InfoPensions – Issue 34 – May 2026

InfoPensions includes announcements and reminders on matters relevant to federally regulated private pension plans, including pooled registered pension plans. It is published twice a year and you can subscribe to it and other pension-related announcements by using Email notifications. We expect to publish the next issue of InfoPensions in November 2026.

If you have questions about any of the articles or if you have suggestions for future articles, please contact us at Pension-Retraite@osfi-bsif.gc.ca. You can find past articles by searching our pension guidance by topic.

For general enquiries, please contact us at information@osfi-bsif.gc.ca. If you prefer to contact us by telephone or by mail, please select "Contact OSFI" on our website.

Table of contents

Supervision

Best practices for defined contribution pension plans

We would like to remind plan administrators of certain best practices for defined contribution (DC) pension plans.

1. DC plans permitting investment choices

In order to meet their fiduciary duties, plan administrators should ensure that members and any other persons permitted to make investment choices receive adequate and appropriate information to make informed investment decisions and have access to decision-making tools. In addition, we would like to remind plan administrators of our expectation to periodically review the design, performance and continued suitability of the default investment option. Please consult our guidance on the Default Option for Member Choice DC Plans for more information.

2. DC plans not permitting investment choices

Where a DC plan does not permit investment choices, the administrator must establish a Statement of Investment Policies and Procedures (SIP&P) for the plan. Subsection 7.2(1) of the Pension Benefits Standards Regulations, 1985 (PBSR) also requires the administrator to review and confirm or amend the SIP&P at least once each plan year. The annual review allows the plan administrator to identify whether the SIP&P still meets the plan's objectives for the investments of the pension fund.

3. CAPSA guidelines

Plan administrators of DC pension plans are reminded to review the following Canadian Association of Pension Supervisory Authorities (CAPSA) guidelines, which provide useful guidance and expectations related to the administration of DC pension plans:

- CAPSA Guideline No. 3: Guideline for Capital Accumulation Plans (PDF)

- CAPSA Guideline No. 4: Pension Plan Governance Guideline (PDF)

- CAPSA Guideline No. 8: Defined Contribution Pension Plans Guideline (PDF)

- CAPSA Guideline No. 10: Guideline for Risk Management for Plan Administrators (PDF)

General observations related to annual filings

Plan administrators must file with OSFI the Certified Financial Statements and may also be required to file an auditor's report of the pension fund, in accordance with the Pension Benefit Standards Act, 1985, the Pension Benefits Standards Regulations, 1985 and the Directives of the Superintendent pursuant to the Pension Benefits Standards Act, 1985.

Please note the following observations related to these annual filings:

1. Certified Financial Statements (OSFI 60)

We have noticed that, for some plans, the Statement of changes in net assets was not completed in the OSFI 60. Plan administrators are reminded that they must complete both the Statement of changes in net assets and the Statement of net assets in Section A (defined contribution provision) and Section B (defined benefit provision), as applicable. For further details, please consult our Instruction guide for filing the Certified Financial Statements (OSFI 60).

2. Filing Confirmation (ARFC)

As noted in our Instruction guide for filing the Auditor's Report Filing Confirmation (ARFC), an auditor's report is not required to be filed with us when the filer answers "Yes" to any of questions 1-4 of the ARFC. Plan administrators may still file an auditor's report even when they are not required to do so. In cases where an auditor's report is not required and one is not being submitted, the ARFC must be submitted without uploading any other document and questions 5.a) and 5.b) must remain blank.

Plan amendment filing and disclosure requirements

Plan administrators are reminded of key amendment filing and disclosure requirements below:

1. Deadline for filing amendments

Subsection 10.1(1) of the Pension Benefit Standards Act, 1985 (PBSA) requires the plan administrator to file with the Superintendent a copy of any amendment to the plan or any supporting document within 60 days after the amendment is made.

We consider the date the amendment is made to be the date that it is adopted in accordance with the governance procedures set up for that plan, for example, by way of a board resolution.

2. Disclosure of amendments to members

Plan administrators are reminded that paragraph 28(1)(a) of the PBSA requires that a written explanation of the provisions of the plan and of any applicable amendments to the plan, be provided to each member and each employee who is eligible to join the plan, and that person's spouse or common-law partner, within 60 days of the establishment of the plan or after the making of the amendment.

We expect plan administrators to apply paragraph 28(1)(a) of the PBSA broadly and assume that most amendments to a plan could be considered applicable to all members of that plan and should therefore be disclosed to all members and eligible employees and their spouses or common-law partners. For example, while a particular amendment may not directly affect the benefit level of a particular class of members, it may have an impact on the funding of the plan.

