 | 781 |

| 2023 | 668 | 8 | 29 | 24 | 728 |

| 2024 | 596 | 7 | 19 | 21 | 643 |

| 2025 | 502 | 6 | 9 | 19 | 536 |

| 2026 | 398 | 5 | 0 | 17 | 420 |

| 2027 | 296 | 3 | -nil | 15 | 314 |

| 2028 | 205 | 2 | -nil | 12 | 219 |

| 2029 | 132 | 2 | -nil | 9 | 142 |

| 2030 | 85 | -nil | -nil | 4 | 90 |

| 2031 | 54 | -nil | -nil | 1 | 56 |

| 2032 | 27 | -nil | -nil | 0 | 27 |

| 2033 | 0 | -nil | -nil | 0 | 0 |

| 2034 | 0 | -nil | -nil | -nil | 0 |

| 2035 | -nil | -nil | -nil | -nil | -nil |

| 2036 | -nil | -nil | -nil | -nil | -nil |

Table 8 Footnotes

|

|||||

At the end of the 2020-2021 loan year, the sum of all loans coming from the guaranteed and risk-shared regimes that are owned by the Government amounts to approximately $151 million (principal and interest). The Government sets up a separate allowance in the Public Accounts for those loans. This allowance calculation is not included in this report. Expenses related to Guaranteed and Risk-Shared Loans are presented in Table 15 and Table 16.

2.4.2 Direct Loan Regime

The projection of the direct loan portfolio includes the balance of outstanding loans (in-study and in repayment separately) and the balance of loans in default. There are two allowances for bad debt (principal and interest) to cover the risk of future default, net of recoveries, and an allowance for the RAP (principal) to cover the future cost of students benefiting from this program. The projection of the direct loan portfolio and allowances is shown in Table 9.

| As at July 31 |

Principal only - Loans In‑Study |

Principal only - Loans in Repayment |

Principal only - Defaulted Loans |

Principal only - Total |

Allowance for Bad Debt Principal |

Allowance for Bad Debt Interest |

Allowance for RAP - Principal |

|---|---|---|---|---|---|---|---|

| 2021 | 8,964 | 11,784 | 2,288Table 9 Footnote * | 23,036 | 3,001 | 224 | 2,125Table 9 Footnote ** |

| 2022 | 8,110 | 12,206 | 2,444 | 22,760 | 3,018Table 9 Footnote **** | 195Table 9 Footnote **** | 2,323Table 9 Footnote ***Table 9 Footnote **** |

| 2023 | 8,100 | 11,784 | 2,566 | 22,450 | 3,074 | 171 | 2,334 |

| 2024 | 9,039 | 11,683 | 2,626 | 23,348 | 3,175 | 172 | 2,413 |

| 2025 | 9,699 | 11,925 | 2,672 | 24,296 | 3,278 | 179 | 2,486 |

| 2026 | 10,215 | 12,294 | 2,727 | 25,236 | 3,387 | 191 | 2,555 |

| 2027 | 10,649 | 12,707 | 2,798 | 26,154 | 3,503 | 205 | 2,621 |

| 2028 | 11,011 | 13,162 | 2,858 | 27,031 | 3,600 | 217 | 2,687 |

| 2029 | 11,331 | 13,631 | 2,907 | 27,869 | 3,680 | 227 | 2,758 |

| 2030 | 11,620 | 14,104 | 2,972 | 28,696 | 3,770 | 239 | 2,832 |

| 2031 | 11,887 | 14,572 | 3,049 | 29,508 | 3,868 | 253 | 2,910 |

| 2032 | 12,133 | 15,030 | 3,131 | 30,294 | 3,967 | 267 | 2,988 |

| 2033 | 12,359 | 15,467 | 3,213 | 31,039 | 4,064 | 281 | 3,063 |

| 2034 | 12,562 | 15,884 | 3,294 | 31,740 | 4,157 | 294 | 3,134 |

| 2035 | 12,746 | 16,270 | 3,375 | 32,391 | 4,247 | 307 | 3,206 |

| 2036 | 12,924 | 16,628 | 3,454 | 33,006 | 4,334 | 318 | 3,275 |

| 2037 | 13,109 | 16,963 | 3,531 | 33,603 | 4,419 | 328 | 3,342 |

| 2038 | 13,297 | 17,287 | 3,608 | 34,192 | 4,504 | 336 | 3,406 |

| 2039 | 13,491 | 17,592 | 3,684 | 34,767 | 4,589 | 344 | 3,466 |

| 2040 | 13,692 | 17,885 | 3,759 | 35,336 | 4,673 | 351 | 3,524 |

| 2041 | 13,903 | 18,172 | 3,834 | 35,909 | 4,759 | 359 | 3,581 |

| 2042 | 14,123 | 18,459 | 3,908 | 36,490 | 4,845 | 367 | 3,639 |

| 2043 | 14,350 | 18,749 | 3,982 | 37,081 | 4,932 | 375 | 3,696 |

| 2044 | 14,579 | 19,044 | 4,055 | 37,678 | 5,019 | 381 | 3,754 |

| 2045 | 14,807 | 19,344 | 4,128 | 38,279 | 5,106 | 388 | 3,813 |

| 2046 | 15,108 | 19,649 | 4,203 | 38,960 | 5,199 | 396 | 3,877 |

Table 9 Footnotes

|

|||||||

The outstanding direct loans portfolio is projected to increase rapidly from $23 billion as at 31 July 2021 to $25.2 billion five years later. By the end of the 2045-2046 loan year, the portfolio is projected to reach $39 billion.

As at 31 July 2021, the outstanding direct loan portfolio is $23 billion and is retrospectively derived from the experienceFootnote 7 during loan years 2000-2001 to 2020-2021 as followsFootnote 8:

| New loans issued | $50.4 billion |

|---|---|

| Plus the interest accrued during the non-repayment periodTable 9.5 Footnote * | $1.4 billion |

| Minus repaymentsTable 9.5 Footnote ** | $26.2 billion |

| Minus loans forgiven and debt reductions in repaymentTable 9.5 Footnote *** | $1.0 billion |

| Minus defaulted loans written off | $1.4 billion |

| blank | $23.0 billion |

Table 9.5 Footnotes

|

|

The remainder of subsection 2.4.2 provides detailed information on the three allowances.