3. Amendment forms (OSFI 593 and OSFI 594)

In February 2025, we updated the OSFI 593 and OSFI 594 forms to include additional information, specifically the date the amendment was made and the date members and eligible employees received a copy of the amendment. Plan administrators must use the most recent version of these forms when submitting a plan amendment via the Regulatory Reporting System. For further details, please consult our Instruction guide for filing Pension Plan Amendments Using the Regulatory Reporting System.

Guidance and legislative matters

Final publication of framework - unclaimed pension balances

Finalized regulations amending the Pension Benefits Standards Regulations, 1985 (PBSR) for the unclaimed pension balances regime were published in the April 8th edition of the Canada Gazette, Part II, which also includes the Order-in-Council bringing into force the related legislative amendments. The legislative amendments include amendments to sections 10.3 and 39 of the Pension Benefits Standards Act, 1985. The legislation and regulations providing for the unclaimed balances regime will come into force on January 1, 2027.

Under the unclaimed pension balances regime, terminated, federally regulated private pension plans will be able to transfer pension balances for un-locatable members to the designated entity, after obtaining approval from the Superintendent. The Governor in Council has approved the designation by the Minister of Finance of the Bank of Canada as the designated entity (Order-in-Council PC Number: 2026-0276). The designation by the Minister of Finance of the Bank of Canada as the designated entity will be formalized at a future date.

Transferring unclaimed pension balances to the Bank of Canada will allow terminated pension plans to complete the process of winding up. Plan administrators will be expected to make appropriate efforts to locate members, former members, survivors and any other persons entitled to benefits under the plan before seeking approval.

We anticipate publishing guidance this fall with more details on the approval from the Superintendent to transfer balances. In addition, we will begin accepting applications no earlier than January 1, 2027.

Once transferred to the Bank of Canada, unclaimed pension balances will be able to be claimed in a similar manner as what is available for unclaimed banking deposits from the Bank of Canada.

As described in Part II of the Canada Gazette, the amendments:

- set out the information associated with unclaimed pension balances of un-locatable members that the plan administrators must provide to the Bank of Canada, at the time of transfer.

- set out the information the Bank of Canada can publish on a public database to facilitate the search for unclaimed pension assets.

- allow the Bank of Canada to publish the last known name and address of the un-locatable members, the name and registration number of the pension plan, as well as the market value of the transferred assets.

- specify who qualifies as an eligible claimant of unclaimed pension assets and establish the period for how long the Bank of Canada can administer the unclaimed assets before the funds are transferred to the Crown.

Proposed regulatory changes to the Pension Benefit Standards Regulations, 1985 – buy-out annuities and unlocking

On April 4, 2026, the federal government published a notice in the Canada Gazette, Part I, of proposed amendments to the Pension Benefits Standards Regulations, 1985 (PBSR). These proposed amendments related to buy-out annuities and unlocking pension funds within a pension plan. Interested persons were able to make representations concerning these proposed amendments until May 4, 2026.

As described in the notice, the amendments would:

- prescribe the types of annuities that plan administrators may purchase in order to transfer pension obligations to a life insurance company and set related disclosure requirements.

- provide defined contribution plan members who choose to receive variable benefits, if offered by their plan, with the same flexibility and options to unlock pension funds in retirement as members who choose to transfer their pension benefits from defined contribution plans to a locked-in retirement savings vehicle.

- make minor technical changes to the PBSR and the Pooled Registered Pension Plans Regulations, and the Assessment of Pension Plans Regulations.

CAPSA's 2026-2029 Strategic Plan

OSFI is a member of the Canadian Association of Pension Supervisory Authorities (CAPSA), a national association of pension regulators whose mission is to facilitate an efficient and effective pension regulatory system in Canada. On April 16, 2026, CAPSA published its Strategic Plan for 2026 through 2029. CAPSA's 2026 to 2029 strategic priorities include the harmonization of regulator expectations, strengthening pension plan supervision, enhancing regulator partnerships and stakeholder engagement, and promoting public awareness of pension plans. Priority initiatives include work to support the implementation of the 2020 Agreement Respecting Multi-jurisdictional pension plans and to support the development of enhancements to the agreement. CAPSA will also consider updating, consolidating, or developing new guidelines.

Guidance posted on our website

The following documents were posted to our website since the last edition of InfoPensions:

- January 2026 – Form 1 and Instructions – Attestation regarding withdrawal based on financial hardship

- December 2025 – 2026 Maximum Annual amount of Life Income Funds, Restricted Life Income Funds, and Variable Benefits Accounts

Actuarial

Estimated solvency ratio results

We regularly estimate the solvency ratio for federally regulated private pension plans with defined benefit provisions. The estimated solvency ratio (ESR) exercise assists us in identifying solvency issues that could affect the security of pension benefits promised to members and beneficiaries before a pension plan files their actuarial report. The ESR results also help identify broader trends.

We calculate the ESR using the most recent actuarial, financial, and membership information filed with us for each plan before the analysis date. Assets are projected based on either the rate of return provided on the Solvency Information Return (SIR) or an assumed rate of return for the plan when no SIR has been filed. Solvency liabilities are projected using relevant interest rates. Expected contributions, benefit payments, and expenses are considered and an ESR based on the estimated adjusted market value of the fund and estimated liabilities is then calculated for each plan.

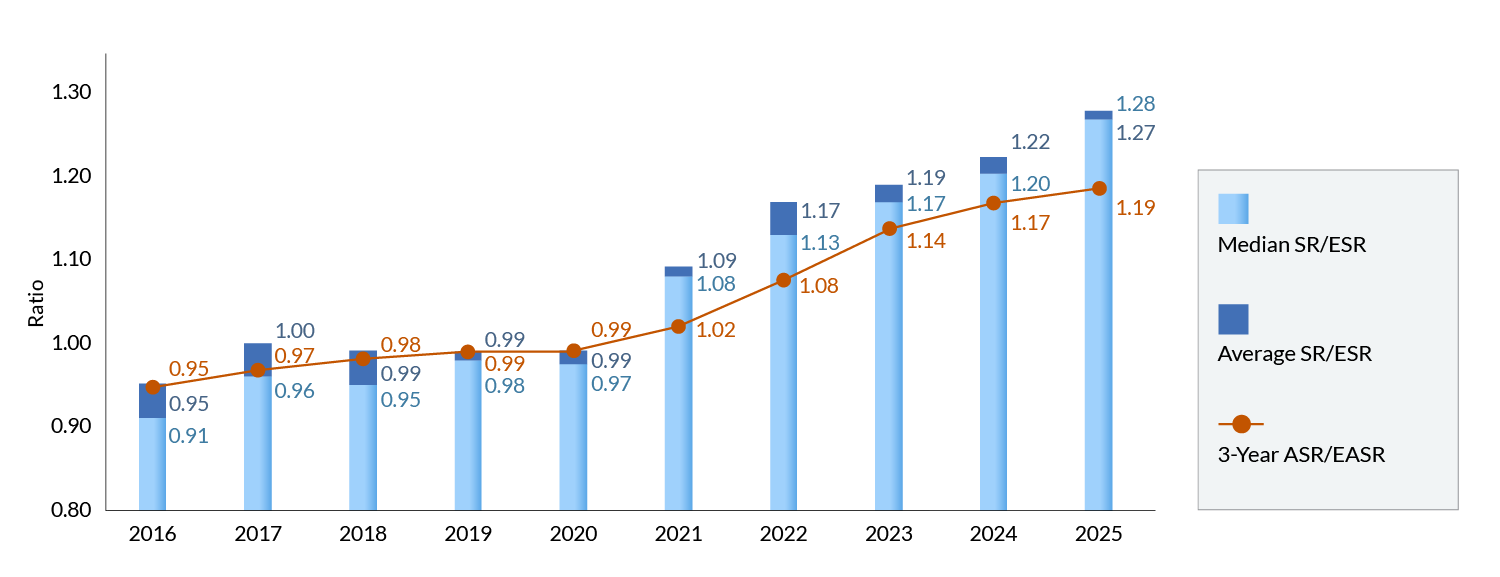

The solvency position of federally regulated private pension plans with defined benefit provisions improved in 2025. The median ESR for the 296 plans included in the exercise (down from 303 last year) increased to 1.28 as at December 31, 2025, up from 1.20 at the end of 2024. The liability weighted average ESR for all plans is 1.27 as at December 31, 2025, up from 1.22 at the end of 2024. The main drivers of the variation from the SR at the end of 2024 to the ESR at the end of 2025 are the positive investment returns and the increase in solvency discount rates. The three-year estimated average solvency ratio (EASR), on which funding requirements are based, has increased to 1.19 as at December 31, 2025, up from a three-year average solvency ratio (ASR) of 1.17 at the end of 2024.