Allowance for Bad Debt – Principal

Table 10 provides the calculation details for the projection of the defaulted loans portfolio and the allowance for bad debt – principal under the direct loan regime.

| Loan Year | Defaulted Loans Portfolio (Principal only) - Balance 1 August (1) |

Defaulted Loans Portfolio (Principal only) - New Defaulted LoansTable 10 Footnote * (2) |

Defaulted Loans Portfolio (Principal only) - Collected Loans (3) |

Defaulted Loans Portfolio (Principal only) - Write‑offs (4) |

Defaulted Loans Portfolio (Principal only) - Balance 31 July (1 + 2) − (3 + 4) |

Allowance for Bad Debt - Principal - Allowance 1 August (1) |

Allowance for Bad Debt - Principal - Write‑offs (2) |

Allowance for Bad Debt - Principal - Allowance 31 July (3) |

Allowance for Bad Debt - Principal - Yearly Expense (3) − (1 − 2) |

|---|---|---|---|---|---|---|---|---|---|

| 2020-2021 | 2,213 | 277Table 10 Footnote ** | 56 | 146 | 2,288 | 2,810 | 146 | 3,001 | 337 |

| 2021-2022 | 2,288 | 418 Table 10 Footnote *** | 128 | 134 | 2,444 | 3,001 | 134 | 3,018 | 151 |

| 2022-2023 | 2,444 | 380 | 122 | 137 | 2,565 | 3,018 | 137 | 3,074 | 193 |

| 2023-2024 | 2,566 | 342 | 125 | 157 | 2,626 | 3,074 | 157 | 3,175 | 258 |

| 2024-2025 | 2,626 | 331 | 126 | 160 | 2,671 | 3,175 | 160 | 3,278 | 263 |

| 2025-2026 | 2,672 | 341 | 127 | 159 | 2,727 | 3,278 | 159 | 3,387 | 268 |

| 2026-2027 | 2,727 | 358 | 129 | 158 | 2,798 | 3,387 | 158 | 3,503 | 274 |

| 2027-2028 | 2,798 | 373 | 131 | 183 | 2,857 | 3,503 | 183 | 3,600 | 280 |

| 2028-2029 | 2,858 | 388 | 133 | 206 | 2,907 | 3,600 | 206 | 3,680 | 286 |

| 2029-2030 | 2,907 | 402 | 136 | 202 | 2,971 | 3,680 | 202 | 3,770 | 292 |

| 2030-2031 | 2,972 | 415 | 140 | 198 | 3,049 | 3,770 | 198 | 3,868 | 296 |

| 2031-2032 | 3,049 | 427 | 143 | 202 | 3,131 | 3,868 | 202 | 3,967 | 301 |

| 2032-2033 | 3,131 | 438 | 147 | 209 | 3,213 | 3,967 | 209 | 4,064 | 306 |

| 2033-2034 | 3,213 | 448 | 151 | 216 | 3,294 | 4,064 | 216 | 4,157 | 309 |

| 2034-2035 | 3,294 | 458 | 155 | 222 | 3,375 | 4,157 | 222 | 4,247 | 312 |

| 2035-2036 | 3,375 | 467 | 159 | 229 | 3,454 | 4,247 | 229 | 4,334 | 316 |

| 2036-2037 | 3,454 | 476 | 162 | 236 | 3,532 | 4,334 | 236 | 4,419 | 321 |

| 2037-2038 | 3,531 | 484 | 166 | 241 | 3,608 | 4,419 | 241 | 4,504 | 326 |

| 2038-2039 | 3,608 | 492 | 170 | 246 | 3,684 | 4,504 | 246 | 4,589 | 331 |

| 2039-2040 | 3,684 | 500 | 174 | 251 | 3,759 | 4,589 | 251 | 4,673 | 335 |

| 2040-2041 | 3,759 | 508 | 177 | 256 | 3,834 | 4,673 | 256 | 4,759 | 342 |

| 2041-2042 | 3,834 | 516 | 180 | 261 | 3,909 | 4,759 | 261 | 4,845 | 347 |

| 2042-2043 | 3,908 | 524 | 184 | 266 | 3,982 | 4,845 | 266 | 4,932 | 353 |

| 2043-2044 | 3,982 | 532 | 187 | 272 | 4,055 | 4,932 | 272 | 5,019 | 359 |

| 2044-2045 | 4,055 | 540 | 190 | 277 | 4,128 | 5,019 | 277 | 5,106 | 364 |

| 2045-2046 | 4,128 | 549 | 193 | 280 | 4,204 | 5,106 | 280 | 5,199 | 373 |

Table 10 Footnotes

|

|||||||||

The balance of loans in default (principal only) was $2,288 million as at 31 July 2021. The defaulted loans portfolio is projected to reach $4,204 million by the end of the projection period.

As shown in Table 10, an amount of $146 million was written off in 2020-2021. The amount of write-offs in 2021-2022 is $134 million and includes all the non-recoverable loans that were identified and approved for write-off by ESDC and CRA between July 2020 and June 2021. These write-offs were approved on 31 March 2022, via Royal Assent of Bill C-15 (Appropriation Act No. 5, 2021-2022). The decision to write off particular loans is part of a multi-step process inevitably resulting in some volatility in the actual amount written off from year to year.

The allowance for bad debt – principal covers the risk of future defaults, net of recoveries. It is estimated at $3,001 million as at 31 July 2021, which is higher than the $2,984 million projected in the previous report as at 31 July 2020. Projections of the previous report were adjusted to reflect the newest experience available. For the 2020-2021 loan year, the yearly expense for the allowance for bad debt – principal is $337 million.

The provision rates used to determine the 2021-2022 allowance are presented below. The ultimate provision rates are presented in Appendix C.

Provision Rates

Allowance as at 31 July 2022

- 6.7% of the outstanding balance of loans in-study;

- 4.8% of the outstanding balance of loans in repayment; and

- 77.0% of the outstanding balance of loans in default.

Allowance for Public Accounts: Provision rates used to determine the allowances for Public Accounts were based on the program’s conditions as of 31 March 2022, i.e., without considering the indirect impacts from the changes proposed in Budget 2021 to the RAP nor the new disability definition.

- 6.8% of the outstanding balance of loans in-study, which is $8,748 million as at 31 March 2022;

- 4.9% of the outstanding balance of loans in repayment, which is $12,483 million as at 31 March 2022; and

- 76.9% of the outstanding balance of loans in default, which is $2,381 million as at 31 March 2022.

- Total allowance as at 31 March 2022: $3,037 million.

Allowance for Bad Debt – Interest

In accordance with the collection practice, interest accrues on defaulted loans until they reach a “non-recoverable” status. A provision is set to cover the risk that such accrued interest will never be recovered. The methodology used is the same as in the previous report. Provision rates are modified to take into account recent experience. The allowance for bad debt – interest is determined using the outstanding interest and a variable provision rate for each year since default. The provision rates are presented in Appendix C (Table 27).