Graph 1 below shows the reported SRs, median SRs, and ASRs from December 2016 to December 2024. It also shows the ESR, median ESR, and the three-year EASR for December 2025.

Graph 1 - Text version

| Year | Median SR/ESR | Average SR/ESR | 3-Year ASR/EASR |

|---|---|---|---|

| 2016 | 0.91 | 0.95 | 0.95 |

| 2017 | 0.96 | 1.00 | 0.97 |

| 2018 | 0.95 | 0.99 | 0.98 |

| 2019 | 0.98 | 0.99 | 0.99 |

| 2020 | 0.97 | 0.99 | 0.99 |

| 2021 | 1.08 | 1.09 | 1.02 |

| 2022 | 1.13 | 1.17 | 1.08 |

| 2023 | 1.17 | 1.19 | 1.14 |

| 2024 | 1.20 | 1.22 | 1.17 |

| 2025 | 1.28 | 1.27 | 1.19 |

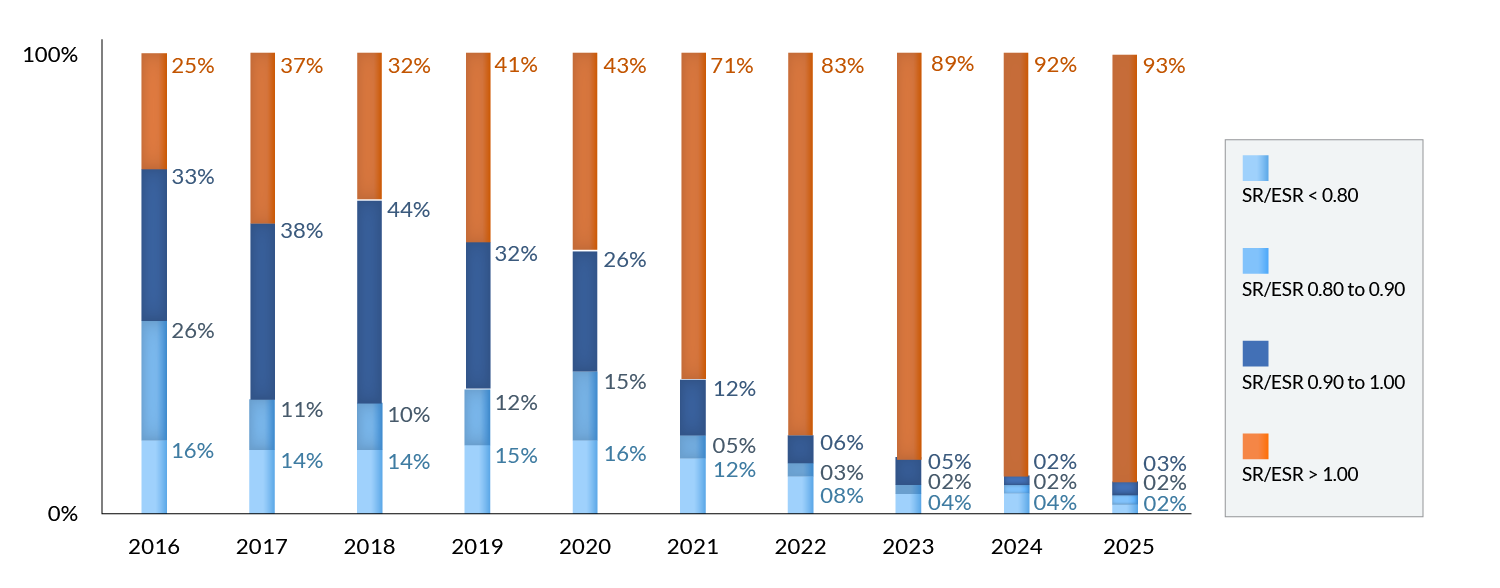

The most recent ESR results show that over 90% of pension plans with defined benefit provisions are fully funded. There was a reduction in the percentage of plans that were underfunded (7% in 2025 versus 8% in 2024). The number of plans that were significantly underfunded (SRs or ESRs below 0.80) also decreased (2% in 2025 down from 4% in 2024). It should be noted that all significantly underfunded plans are designated plans and therefore their funding is limited by the Income Tax Regulations. Graph 2 below illustrates the distribution of the SR/ESR results as at December 31 of each year since 2016.