The projection of the balance of interest on defaulted loans is presented in Table 11.

| Loan Year | Interest on Defaulted Loans - Balance August 1 (1) |

Interest on Defaulted Loans - Interest Transferred in DefaultTable 11 Footnote * (2) |

Interest on Defaulted Loans - Interest Accrued (3) |

Interest on Defaulted Loans - Interest Collected (4) |

Interest on Defaulted Loans - Write‑offs (5) |

Interest on Defaulted Loans - Balance July 31 (1 + 2 + 3) − (4 + 5) |

Allowance for Bad Debt - Interest - Allowance August 1 (1) |

Allowance for Bad Debt - Interest - Write‑offs (2) |

Allowance for Bad Debt - Interest - Allowance July 31 (3) |

Allowance for Bad Debt - Interest - Yearly Expense (3) − (1 − 2) |

|---|---|---|---|---|---|---|---|---|---|---|

| 2020-2021 | 358 | 7 | 30Table 11 Footnote **Table 11 Footnote *** | 19 | 39 | 337 | 238 | 39 | 224 | 26 |

| 2021-2022 | 337 | 2 | 5Table 11 Footnote *** | 37 | 35 | 271 | 224 | 35 | 195 | 6 |

| 2022-2023 | 271 | 1 | 21Table 11 Footnote *** | 35 | 34 | 224 | 195 | 34 | 171 | 10 |

| 2023-2024 | 224 | 9 | 69 | 39 | 31 | 233 | 171 | 31 | 172 | 33 |

| 2024-2025 | 233 | 10 | 81 | 44 | 29 | 250 | 172 | 29 | 179 | 36 |

| 2025-2026 | 250 | 10 | 85 | 48 | 28 | 269 | 179 | 28 | 191 | 39 |

| 2026-2027 | 269 | 11 | 87 | 51 | 27 | 289 | 191 | 27 | 205 | 41 |

| 2027-2028 | 289 | 12 | 91 | 53 | 31 | 307 | 205 | 31 | 217 | 43 |

| 2028-2029 | 307 | 12 | 95 | 56 | 35 | 323 | 217 | 35 | 227 | 46 |

| 2029-2030 | 323 | 13 | 100 | 59 | 36 | 340 | 227 | 36 | 239 | 48 |

| 2030-2031 | 340 | 14 | 106 | 62 | 37 | 361 | 239 | 37 | 253 | 51 |

| 2031-2032 | 361 | 15 | 111 | 65 | 40 | 381 | 253 | 40 | 267 | 54 |

| 2032-2033 | 381 | 15 | 117 | 69 | 43 | 402 | 267 | 43 | 281 | 57 |

| 2033-2034 | 402 | 16 | 123 | 73 | 47 | 422 | 281 | 47 | 294 | 60 |

| 2034-2035 | 422 | 16 | 127 | 76 | 48 | 440 | 294 | 48 | 307 | 61 |

| 2035-2036 | 440 | 17 | 130 | 79 | 51 | 457 | 307 | 51 | 318 | 63 |

| 2036-2037 | 457 | 17 | 133 | 81 | 55 | 470 | 318 | 55 | 328 | 64 |

| 2037-2038 | 470 | 17 | 135 | 84 | 57 | 482 | 328 | 57 | 336 | 65 |

| 2038-2039 | 482 | 18 | 138 | 86 | 58 | 494 | 336 | 58 | 344 | 66 |

| 2039-2040 | 494 | 18 | 141 | 88 | 61 | 504 | 344 | 61 | 351 | 67 |

| 2040-2041 | 504 | 18 | 143 | 90 | 61 | 515 | 351 | 61 | 359 | 69 |

| 2041-2042 | 515 | 18 | 146 | 92 | 61 | 526 | 359 | 61 | 367 | 70 |

| 2042-2043 | 526 | 19 | 149 | 94 | 63 | 537 | 367 | 63 | 375 | 71 |

| 2043-2044 | 537 | 19 | 151 | 95 | 66 | 546 | 375 | 66 | 381 | 72 |

| 2044-2045 | 546 | 19 | 154 | 97 | 67 | 555 | 381 | 67 | 388 | 73 |

| 2045-2046 | 555 | 20 | 157 | 99 | 66 | 567 | 388 | 66 | 396 | 75 |

Table 11 Footnotes

|

||||||||||

When a loan is transferred to the Government after nine months without a payment, it comes with an interest portion that generally represents slightly more than nine months of interest accrued on the defaulted principal transferred. Table 11 shows that $7 million of interest was returned to the Government in the 2020-2021 loan year, along with the newly defaulted principal portion of the loans. An additional amount of $30 million in interest was accrued during the 2020-2021 loan year on the principal balance of the recoverable defaulted loans portfolio at the beginning of the loan year.

Once loans are in default, CRA collects money for their repayment on behalf of the program. These collections are first applied to the interest portion of defaulted loans. To help individuals with a loan in default deal with COVID-19, CRA temporarily stopped collecting money. As such, an amount of $19 million was recovered in the 2020-2021 loan year, which is lower than the previous years.

Finally, when a loan meets certain criteria and has exceeded the six-year limitation period, the interest amounts are also considered for write-off. In the 2020-2021 loan year, $39 million in interest was written off. As shown in Table 11, the balance of interest in default was $358 million at the beginning of the 2020-2021 loan year and it decreased to $337 million as at 31 July 2021. The balance of interest in default is projected to increase to $567 million by the end of the projection period.

The allowance for bad debt – interest is estimated at $224 million as at 31 July 2021, which is higher than the $216 million projected in the previous report as at 31 July 2020. Projections of the previous report were adjusted to reflect the newest experience available. For the 2020-2021 loan year, the yearly expense for the allowance for bad debt – interest is $26 million.

The allowances are determined using provision rates applied to their corresponding outstanding balances of accrued interest according to the year since default. The sets of provision rates for the 2021-2022 allowances, as well as the ultimate provision rates, are presented in Appendix C. The provision rates used to determine the allowances for Public Accounts were based on the conditions of the program as of 31 March 2022, i.e., without considering the indirect impacts from the changes proposed in Budget 2021 to the RAP nor the new disability definition. The resulting allowance for Public Accounts as at 31 March 2022 corresponds to $209 million.

Allowance for the Repayment Assistance Plan – Principal

Table 12 provides the calculation details for the projection of the allowance for the Repayment Assistance Plan (RAP) under the direct loan regime.

| Loan Year | Allowance 1 August (1) |

RAP Expenses (2) |

Allowance 31 July (3) |

Yearly Expense (3) − (1 − 2) |

|---|---|---|---|---|

| 2020-2021 | 1,717 | 147Table 12 Footnote * | 2,125Table 12 Footnote ** | 555 |

| 2021-2022 | 2,125 | 164 | 2,323 | 362 |

| 2022-2023 | 2,323 | 197 | 2,334 | 208 |

| 2023-2024 | 2,334 | 199 | 2,413 | 278 |

| 2024-2025 | 2,413 | 209 | 2,486 | 282 |

| 2025-2026 | 2,486 | 219 | 2,555 | 288 |

| 2026-2027 | 2,555 | 228 | 2,621 | 294 |

| 2027-2028 | 2,621 | 234 | 2,687 | 300 |

| 2028-2029 | 2,687 | 236 | 2,758 | 307 |

| 2029-2030 | 2,758 | 238 | 2,832 | 312 |

| 2030-2031 | 2,832 | 239 | 2,910 | 317 |

| 2031-2032 | 2,910 | 245 | 2,988 | 323 |

| 2032-2033 | 2,988 | 252 | 3,063 | 327 |

| 2033-2034 | 3,063 | 258 | 3,134 | 329 |

| 2034-2035 | 3,134 | 265 | 3,206 | 337 |

| 2035-2036 | 3,206 | 270 | 3,275 | 339 |

| 2036-2037 | 3,275 | 276 | 3,342 | 343 |

| 2037-2038 | 3,342 | 285 | 3,406 | 349 |

| 2038-2039 | 3,406 | 294 | 3,466 | 354 |

| 2039-2040 | 3,466 | 302 | 3,524 | 360 |

| 2040-2041 | 3,524 | 309 | 3,581 | 366 |

| 2041-2042 | 3,581 | 315 | 3,639 | 373 |

| 2042-2043 | 3,639 | 321 | 3,696 | 378 |

| 2043-2044 | 3,696 | 326 | 3,754 | 384 |

| 2044-2045 | 3,754 | 332 | 3,813 | 391 |

| 2045-2046 | 3,813 | 337 | 3,877 | 401 |

Table 12 Footnotes

|

||||

Table 12 shows the projection of the allowance for the principal portion of the required payment paid by the Government under Stage 2, including the RAP for borrowers with permanent disabilities (RAP-PD). For the RAP – interest, a provision is determined by ESDC for accounting purposes to take into account the timing of the interest accrued.

As shown in Table 12, the allowance for the RAP – principal is estimated at $2,125 million as at 31 July 2021, which is lower than the $2,237 million projected in the previous report as at 31 July 2020. The projections of the last report were adjusted to reflect the newest experience available. For the 2020-2021 loan year, the yearly expense for the allowance for RAP – principal allowance is $555 million.

Budget 2021 proposed to modify the definition of disability to access RAP-PD (from permanent to persistent or prolonged), increase the RAP thresholds as well as to decrease the maximum affordable payment, all starting in loan year 2022-2023. Assumptions were adjusted to reflect these modifications, which result in more borrowers being eligible for RAP, a higher share of RAP-PD users, in addition to a higher share of principal payments to be covered by the Government. The changes to the RAP thresholds and decrease in the maximum affordable payment is reflected starting with the allowance for the loan year 2020-2021Footnote 9 allowance while the change in disability definition is reflected starting with the loan year 2021-2022 allowanceFootnote 10, as seen in Table 12.

The provision rates used to determine the 2021-2022 allowance are presented below. The ultimate provision rates are presented in Appendix C.

Provision Rates

Allowance as at 31 July 2022

- 7.2% of the outstanding balance of loans in-study;

- 1.8% of the outstanding balance of loans in repayment (net of loans in the RAP); and

- 45.3%Footnote 11 of the outstanding balance of loans in RAP (all stages combined).

Allowance for Public Accounts: Provision rates used to determine the allowances for Public Accounts were based on the program’s conditions as of 31 March 2022, i.e., without considering the changes proposed in Budget 2021 to the RAP nor the new disability definition.

- 5.2% of the outstanding balance of loans in-study, which is $8,748 million as at 31 March 2022;

- 1.2% of the outstanding balance of loans in repayment (reduced by loans in the RAP - all stages), which is $9,141 million as at 31 March 2022;

- 36.0% of the outstanding balance of loans in the RAP (all stages), which is $3,342 million as at 31 March 2022.

- Total allowance as at 31 March 2022: $1,768 million.

For comparison purposes, Table 13 shows the direct loan portfolio and allowances in 2021 constant dollars.