Graph 2 - Text version

| Year | SR/ESR < 0.80 | SR/ESR 0.80-0.90 | SR/ESR 0.90-1.00 | SR/ESR > 1.00 |

|---|---|---|---|---|

| 2016 | 16% | 26% | 33% | 25% |

| 2017 | 14% | 11% | 38% | 37% |

| 2018 | 14% | 10% | 44% | 32% |

| 2019 | 15% | 12% | 32% | 41% |

| 2020 | 16% | 15% | 26% | 43% |

| 2021 | 12% | 05% | 12% | 71% |

| 2022 | 08% | 03% | 06% | 83% |

| 2023 | 04% | 02% | 05% | 89% |

| 2024 | 04% | 02% | 02% | 92% |

| 2025 | 02% | 02% | 03% | 93% |

The first quarter of 2026 was marked with interest rate and market volatility. Overall, the solvency situation of federally regulated private pension plans is expected to decrease due to recent market developments.

Regulatory filings and important dates

Important reminders and dates

Annual filings and plan amendments must be filed using the Regulatory Reporting System (RRS).

Under the Pension Benefits Standards Act, 1985:

| Action or Required Filing | Deadline |

|---|---|

| Annual Information Return (OSFI 49) and Schedule A – Canada Revenue Agency Information Requirements (OSFI 49A) | 6 months after plan year end |

| Pension Plan Annual Corporate Certification (PPACC) | 6 months after plan year end |

| Certified Financial Statements (OSFI 60), Auditor's Report Filing Confirmation (ARFC) and, if required, an Auditor's Report | 6 months after plan year end |

| Payment of Plan Assessment | Upon receipt of the OSFI-issued invoice |

| Annual statements to members and former members and their spouses or common-law partners | 6 months after plan year end |

| Amendments to documents that create or support the plan or pension fund | Within 60 days after the amendment is made |

| Action or Required Filing | Deadline |

|---|---|

| Actuarial Report and Actuarial Information Summary and, if required, Replicating Portfolio Information Summary | 6 months after plan year end |

| Solvency Information Return (OSFI 575) | The later of 45 days after the plan year end or February 15 |

Documents in support of an application for plan registration can be submitted by email to Approvals-Approbations@osfi-bsif.gc.ca. All other documents in support of an application that requires the Superintendent's authorization must be filed using RRS. For additional information including instruction guides for filing an application using RRS, please visit the Amendments, Applications and Approvals section of our website.

Under the Pooled Registered Pension Plans Act:

| Action or Required Filing | Deadline |

|---|---|

| Pooled Registered Pension Plan Annual Information Return (includes financial statements) | April 30 (4 months after the end of the year to which the document relates) |

| Auditor's Report | April 30 (4 months after the end of the year to which the document relates) |

| Pension Plan Annual Corporate Certification (PPACC) | April 30 (4 months after the end of the year) |

| Payment of Plan Assessments | Upon receipt of the OSFI-issued invoice |

| Annual statements to members and their spouses or common-law partners | February 14 (45 days after the end of the year) |

Other topics

Pension Awareness Day 2026

In February 2026, we participated in Pension Awareness Day, an annual event dedicated to raising awareness of pension plans and their value.

To support this initiative, we shared a comprehensive Pension Awareness Day toolkit, developed by the Financial Services Regulatory Authority of Ontario, Ontario's pension regulator, with all federally regulated private pension plan administrators and with pension industry stakeholders. The toolkit included templates for social media posts, email campaigns, and news releases to help amplify the message across multiple communication channels.

Pension Plans Survey - Update

Last fall, as part of our ongoing commitment to be responsive to stakeholder input and to continually improve performance, we conducted an online survey with pension plan administrators and other pension stakeholders of federally regulated private pension plans.

The survey was administered by Phoenix Strategic Perspectives Inc. (Phoenix), an independent third party. Phoenix was also responsible for compiling the results of the survey and preparing a final report, which is now available on the Library and Archives Canada website. The final report presents results in summary form only, without attributing them to any individual or organization. Our teams are reviewing the findings and developing an action plan to address key areas that present opportunities for improvement.

Thank you to everyone who participated in the survey and provided valuable input.

Organizational changes

Brendan Carley was appointed Managing Director of the Legislative Affairs and Strategic Relations Division in February 2026. This position was previously held on an interim basis by Vlasios Melessanakis. Claire Ezzeddin, Director, Private Pension Plans, Legislative Affairs and Strategic Relations, is now reporting to Brendan Carley.