| As at July 31 |

Principal only - Loans In‑study |

Principal only - Loans in Repayment |

Principal only - Defaulted Loans |

Principal only - Total |

Allowance for Bad Debt Principal |

Allowance for Bad Debt Interest |

Allowance for RAP - Principal |

|---|---|---|---|---|---|---|---|

| 2021 | 8,964 | 11,784 | 2,288 | 23,036 | 3,001 | 224 | 2,125 |

| 2022 | 7,750 | 11,665 | 2,336 | 21,750 | 2,884 | 186 | 2,220 |

| 2023 | 7,524 | 10,946 | 2,383 | 20,853 | 2,855 | 159 | 2,168 |

| 2024 | 8,222 | 10,627 | 2,389 | 21,237 | 2,888 | 156 | 2,195 |

| 2025 | 8,653 | 10,639 | 2,384 | 21,677 | 2,925 | 160 | 2,218 |

| 2026 | 8,951 | 10,772 | 2,389 | 22,113 | 2,968 | 167 | 2,239 |

| 2027 | 9,170 | 10,943 | 2,409 | 22,522 | 3,017 | 177 | 2,257 |

| 2028 | 9,322 | 11,142 | 2,419 | 22,883 | 3,048 | 184 | 2,275 |

| 2029 | 9,433 | 11,347 | 2,420 | 23,200 | 3,063 | 189 | 2,296 |

| 2030 | 9,515 | 11,549 | 2,434 | 23,497 | 3,087 | 196 | 2,319 |

| 2031 | 9,577 | 11,740 | 2,456 | 23,773 | 3,116 | 204 | 2,344 |

| 2032 | 9,620 | 11,917 | 2,482 | 24,019 | 3,145 | 212 | 2,369 |

| 2033 | 9,646 | 12,072 | 2,508 | 24,226 | 3,172 | 219 | 2,391 |

| 2034 | 9,654 | 12,207 | 2,531 | 24,392 | 3,195 | 226 | 2,408 |

| 2035 | 9,647 | 12,314 | 2,554 | 24,516 | 3,214 | 232 | 2,427 |

| 2036 | 9,636 | 12,397 | 2,575 | 24,608 | 3,231 | 237 | 2,442 |

| 2037 | 9,630 | 12,461 | 2,594 | 24,686 | 3,246 | 241 | 2,455 |

| 2038 | 9,627 | 12,516 | 2,612 | 24,754 | 3,261 | 243 | 2,466 |

| 2039 | 9,628 | 12,555 | 2,629 | 24,812 | 3,275 | 245 | 2,474 |

| 2040 | 9,634 | 12,584 | 2,645 | 24,863 | 3,288 | 247 | 2,480 |

| 2041 | 9,647 | 12,609 | 2,660 | 24,915 | 3,302 | 249 | 2,485 |

| 2042 | 9,665 | 12,632 | 2,674 | 24,972 | 3,316 | 251 | 2,490 |

| 2043 | 9,688 | 12,658 | 2,688 | 25,034 | 3,330 | 253 | 2,495 |

| 2044 | 9,711 | 12,685 | 2,701 | 25,098 | 3,343 | 254 | 2,501 |

| 2045 | 9,733 | 12,716 | 2,714 | 25,163 | 3,356 | 255 | 2,507 |

| 2046 | 9,802 | 12,749 | 2,727 | 25,278 | 3,373 | 257 | 2,516 |

Table 13 Footnotes

|

|||||||

2.4.3 Limit on the Aggregate Amount of Outstanding Loans

The Canada Student Financial Assistance Regulations (CSFAR) imposes a limit on the aggregate amount of outstanding loans in the program. The limit was increased from $24 billion to $34 billion in June 2019.

Table 14 presents the projection of the aggregate amount of outstanding loans. It is the sum of:

- Total principal amount of direct loans in study, in repayment and in default;

- Total principal amount of defaulted risk-shared loans returnedFootnote 12 to the Government from financial institutions.

In comparison with Table 8 and Table 9, which show the projection of the loan portfolio at the end of loan years, Table 14 presents the estimated peak of the portfolio during the loan year. Monthly fluctuations throughout the year cause the aggregate amount of loans to be lower both at the beginning and at the end of the loan year. The peak usually occurs in the middle of the loan year (January) and is 3% to 5% higher than the aggregate amount at the end of the loan year. Table 9 shows an aggregate amount of outstanding direct loans of $23 billion as at 31 July 2021. Table 14 shows that the aggregate amount of outstanding direct loans reached $23.8 billion in January 2021 (loan year 2020-2021) and $24 billion in OctoberFootnote 13 2021 (loan year 2021-2022).

The projection shows that the $34 billion limit is expected to be reached during the 2035-2036 loan year if the program’s provisions don’t change and assumptions materialize. The limit is reached three years later than estimated in the 2020 Actuarial Report and it is mostly due to higher expected prepayments and lower projected loans issued.

| Loan Year | Estimated Peak During the Loan Year (January) - Direct Loans |

Estimated Peak During the Loan Year (January) - Risk-Shared Loans |

Total |

|---|---|---|---|

| 2020-2021 | 23,830 | 31 | 23,861 |

| 2021-2022 | 24,040 | 28 | 24,068 |

| 2022-2023 | 23,756 | 25 | 23,781 |

| 2023-2024 | 24,363 | 22 | 24,385 |

| 2024-2025 | 25,281 | 20 | 25,301 |

| 2025-2026 | 26,243 | 18 | 26,261 |

| 2026-2027 | 27,208 | 16 | 27,224 |

| 2027-2028 | 28,153 | 13 | 28,166 |

| 2028-2029 | 29,056 | 10 | 29,066 |

| 2029-2030 | 29,916 | 6 | 29,922 |

| 2030-2031 | 30,762 | 3 | 30,765 |

| 2031-2032 | 31,590 | 0 | 31,590 |

| 2032-2033 | 32,383 | 0 | 32,383 |

| 2033-2034 | 33,130 | -nil | 33,130 |

| 2034-2035 | 33,829 | -nil | 33,829 |

| 2035-2036 | 34,486 | -nil | 34,486 |

| 2036-2037 | 35,121 | -nil | 35,121 |

| 2037-2038 | 35,742 | -nil | 35,742 |

| 2038-2039 | 36,352 | -nil | 36,352 |

| 2039-2040 | 36,954 | -nil | 36,954 |

| 2040-2041 | 37,557 | -nil | 37,557 |

| 2041-2042 | 38,166 | -nil | 38,166 |

| 2042-2043 | 38,785 | -nil | 38,785 |

| 2043-2044 | 39,411 | -nil | 39,411 |

| 2044-2045 | 40,041 | -nil | 40,041 |

| 2045-2046 | 40,739 | -nil | 40,739 |

2.5 Projection of the Net Cost of the Program

2.5.1 Student Related Expenses

The primary expense of the CSFA Program is the cost of supporting students during their study and repayment periods. The student related expenses are presented in Table 15.

| Loan Year | Direct Loan - Interest Subsidy |

Direct Loan - RAP - InterestTable 15 Footnote 1 |

Direct Loan - Provision RAP - Principal |

Risk-Shared and Guaranteed Loans - Interest SubsidyTable 15 Footnote 2 |

Risk-Shared and Guaranteed Loans - RAP - Interest and Principal |

Canada Student Grants | Total |

|---|---|---|---|---|---|---|---|

| 2020-2021 | 95.7Table 15 Footnote 3 | 50.4Table 15 Footnote 4 | 555.7 | 0.0 | 4.6 | 3,187.5Table 15 Footnote 5 | 3,893.9 |

| 2021-2022 | 187.0 | 0.0Table 15 Footnote 4 | 361.6 | 0.0 | 4.9 | 3,229.9Table 15 Footnote 5 | 3,783.4 |

| 2022-2023 | 241.2 | 50.9Table 15 Footnote 4 | 208.1 | 0.0 | 4.7 | 3,385.7Table 15 Footnote 5Table 15 Footnote 6 | 3,890.6 |

| 2023-2024 | 272.5 | 166.6 | 277.5 | -nil | 4.4 | 1,667.3 | 2,388.3 |

| 2024-2025 | 294.8 | 168.0 | 282.4 | -nil | 4.0 | 1,668.3 | 2,417.5 |

| 2025-2026 | 322.4 | 177.5 | 287.9 | -nil | 3.3 | 1,678.0 | 2,469.1 |

| 2026-2027 | 336.8 | 183.1 | 294.3 | -nil | 2.6 | 1,692.7 | 2,509.5 |

| 2027-2028 | 360.5 | 194.5 | 300.5 | -nil | 2.0 | 1,705.0 | 2,562.5 |

| 2028-2029 | 383.3 | 206.6 | 306.4 | -nil | 1.4 | 1,718.0 | 2,615.7 |

| 2029-2030 | 405.6 | 219.0 | 311.9 | -nil | 0.9 | 1,728.7 | 2,666.1 |

| 2030-2031 | 427.7 | 231.5 | 317.3 | -nil | 0.6 | 1,740.1 | 2,717.2 |

| 2031-2032 | 449.6 | 244.3 | 322.5 | -nil | 0.0 | 1,750.7 | 2,767.1 |

| 2032-2033 | 471.2 | 257.1 | 327.1 | -nil | 0.0 | 1,759.9 | 2,815.3 |

| 2033-2034 | 492.4 | 269.8 | 329.7 | -nil | 0.0 | 1,766.0 | 2,857.9 |

| 2034-2035 | 499.8 | 276.1 | 336.9 | -nil | 0.0 | 1,772.5 | 2,885.3 |

| 2035-2036 | 506.9 | 281.8 | 338.1 | -nil | -nil | 1,780.8 | 2,907.6 |

| 2036-2037 | 514.1 | 287.3 | 342.9 | -nil | -nil | 1,795.6 | 2,939.9 |

| 2037-2038 | 521.5 | 292.6 | 348.8 | -nil | -nil | 1,810.1 | 2,973.0 |

| 2038-2039 | 529.1 | 297.7 | 354.4 | -nil | -nil | 1,826.3 | 3,007.5 |

| 2039-2040 | 536.9 | 302.5 | 360.0 | -nil | -nil | 1,844.9 | 3,044.3 |

| 2040-2041 | 545.2 | 307.3 | 365.9 | -nil | -nil | 1,865.1 | 3,083.5 |

| 2041-2042 | 553.7 | 312.1 | 372.0 | -nil | -nil | 1,886.4 | 3,124.2 |

| 2042-2043 | 562.6 | 317.0 | 378.2 | -nil | -nil | 1,909.0 | 3,166.8 |

| 2043-2044 | 571.6 | 321.9 | 384.2 | -nil | -nil | 1,931.1 | 3,208.8 |

| 2044-2045 | 580.6 | 326.9 | 390.0 | -nil | -nil | 1,951.8 | 3,249.3 |

| 2045-2046 | 591.8 | 332.1 | 401.1 | -nil | -nil | 1,971.7 | 3,296.7 |

Table 15 Footnotes

|

|||||||

In the 2020-2021 loan year, a total of $3,188 million of CSGs were disbursed. Those grants are projected to remain at a similar level for 2021-2022 and to increase in 2022-2023 due to the temporary doubling of grants (2020-2021 to 2022-2023) and the change in the definition of disability (2022-2023+). Monthly grant amounts are set in the Canada Student Financial Assistance Regulations and are assumed to remain constant for the remaining projection period for the purpose of this valuation.

2.5.2 Program Risk Expenses

Another expense for the Government corresponds to the risk that loans will never be repaid. This includes the risk of loan default and the risk of loans being forgiven upon a student’s death or severe permanent disability. Loans forgiven for family physicians and nurses practicing in under-served rural or remote communities are also included in Table 16 below.

| Loan Year | Direct Loan - Provision for Bad Debt - Principal |

Direct Loan - Provision for Bad Debt - Interest |

Risk-Shared - Risk Premium, Put-Backs & Refunds to FIs |

Guaranteed - Claims for Defaulted Loans |

Loans Forgiven |

Total |

|---|---|---|---|---|---|---|

| 2020-2021 | 337.2 | 25.8 | 4.0 | 0.4 | 39.0 | 406.4 |

| 2021-2022 | 150.7 | 6.4 | 0.5 | 0.0 | 38.7 | 196.3 |

| 2022-2023 | 193.5 | 9.5 | 0.4 | 0.0 | 37.0 | 240.4 |

| 2023-2024 | 257.8 | 32.6 | 0.4 | 0.0 | 44.2Table 16 Footnote * | 335.0 |

| 2024-2025 | 262.7 | 36.4 | 0.4 | 0.0 | 45.9 | 345.4 |

| 2025-2026 | 268.1 | 39.3 | 0.3 | 0.0 | 47.2 | 354.9 |

| 2026-2027 | 274.3 | 41.3 | 0.3 | -nil | 49.0 | 364.9 |

| 2027-2028 | 280.2 | 43.4 | 0.2 | -nil | 52.4 | 376.2 |

| 2028-2029 | 285.9 | 45.5 | 0.2 | -nil | 53.5 | 385.1 |

| 2029-2030 | 291.1 | 48.0 | 0.1 | -nil | 54.6 | 393.8 |

| 2030-2031 | 296.2 | 51.0 | 0.1 | -nil | 55.7 | 403.0 |

| 2031-2032 | 301.1 | 54.0 | -nil | -nil | 56.8 | 411.9 |

| 2032-2033 | 305.4 | 56.9 | -nil | -nil | 57.8 | 420.1 |

| 2033-2034 | 309.1 | 59.9 | -nil | -nil | 58.8 | 427.8 |

| 2034-2035 | 312.6 | 61.3 | -nil | -nil | 59.7 | 433.6 |

| 2035-2036 | 316.4 | 62.6 | -nil | -nil | 60.5 | 439.5 |

| 2036-2037 | 321.3 | 63.9 | -nil | -nil | 61.3 | 446.5 |

| 2037-2038 | 326.0 | 65.1 | -nil | -nil | 62.1 | 453.2 |

| 2038-2039 | 330.9 | 66.3 | -nil | -nil | 62.8 | 460.0 |

| 2039-2040 | 336.1 | 67.5 | -nil | -nil | 63.6 | 467.2 |

| 2040-2041 | 341.6 | 68.7 | -nil | -nil | 64.4 | 474.7 |

| 2041-2042 | 347.3 | 69.9 | -nil | -nil | 65.1 | 482.3 |

| 2042-2043 | 353.0 | 71.1 | -nil | -nil | 65.9 | 490.0 |

| 2043-2044 | 358.6 | 72.3 | -nil | -nil | 66.7 | 497.6 |

| 2044-2045 | 364.1 | 73.5 | -nil | -nil | 67.4 | 505.0 |

| 2045-2046 | 373.0 | 74.7 | -nil | -nil | 68.2 | 515.9 |

Table 16 Footnotes

|

||||||

Details on the risks to the Government are provided below:

| Direct Loans |

Provision for bad debts (principal and interest): Cost of the default risk assumed by the Government in directly disbursing loans to students. |

|---|---|

| Risk-Shared |

Risk premium: Amount paid to lending institutions by the Government based on the value of loans consolidating in a year. |

|

Put-backs and Refunds to financial institutions:

|

|

| Guaranteed |

Claims for defaulted loans: the Government bears the entire risk of defaulted loans. |

| Loans Forgiven |

Due to death: during the period of study, repayment or after the loan has defaulted. |

|

Due to severe permanent disability: As of August 2009, limited to borrowers who, due to their severe permanent disability, are unable to pay their loans and will never be able to repay them. |

|

|

For doctors and nurses: Portion of loans for family physicians and nurses who practice in under-served rural or remote communities. Budget 2022 proposed to increase by 50% the maximum amount of doctors and nurses forgivable loans under the loan forgiveness program starting in loan year 2023-2024. Budget 2022 also proposed to expand the current list of eligible professionals and definition or rural communities under the loans forgiveness program. |

2.5.3 Other Expenses

Alternative payments are made directly to Quebec, the Northwest Territories and Nunavut, as they do not participate in the CSFA Program. The calculation of alternative payments is based on expenses and revenues for a given loan year and the payment is accounted for in the following loan year.

The short-term projection of the administrative fees was provided by ESDC. All collection activities on defaulted loans are fulfilled by CRA and a cost is included in the projected general administrative fees for this purpose.

As shown in Table 17, and notwithstanding impacts from temporary measures, total expenses associated with the program increase from $3.6 billion in 2024-2025Footnote 14 to $5.0 billion in 2045-2046. On average, total expenses are projected to increase at an annual rate of 1.7%.

| Loan Year | Student Related Expenses | Risks to the Government | Alternative PaymentsTable 17 footnote * | Administrative Expenses - Fees Paid to Provinces |

Administrative Expenses - General |

Total Expenses |

|---|---|---|---|---|---|---|

| 2020-2021 | 3,893.9 | 406.4 | 487.2 | 35.1 | 99.3 | 4,921.9 |

| 2021-2022 | 3,783.4 | 196.3 | 927.4Table 17 footnote ** | 36.7 | 106.0 | 5,049.8 |

| 2022-2023 | 3,890.6 | 240.4 | 1,065.4Table 17 footnote ** | 38.0 | 117.1 | 5,351.5 |

| 2023-2024 | 2,388.3 | 335.0 | 1,118.4Table 17 footnote ** | 39.0 | 117.9 | 3,998.6 |

| 2024-2025 | 2,417.5 | 345.4 | 645.1 | 40.3 | 119.1 | 3,567.4 |

| 2025-2026 | 2,469.1 | 354.9 | 659.2 | 41.5 | 125.3 | 3,650.0 |

| 2026-2027 | 2,509.5 | 364.9 | 685.9 | 42.8 | 135.8 | 3,738.9 |

| 2027-2028 | 2,562.5 | 376.2 | 712.3 | 44.1 | 139.9 | 3,835.0 |

| 2028-2029 | 2,615.7 | 385.1 | 740.5 | 45.4 | 144.2 | 3,930.9 |

| 2029-2030 | 2,666.1 | 393.8 | 767.4 | 46.8 | 148.6 | 4,022.7 |

| 2030-2031 | 2,717.2 | 403.0 | 793.8 | 48.2 | 153.2 | 4,115.4 |

| 2031-2032 | 2,767.1 | 411.9 | 818.4 | 49.7 | 157.9 | 4,205.0 |

| 2032-2033 | 2,815.3 | 420.1 | 840.8 | 51.2 | 162.7 | 4,290.1 |

| 2033-2034 | 2,857.9 | 427.8 | 861.6 | 52.8 | 167.7 | 4,367.8 |

| 2034-2035 | 2,885.3 | 433.6 | 878.3 | 54.4 | 172.8 | 4,424.4 |

| 2035-2036 | 2,907.6 | 439.5 | 885.7 | 56.1 | 178.1 | 4,467.0 |

| 2036-2037 | 2,939.9 | 446.5 | 889.3 | 57.8 | 183.6 | 4,517.1 |

| 2037-2038 | 2,973.0 | 453.2 | 891.9 | 59.6 | 189.2 | 4,566.9 |

| 2038-2039 | 3,007.5 | 460.0 | 896.5 | 61.4 | 195.0 | 4,620.4 |

| 2039-2040 | 3,044.3 | 467.2 | 898.6 | 63.3 | 201.0 | 4,674.4 |

| 2040-2041 | 3,083.5 | 474.7 | 900.0 | 65.2 | 207.1 | 4,730.5 |

| 2041-2042 | 3,124.2 | 482.3 | 901.5 | 67.2 | 213.4 | 4,788.6 |

| 2042-2043 | 3,166.8 | 490.0 | 903.6 | 69.3 | 220.0 | 4,849.7 |

| 2043-2044 | 3,208.8 | 497.6 | 908.5 | 71.4 | 226.7 | 4,913.0 |

| 2044-2045 | 3,249.3 | 505.0 | 914.5 | 73.6 | 233.7 | 4,976.1 |

| 2045-2046 | 3,296.7 | 515.9 | 918.3 | 75.8 | 240.8 | 5,047.5 |

|

||||||

2.5.4 Total Revenue

Interest revenues from the direct loan regime (shown in Table 18) include:

- Interest earned from student loans in repayment;

- Interest accrued on defaulted loans; and

- Interest portion of the RAP.

These interest revenues are net of interest on loans forgiven. They are also reduced by the Government’s cost of borrowing for loans in repayment and in default (only for the interest accrued expected to be recovered). It is worth noting that the interest on defaulted direct loans is accrued until the status of the loans becomes “non-recoverable”.

Under the guaranteed and risk-shared regimes, revenues mainly come from recoveries of principal and interest from defaulted loans owned by the Government. A small portion of revenues are coming from good-standing loans in repayment that were bought back from financial institutions in loan year 2021-2022.

Total revenues, notwithstanding the temporary waiver of interest, are projected to increase at an average rate of 2.7% per year between 2023-2024Footnote 15 and 2045-2046.

| Loan Year | Direct Loan - Interest Revenues |

Direct Loan - Borrowing Cost |

Direct Loan - Net Interest Revenues |

Risk-SharedTable 18 footnote * - Principal and Interest from Recovery |

Guaranteed - Principal and Interest from Recovery |

Total Revenues |

|---|---|---|---|---|---|---|

| 2020-2021 | 199.9Table 18 footnote **Table 18 footnote *** | -147.4 | 52.5 | 1.4 | 2.2 | 56.1 |

| 2021-2022 | 5.1Table 18 footnote *** | -299.8 | -294.7 | 2.1 | 3.3 | -289.3 |

| 2022-2023 | 154.3Table 18 footnote *** | -423.4 | -269.1 | 2.2 | 2.8 | -264.1 |

| 2023-2024 | 490.5 | -367.7 | 122.8 | 2.1 | 2.1 | 127.0 |

| 2024-2025 | 506.6 | -375.0 | 131.6 | 1.9 | 1.4 | 134.9 |

| 2025-2026 | 533.2 | -397.6 | 135.6 | 1.7 | 0.0 | 137.3 |

| 2026-2027 | 548.2 | -410.4 | 137.8 | 1.5 | 0.0 | 139.3 |

| 2027-2028 | 580.7 | -438.3 | 142.4 | 1.3 | 0.0 | 143.7 |

| 2028-2029 | 615.8 | -468.1 | 147.7 | 1.1 | 0.0 | 148.8 |

| 2029-2030 | 652.7 | -499.4 | 153.3 | 0.8 | -nil | 154.1 |

| 2030-2031 | 691.3 | -531.8 | 159.5 | 0.4 | -nil | 159.9 |

| 2031-2032 | 731.0 | -565.0 | 166.0 | 0.0 | -nil | 166.0 |

| 2032-2033 | 769.4 | -598.5 | 170.9 | 0.0 | -nil | 170.9 |

| 2033-2034 | 810.5 | -632.2 | 178.3 | -nil | -nil | 178.3 |

| 2034-2035 | 832.6 | -648.2 | 184.3 | -nil | -nil | 184.3 |

| 2035-2036 | 852.9 | -663.2 | 189.7 | -nil | -nil | 189.7 |

| 2036-2037 | 871.6 | -677.1 | 194.5 | -nil | -nil | 194.5 |

| 2037-2038 | 889.9 | -690.4 | 199.5 | -nil | -nil | 199.5 |

| 2038-2039 | 907.2 | -703.1 | 204.0 | -nil | -nil | 204.0 |

| 2039-2040 | 923.5 | -715.2 | 208.2 | -nil | -nil | 208.2 |

| 2040-2041 | 939.3 | -727.1 | 212.2 | -nil | -nil | 212.2 |

| 2041-2042 | 954.8 | -738.8 | 216.1 | -nil | -nil | 216.1 |

| 2042-2043 | 970.3 | -750.5 | 219.8 | -nil | -nil | 219.8 |

| 2043-2044 | 985.8 | -762.4 | 223.4 | -nil | -nil | 223.4 |

| 2044-2045 | 1,001.5 | -774.5 | 227.0 | -nil | -nil | 227.0 |

| 2045-2046 | 1,017.5 | -786.8 | 230.6 | -nil | -nil | 230.6 |

|

||||||

2.5.5 Net Cost of the Program

Table 19 shows projected total expenses, total revenues and the total net cost of the program in current dollars for the 25-year projection period, while Table 20 shows the same information expressed in 2021 constant dollars. The expenses and revenues shown correspond to values presented earlier in this report.

| Loan Year | All Regimes - Total Expenses ($ million) |

All Regimes - Total Revenues ($ million) |

All Regimes - Total Net Cost of the Program ($ million) |

All Regimes - Changes (%) |

Net Cost of the Program - Direct Loan ($ million) |

Net Cost of the Program - Risk-Shared & Guaranteed ($ million) |

|---|---|---|---|---|---|---|

| 2020-2021 | 4,921.9 | 56.1 | 4,865.8 | N/A | 4,859.9 | 5.9 |

| 2021-2022 | 5,049.8 | -289.3 | 5,339.1 | 9.7 | 5,338.8 | 0.3 |

| 2022-2023 | 5,351.5 | -264.1 | 5,615.6 | 5.2 | 5,615.1 | 0.5 |

| 2023-2024 | 3,998.6 | 127.0 | 3,871.6 | -31.1 | 3,870.7 | 0.9 |

| 2024-2025 | 3,567.4 | 134.9 | 3,432.5 | -11.3 | 3,431.0 | 1.5 |

| 2025-2026 | 3,650.0 | 137.3 | 3,512.7 | 2.3 | 3,510.4 | 2.3 |

| 2026-2027 | 3,738.9 | 139.3 | 3,599.6 | 2.5 | 3,597.8 | 1.8 |

| 2027-2028 | 3,835.0 | 143.7 | 3,691.3 | 2.5 | 3,690.2 | 1.1 |

| 2028-2029 | 3,930.9 | 148.8 | 3,782.1 | 2.5 | 3,781.5 | 0.6 |

| 2029-2030 | 4,022.7 | 154.1 | 3,868.6 | 2.3 | 3,868.4 | 0.2 |

| 2030-2031 | 4,115.4 | 159.9 | 3,955.5 | 2.2 | 3,955.2 | 0.3 |

| 2031-2032 | 4,205.0 | 166.0 | 4,039.0 | 2.1 | 4,038.9 | 0.1 |

| 2032-2033 | 4,290.1 | 170.9 | 4,119.2 | 2.0 | 4,119.2 | 0.0 |

| 2033-2034 | 4,367.8 | 178.3 | 4,189.5 | 1.7 | 4,189.6 | 0.0 |

| 2034-2035 | 4,424.4 | 184.3 | 4,240.1 | 1.2 | 4,240.3 | 0.0 |

| 2035-2036 | 4,467.0 | 189.7 | 4,277.3 | 0.9 | 4,277.3 | 0.0 |

| 2036-2037 | 4,517.1 | 194.5 | 4,322.6 | 1.1 | 4,322.5 | -nil |

| 2037-2038 | 4,566.9 | 199.5 | 4,367.4 | 1.0 | 4,367.3 | -nil |

| 2038-2039 | 4,620.4 | 204.0 | 4,416.4 | 1.1 | 4,416.3 | -nil |

| 2039-2040 | 4,674.4 | 208.2 | 4,466.2 | 1.1 | 4,466.3 | -nil |

| 2040-2041 | 4,730.5 | 212.2 | 4,518.3 | 1.2 | 4,518.2 | -nil |

| 2041-2042 | 4,788.6 | 216.1 | 4,572.5 | 1.2 | 4,572.5 | -nil |

| 2042-2043 | 4,849.7 | 219.8 | 4,629.9 | 1.3 | 4,629.9 | -nil |

| 2043-2044 | 4,913.0 | 223.4 | 4,689.6 | 1.3 | 4,689.6 | -nil |

| 2044-2045 | 4,976.1 | 227.0 | 4,749.1 | 1.3 | 4,749.0 | -nil |

| 2045-2046 | 5,047.5 | 230.6 | 4,816.9 | 1.4 | 4,816.9 | -nil |

As shown in Table 19, the initial net annual cost for the direct loan regime is $4.9 billion for the 2020-2021 loan year. The net cost is projected to increase between loan year 2024-2025Footnote 14 and loan year 2045-2046 from $3.4 billion to $4.8 billion, representing an annual average increase of 1.6%.